Research Notes

Strategy

- Mag-7 is overbought and parabolic, as we saw in Q3 '24 and Q1 '25. Best move: don't chase with fresh money, use consolidations to scale up.

- The Russell 2000 closed at a new record high for the first time in almost four years, Wed expect some consolidation here but don't buy into the calls for a "triple-top". First, we don't believe in triple-tops and second, this chart looks like it's going to take another leg higher in the 4th quarter.

- Lower Treasury yields have translated into the lowest fixed mortgage rates since 2022. That has predictably boosted homebuilders, but building product names made a fresh relative strength low on Tuesday.

- Cyclicals hit a new high versus defensives. Not what you'd expect to see on the verge of something nefarious from an economic standpoint.

- Watch update on this and our beta --> momentum trade here.

- This week, we saw a new high in the SPAC and IPO index. You can put this down in the "animal spirits" camp where good things are happening, and that tends to be bullish.

Economics

- Some Neil thoughts on the Fed:

- There is no conviction around next year. Seeing stronger nominal growth, a lower unemployment rate and just one rate cut seems somewhat incongruent.

- Powell mentioned that 50bps wasn't seriously considered - recall that in July of last year, Powell hinted that it was a close call to hold off on easing.

- Powell made a very revealing admission: "We have two sided risks which means there is no risk-free path." Neil thinks this means the next 2 meetings should be priced closer to coin flips, and that 3 cuts are far from guaranteed.

- Retail sales blew past estimates in August, climbing 0.6% vs 0.2% expected. Control sales (ex. building material stores, autos, and gasoline) surged 0.7%, climbing 8.2% SAAR over last 3 months. This is a solid performance though it is worth highlighting that consumption is rarely what leads to a slowdown.

- US equities remain buoyant even as bonds price faster rate cuts and subdued inflation. Markets seem to be betting on a productivity boom to justify earnings expectations - but with productivity up just 1.5% over the past year and R&D spending at its weakest pace since 2010, there's little evidence of a surge.

- The NAHB index slipped to 32 in September, still below the 50 mark signaling pessimism. While six-month sales expectations improved, buyer traffic hit a three-month low, pointing to weaker residential investment ahead.

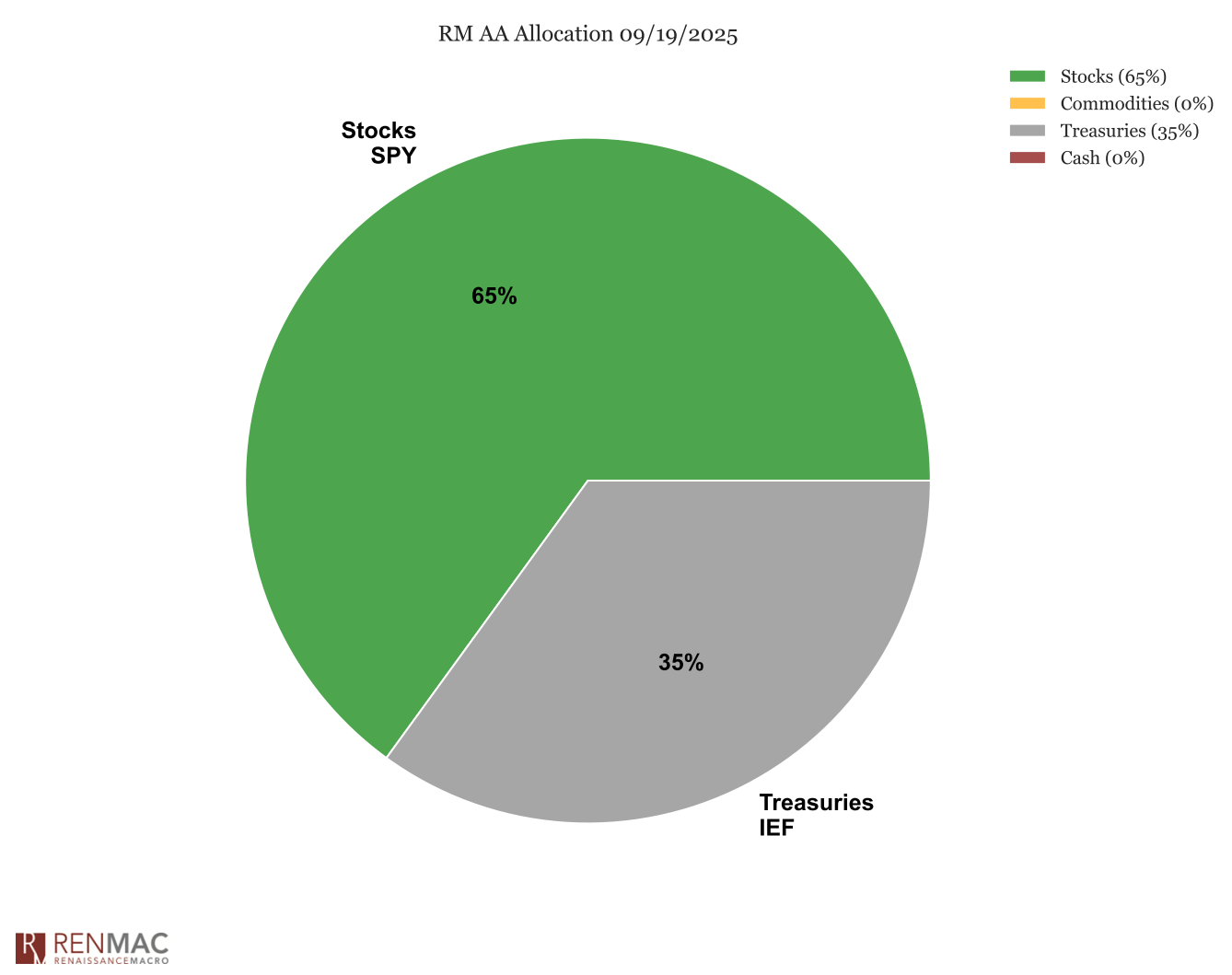

Asset Allocation Model

Sector Ranks

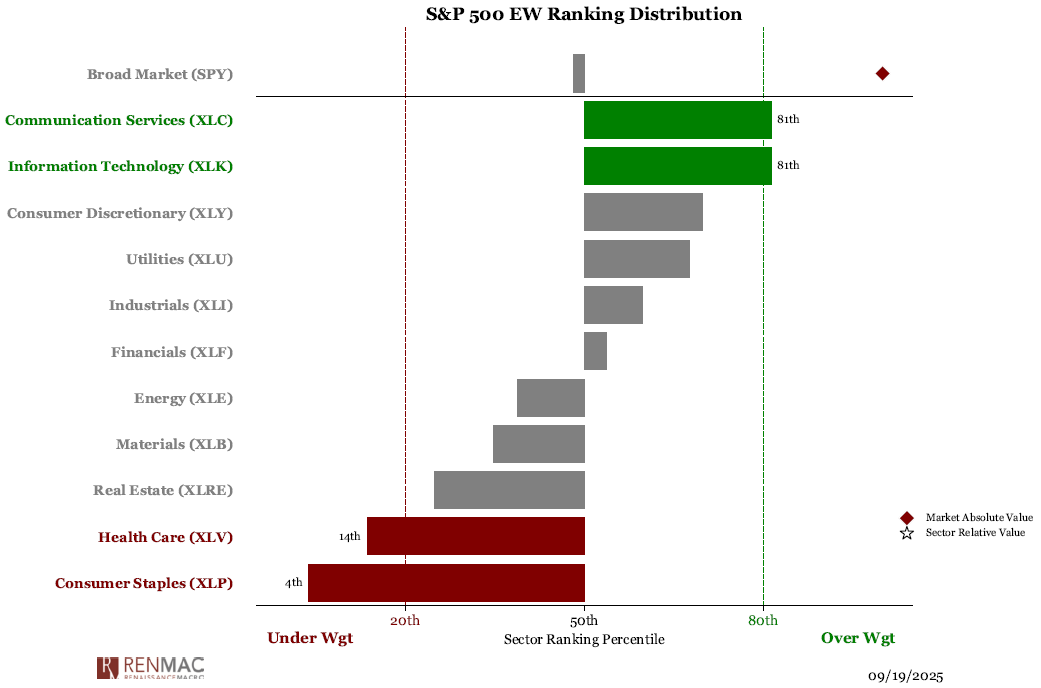

Sector Ranks  Chart of the weekThe near +30% move in INTC Thursday proves that the QAI trade is still alive and well. 25% of the components in the S&P 1500 Semiconductor Industry made positive volatility alerts as the SOXX ETF broke out to new all-time highs. Semi's have bucked the weak seasonal trend and have had a big run in the month of September so far. However, Semi's are very overbought and look poised for at least some consolidation.

Chart of the weekThe near +30% move in INTC Thursday proves that the QAI trade is still alive and well. 25% of the components in the S&P 1500 Semiconductor Industry made positive volatility alerts as the SOXX ETF broke out to new all-time highs. Semi's have bucked the weak seasonal trend and have had a big run in the month of September so far. However, Semi's are very overbought and look poised for at least some consolidation.

RenMac Off-Script Podcast

Research Notes

Economics

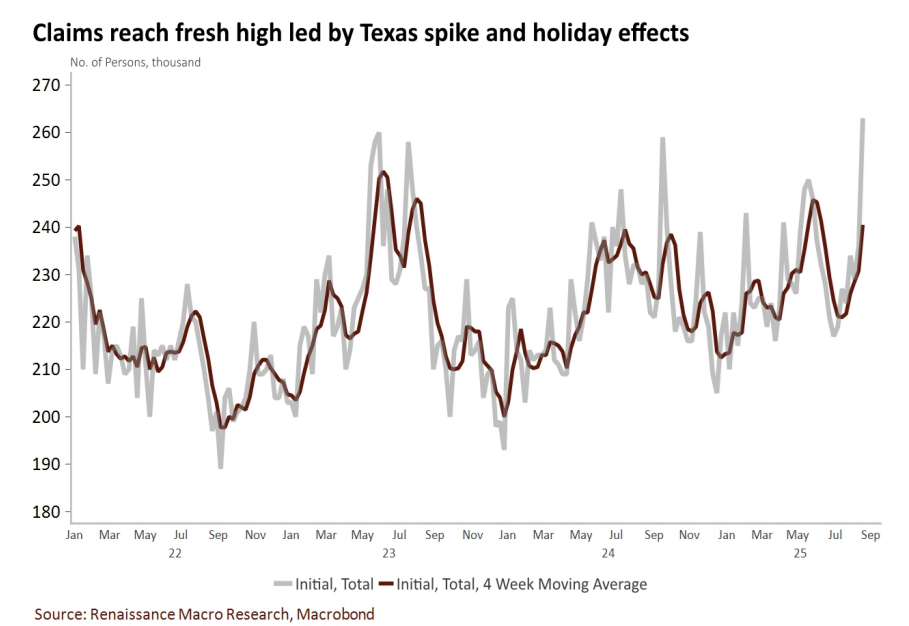

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week