Research Notes

Strategy

- The S&P isn’t oversold either externally or internally—our oscillator is neutral near -0.2, and only about a third of stocks sit above their 20-day averages. The 50-day continues to act as support, suggesting any reset may come more through time than price. Internal stress remains modest, with just 16% of stocks hitting 20-day lows versus the 50%+ extremes that typically mark tradable bottoms. We're looking for a deeper pullback or time-based consolidation to add.

- The Russell 2000 just formed a “golden cross” versus the Russell 1000, signaling improving relative momentum for small caps. The trend looks more durable than last year’s brief move, suggesting the path of least resistance is higher.

- Despite the setup, small-cap ETFs haven’t seen excess inflows yet—investors remain anchored to large caps, which makes the small-cap trade even more attractive as performance builds.

- Major banks kicked off earnings season strong—WFC, MS, and BAC all hit positive volatility alerts and reclaimed YTD highs. We’d stay long large-cap banks and add on relative strength.

- Regional banks continue to lag, with KRE near YTD relative lows. The absolute trend remains bullish, but we’d wait for a relative breakout before adding exposure and stay overweight large-cap vs. small-cap banks for now.

- Crypto remains weak, with Bitcoin drifting toward the lower end of its range. A break below $110K would put the $104K flash-crash lows in play, while Ethereum risks slipping under $3,900 toward $3,400.

- Bitcoin continues to diverge from the NDX, and a downside break could test stronger support in the mid-$90K range.

Economics

- The San Francisco Fed's Daily News Sentiment Index fell to -0.137 on October 5th, its lowest since April, signaling a clear negative shift in economic tone.

- The drop closely tracks weakening consumer confidence and notably occurred before recent market volatility, while prediction markets now expect the government shutdown to last over a month.

- Across 17 industries, higher AI adoption has been linked to stronger - not weaker - employment momentum in 2025, with correlations ranging from 0.23 to 0.43.

- Finance (+9.7 pp AI use) and Healthcare (+4.9 pp) both showed solid job growth, while sectors with minimal AI uptake like Mining saw the steepest job losses.

- The data suggests AI is complementing workers and enabling business expansion rather than displacing jobs - at least so far.

- It's early in the integration phase, but the takeaway is clear: industries investing in AI tend to be the ones still hiring.

- Inflation is not a concern:

- Oil prices have tumbled. This will bleed into retail gasoline prices and pull down survey measures of household inflation expectations.

- Labor markets have slackened. Households report increasing difficulty of finding a job and the unemployment rate has risen 0.1ppt in each of the last two months. Surveys point to additional upward pressure on the jobless rate.

- Housing rental inflation continues to cool off. The latest data from Zillow show that observed rents are up just 2% SAAR over the last three months. This indicates further downside to measure rents in CPI.

- Despite strong growth and GDP projections, unemployment has risen 0.3ppt since March - an unusual divergence. If Okun's Law holds, potential growth would need to be around 4%, which seems implausible, suggesting GDP is overstating true activity and likely to slow ahead.

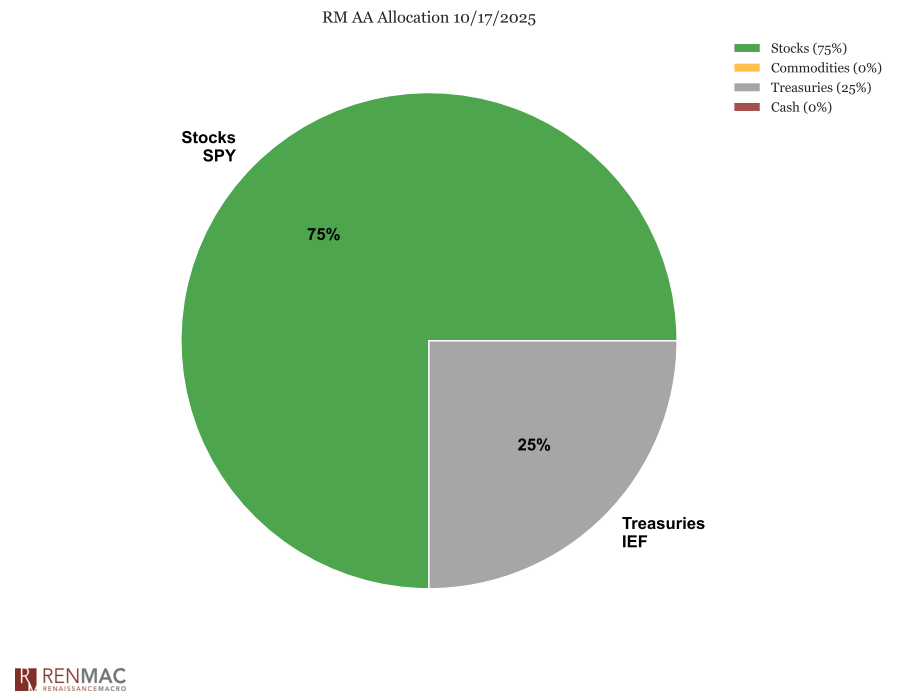

Asset Allocation Model

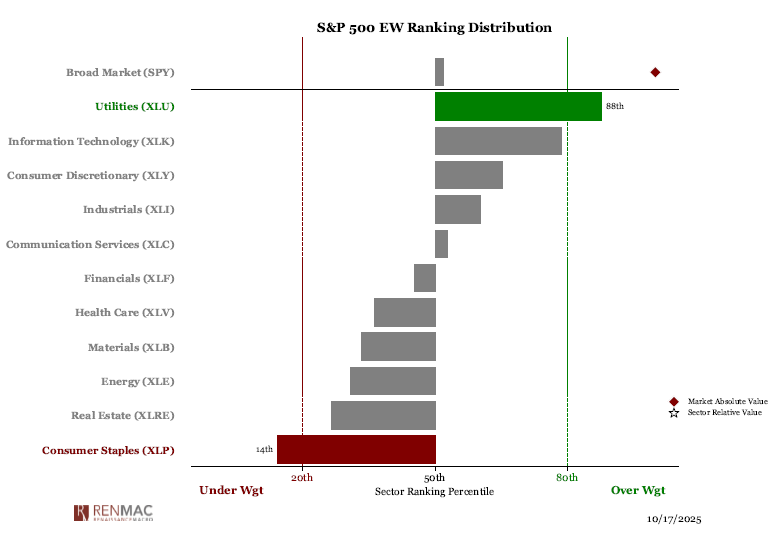

Sector Ranks

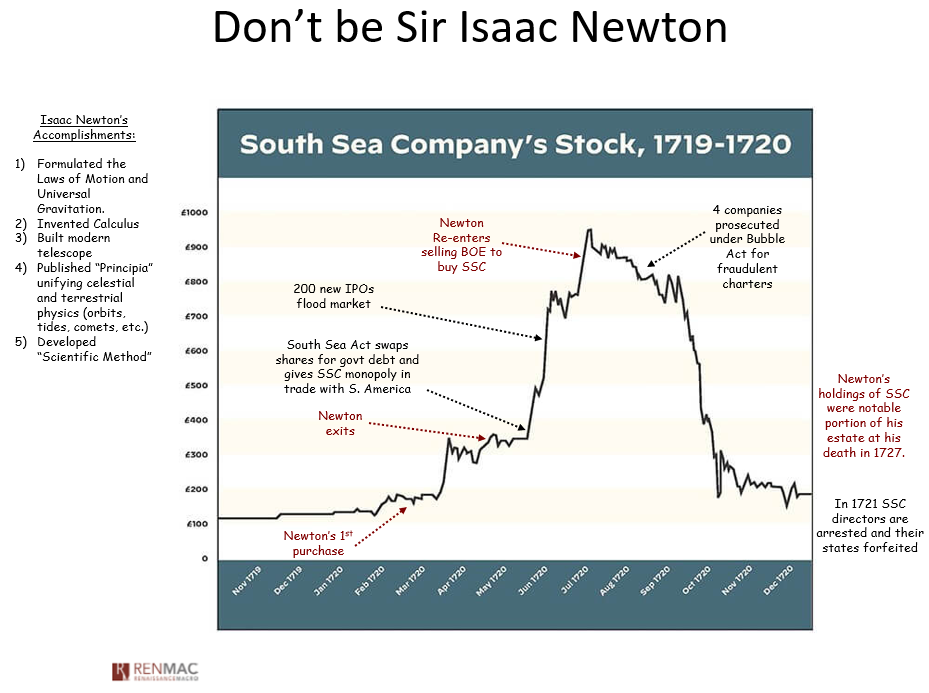

Sector Ranks  Chart of the weekThe story of Sir Isaac Newton and the South Sea Bubble is a timeless lesson in investor psychology. Despite being one of history’s greatest minds—discovering gravity, inventing calculus, and pioneering modern physics—Newton was still swayed by the emotions of greed and fear. After profiting early in the South Sea Company’s rise in 1720, he sold, watched the stock soar higher, and re-entered near the top—eventually losing much of his fortune. The takeaway is simple: even the smartest investors can be undone by euphoria. When markets turn parabolic, stay disciplined—trim systematically rather than chasing or exiting in panic. We’re not in a full-blown bubble yet, but the setup feels increasingly familiar, making discipline and patience more important than ever.

Chart of the weekThe story of Sir Isaac Newton and the South Sea Bubble is a timeless lesson in investor psychology. Despite being one of history’s greatest minds—discovering gravity, inventing calculus, and pioneering modern physics—Newton was still swayed by the emotions of greed and fear. After profiting early in the South Sea Company’s rise in 1720, he sold, watched the stock soar higher, and re-entered near the top—eventually losing much of his fortune. The takeaway is simple: even the smartest investors can be undone by euphoria. When markets turn parabolic, stay disciplined—trim systematically rather than chasing or exiting in panic. We’re not in a full-blown bubble yet, but the setup feels increasingly familiar, making discipline and patience more important than ever.

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week