Research Notes

Strategy

- Despite a testing of the SPX 65-day low, our stress indicators have not yet triggered. The NDX still is not oversold despite META’s best efforts. Importantly, the rise in nominal yields is carried on the back of real rates, not inflation expectations.

- One of the keys here will be regional banks and BB vs BBB spread performance to indicate whether this is being discounted as a supply shock, or more systemic. For now it’s the former not the latter.

- One of the keys here will be regional banks and BB vs BBB spread performance to indicate whether this is being discounted as a supply shock, or more systemic. For now it’s the former not the latter.

- The probability of an Iran Israel/US conflict ending by the end of April dropped from 50% to 38% since the beginning of the week.

- That’s consistent with the bull -bear spread which has moved into a more neutral zone and more typical with the 13wk S&P historical returns. Our RenMac credit conditions model is deteriorating, but not to the point of issuing a sell signal.

- That’s consistent with the bull -bear spread which has moved into a more neutral zone and more typical with the 13wk S&P historical returns. Our RenMac credit conditions model is deteriorating, but not to the point of issuing a sell signal.

- Gold has bounced out of the oversold condition. We believe that there is still more to room to run, but we believe this is likely part of a consolidation, not a resumption of the up trend, at least until real rates go down.

- 10yr Treasury yields are overbought in close proximity to the downtrend line dating back to 4Q 2023. U.S. yields have held up better than most G7 nations which have seen yields breaking out in the face of higher oil. This move has pushed5-yr – 5yr forward inflation expectations to their lowest levels since April of last year; the teeth of the tariff tantrum.

- That may help explain golds weakness, though that’s likely a multi-dimensional issue not just a U.S. inflation expectation play.

- Staples are tactically oversold, but the bearish relative conditions persist. This is NOT the sector we'd favor for defensive exposure.

Economics

- Higher oil prices won't produce a symmetric investment boom. The shale industry has been through two brutal cycles, investors have demanded capital discipline since, and breakevens have risen to $60-$65/bbl on labor and steel inflation. Most drillers expect the geopolitical shock to fade. The investment response will be slower and more muted than history suggests.

- The consumer hit comes faster. Gas prices bite disposable income quickly, and without savings buffers, real spending slows, especially for lower-income households.

- Modeling a ~60% Brent surge through the Atlanta Fed's Bayesian VAR framework shows mining investment responding positively, but the net impact is clearly negative: real GDP roughly 1% below baseline by end-2026, deepening to 2.2% longer run, with consumption accounting for 2/3 of the drag.

- Construction spending slipped 0.3% in January after December's 0.8% pop. Nominal spending is up ~1% YoY, but that likely flatters the real picture - in volume terms, construction is going nowhere.

- Two things stand out to Neil. Private nonresidential construction fell 0.4% for the 4th straight month, and the data center boom isn't big enough to offset the broader weakness. Real structures investment is tracking negative for Q1.

- On the residential side, the pipeline is thin. New single-family homes sold but not started hit a fresh low of 50k in January, down sharply YoY, and private single-family construction spending is already off ~6% annually. Both residential and nonresidential structures will be a drag going forward.

- Traditional macro drivers (gas prices, equities, claims) have been undershooting Conference Board CCI by ~18 points since early 2024, more than a full standard deviation. As of February all three inputs looked fine yet confidence was still -9% YoY. Whatever is driving the gloom isn't showing up in traditional macro channels.

- Since then gas is up nearly a dollar and equities are off 8%, so the macro headwinds are only now beginning to arrive on top of pre-existing pessimism.

- On whether it matters for spending, the vibes gap is real but has yet to bite. Real PCE has consistently exceeded what depressed sentiment implied, and that gap widened in 2026.

- Expectations-based measures do lead spending with statistical significance, but present-situation measures mostly just reflect it. Right now they're telling different stories, so the signal is ambiguous.

- The SF Fed's Daily News Sentiment Index hit -0.22 on March 22, the lowest since June 2023. The index tracks economic sentiment via textual analysis of news articles and tends to lead survey-based consumer confidence measures.

- Worth taking seriously, real household consumption ex-healthcare has been slowing over the past year alongside deteriorating sentiment. Impulse response analysis shows a one-standard deviation shock hits spending immediately, with peak impact around 4 months out.

- Mortgage applications dropped nearly 20% over the past two weeks as the 30-year fixed rate hit 6.43%, a five-month high. The rate spike, driven by Treasury yield pressure from Middle East tensions, is quickly reversing months of demand stability.

- Refi activity took the harder hit, down 15% this week as the refi-incentive window closed. Purchase apps fell a more modest 5%, but even committed buyers are starting to pull back at these financing costs. The divergence is a classic pattern: rate-sensitive segments lead the retreat first.

- Import prices +1.3% in February, biggest gain since March 2022 and notably broad - record monthly jump in capital goods, industrial supplies up 2.6% after a 2.4% January increase, nonfuel YoY now at 2.5%. Not just an energy story.

- Export prices confirmed it at +1.5%, with synchronized gains to Canada (1.9%) and the EU (+3.2%). When it's moving this broadly across trading partners, it's a global inflation dynamic, not a domestic blip.

RenMac Off-Script Podcast

.png?width=717&height=403&name=01-16-26%20RenMac%20-%202%20(1).png)

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

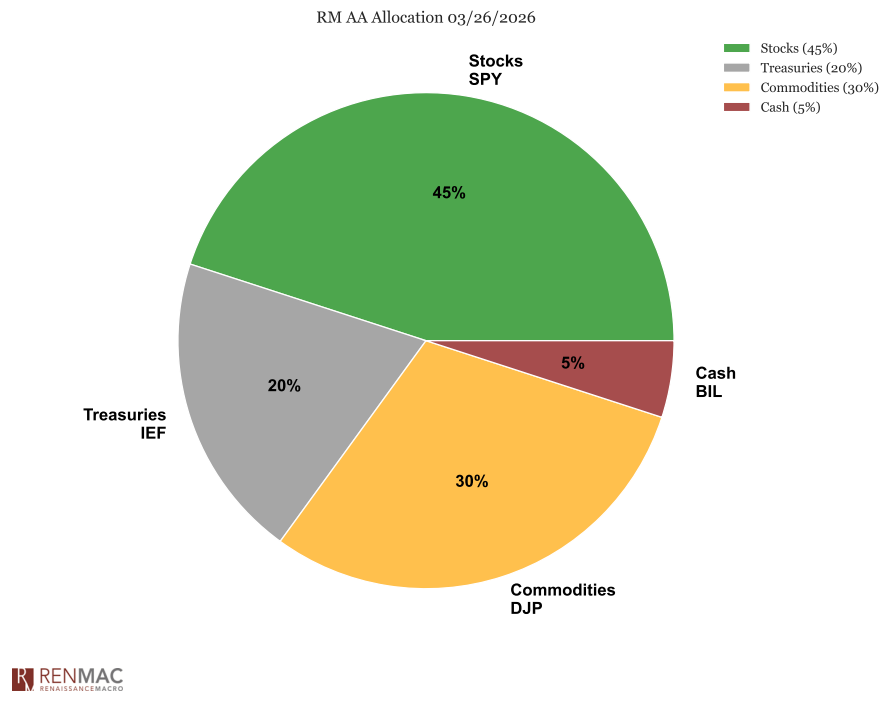

Asset Allocation Model

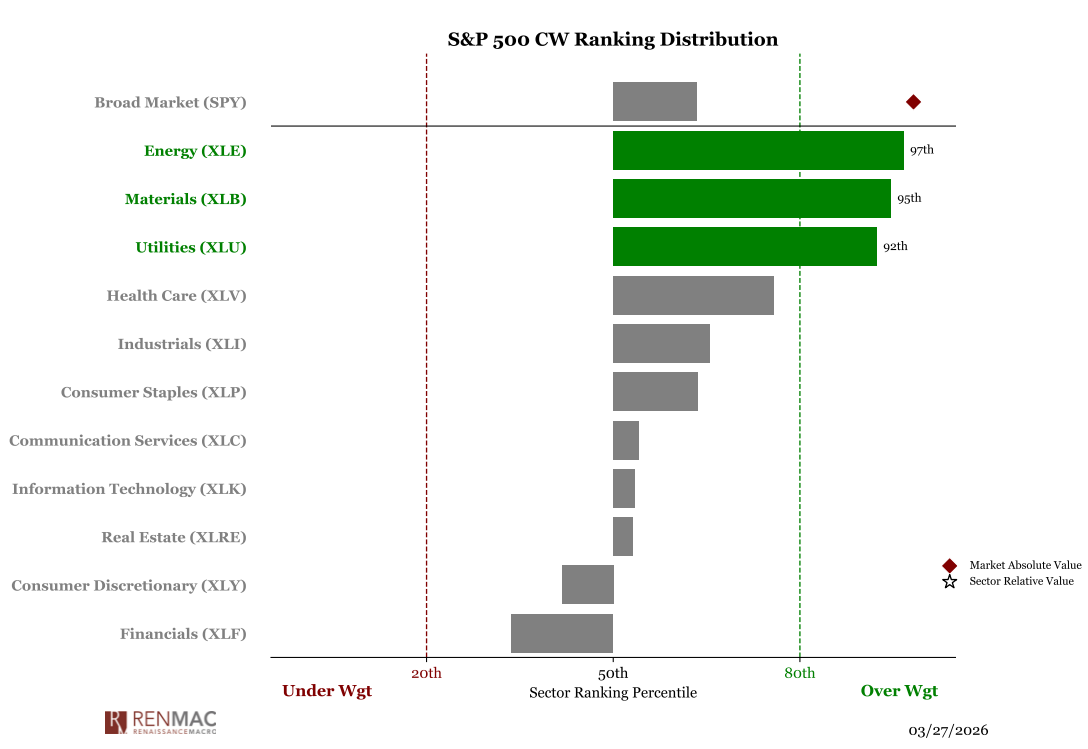

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week