Research Notes

Strategy

- From a purely seasonal perspective historically (1928-2024),, Thursday was the best day to buy stocks for a 3-month holding period. Cyclicals tend to dominate defensives as well. Gold also tends to do well, but we don't follow seasonality blindly.

- Given the recent excessive inflows to gold ETFs, we believe the sentiment environment is more likely to dominate than the seasonals.

- What to do with gold and some of these angels that appear to be falling from grace? Wait until they become oversold in unison.

- Much like the industry and sector works we focus on for optimal entries, we suspect over 50% of this basket will get oversold in unison and will then give us a lower risk entry to await the return of animal spirits.

- Should those names rally and fail, they're likely done and dormant for years, but even if the oversold condition proves to be a tactical bounce, there is potential to extract pounds of flesh between these emotionally charged extremes.

- If this is a weak dollar story, don't say it too loudly because most of precious metal's strength over the last few months has come with the $ reaching overbought levels.

- As this fever dream breaks, we'll watch closely for oversold conditions as they will be the first indication of a correction or permanent impairment.

- ICYMI: deGraaf put together a video on Gold earlier this week, as well as how we define bubbles - click here.

Economics

- There are plenty of reasons to expect long-term interest rates to rise, though Neil is focusing on the reasons rates could go the other way. It's always about what's priced in versus what you believe the likely outcome to be.

- WTI crude prices have declined about 20% YTD.

- Market-based measures of apartment rent show renewed slowing with rents climbing at their slowest pace since the pandemic.

- Labor market conditions continue to slow. The latest data from Indeed show ongoing cooling in wage growth in posted jobs.

- While deficits have been large, they have been somewhat smaller than expected at the margin.

- When Neil looks at this table, he thinks its a bridge too far to argue that the breakeven rate to keep the unemployment rate is steady is NEGATIVE.

- In the last 2 months, the economy has added roughly 50k jobs/months but the unemployment rate has climbed by 0.1ppt on average. A breakeven range of 25k to 75k seems like a plausible baseline.

- While the breakeven rate has declined, it has been insufficient in keeping the unemployment rate from rising.

- Employment growth is already weak with less than half of industries adding to their ranks, there is little reason to expect an acceleration, especially with hiring intentions much softer than is typical for this time of year, and key areas of payrolls such as residential construction poised to cool off further.

- Despite lower mortgage rates, housing demand remains weak. Mortgage purchase applications fell 3.2% in the week ending October 17 - the fourth straight decline - and are up just 2.5% over the past six months, even with a 53bp drop in 30-year rates.

- This lackluster response suggests buyers are holding out for better prices, with the average loan size down 2.5% from last year - pointing to smaller home purchases and slower home price growth.

- Service sector activity slid across the Philly Fed District in October. The non-manufacturing business outlook index slid to -22.2, the lowest since June with new orders contracting for the first time in 4 months.

- Full-time employment slid to -4.5 from +9.4, the second month in contraction in the last three.

- Price pressures appear to be abating. Prices received slid to a 3 month low of +12.9 while prices paid cooled to +35.8.

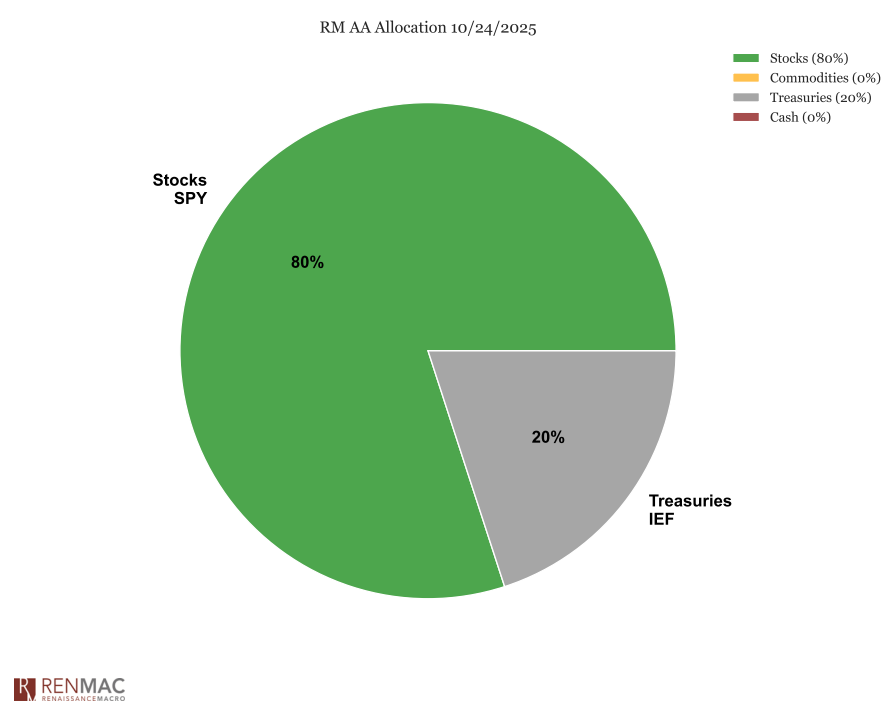

Asset Allocation Model

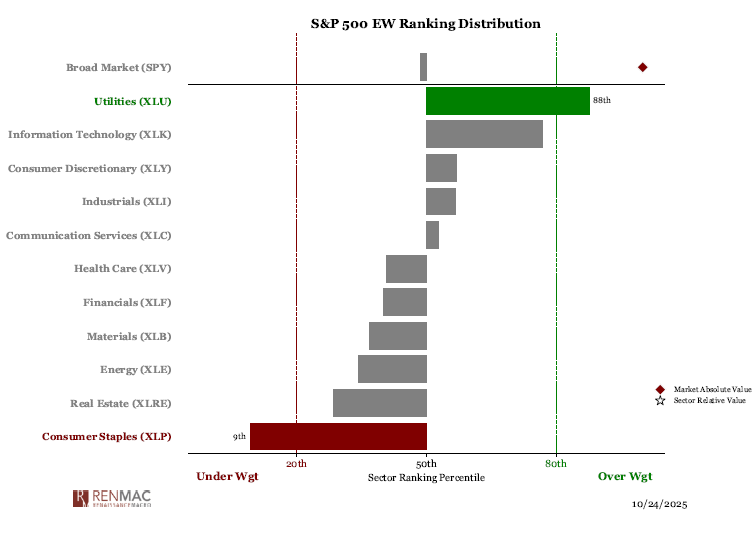

Sector Ranks

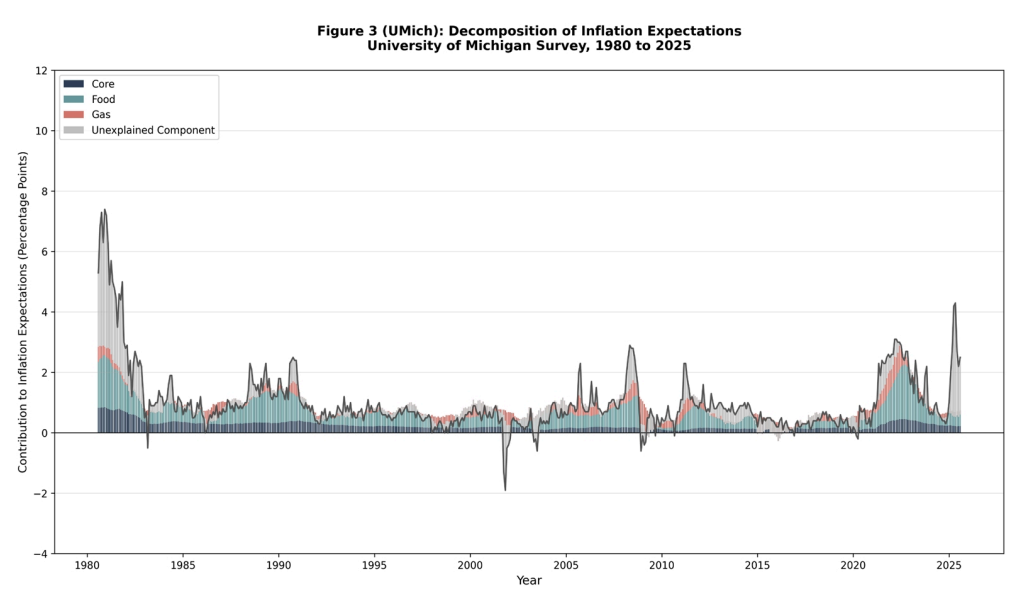

Sector Ranks  Chart of the weekOur replication of the Boston Fed's analysis finds that claims of inflation "de-anchoring" depend more on survey choice than real economic behavior, while the Michigan survey shows a large unexplained gap (predicted 2.9% vs. actual 5.0%), the Conference Board's fit is weaker (29% explained), and the NY Fed's is nearly perfect (3.1% vs 3.2%), suggesting no real break from fundamentals. The assumed link between high inflation expectations and wage pressures ignores today's cooling labor market and declining bargaining power, leaving little evidence that elevated expectations are translating into higher wages.

Chart of the weekOur replication of the Boston Fed's analysis finds that claims of inflation "de-anchoring" depend more on survey choice than real economic behavior, while the Michigan survey shows a large unexplained gap (predicted 2.9% vs. actual 5.0%), the Conference Board's fit is weaker (29% explained), and the NY Fed's is nearly perfect (3.1% vs 3.2%), suggesting no real break from fundamentals. The assumed link between high inflation expectations and wage pressures ignores today's cooling labor market and declining bargaining power, leaving little evidence that elevated expectations are translating into higher wages.

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week