Research Notes

Strategy

- On average, we would expect roughly a 26% total return for the S&P over the next 3 years, but if we look at valuations we are in a zone where that number drops to 23%. Not statistically meaningful, though we are relatively close to being in the bottom 20th percentile for excess CAPE where we do need to start worrying about the returns.

- Now if we look at the 10yr relative to equities, we see it favoring a tilt towards a higher allocation to bonds as average excess return in equities over 3 years is 20%, but in this zone that drops to 13%.

- In the event that we do get into that bottom 20th percentile zone for excess CAPE, then we're looking at an area where bonds tend to outperform.

- The dollar continues to build on its reversal higher following the September FOMC low, getting close to an overbought condition.

- The bouncing dollar contributed to taking some steam out of the precious metals trade as the gold miners ETF, GDX was down nearly 5% Thursday, it's worst day since May.

- Silver spiked above $50 before having a sharp reversal, suggesting more tactical consolidation or weakness is likely from here. We are still bullish but would stay patient as this is likely not the time to chase.

- Consumer Discretionary is oversold for the first time since the April lows. We are closely monitoring the relative performance of cyclicals versus defensives, as a breakdown would signal increased consumer strain.

- Equal-Weight Discretionary is losing some ground vs. Staples but still remains in a bullish relative trend.

- Homebuilders are weakening again on a relative basis while also flagging as excess alpha in SERM and excessive ETF inflows. Home Improvement Retail and Textiles, Apparel & Retail are back at the relative lows and look vulnerable.

Economics

- When we look at labor (without having BLS data), we have a Bathtub Model of Unemployment, looking at what is flowing in vs out. If we picture this bathtub as the pool of unemployment, a low firing rate has us with a slow flow of water into the tub, but hiring rates are not high enough to outpace those firing rates, causing this to eventually flood.

- Important to note that firms typically reduce hiring intensity before taking more drastic action.

- We estimate the unemployment rate will reach 4.5% by year-end and continue rising next year.

- Mortgage purchase demand has slowed. Over the last 6 months, purchase apps are down 2.4% annualized regardless of the fact that the interest rate on a 30yr mortgage has declined 20bps.

- Additionally, home prices are likely declining. Average loan size on purchase loans is down 3.3% YoY which tends to be a reliable proxy for the direction of travel on national home prices.

- Lately, we've seen a notable slowdown in search queries for home renovations. If less people are searching for these today, we would assume there is less in the pipeline for future renovations spending.

- Medium and heavy truck sales have declined to 0.400 million units SAAR in August, the lowest level since July 2020, representing a 19% decrease YoY. Putting this into a single-indicator recession model points to a 72% 12-month implied recession probability. We've seen many false positives recently, though this is still worth keeping a close eye on as a proxy for activity in the industrial and freight economy. Important to note, this also precedes the 25% tariff just imposed.

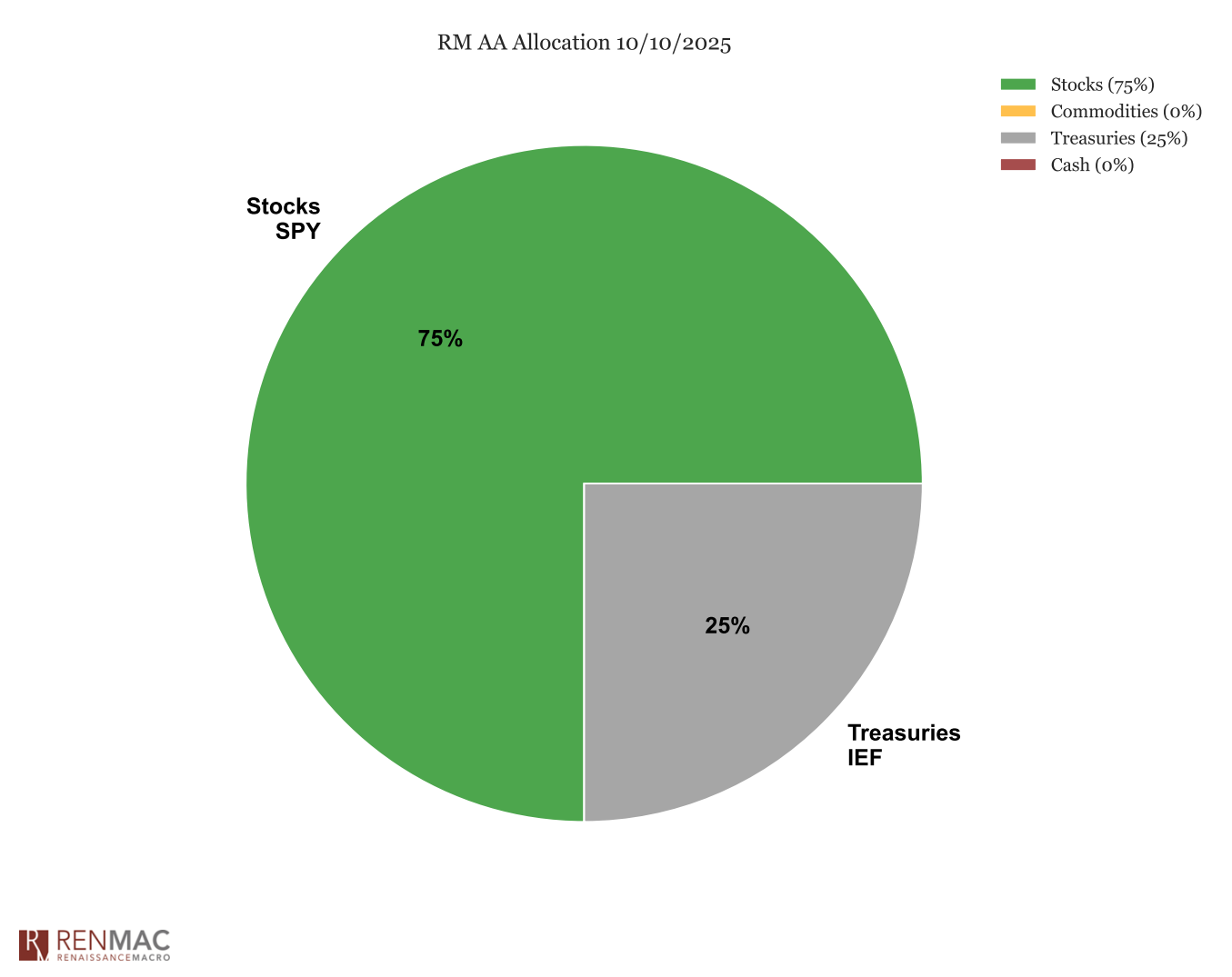

Asset Allocation Model

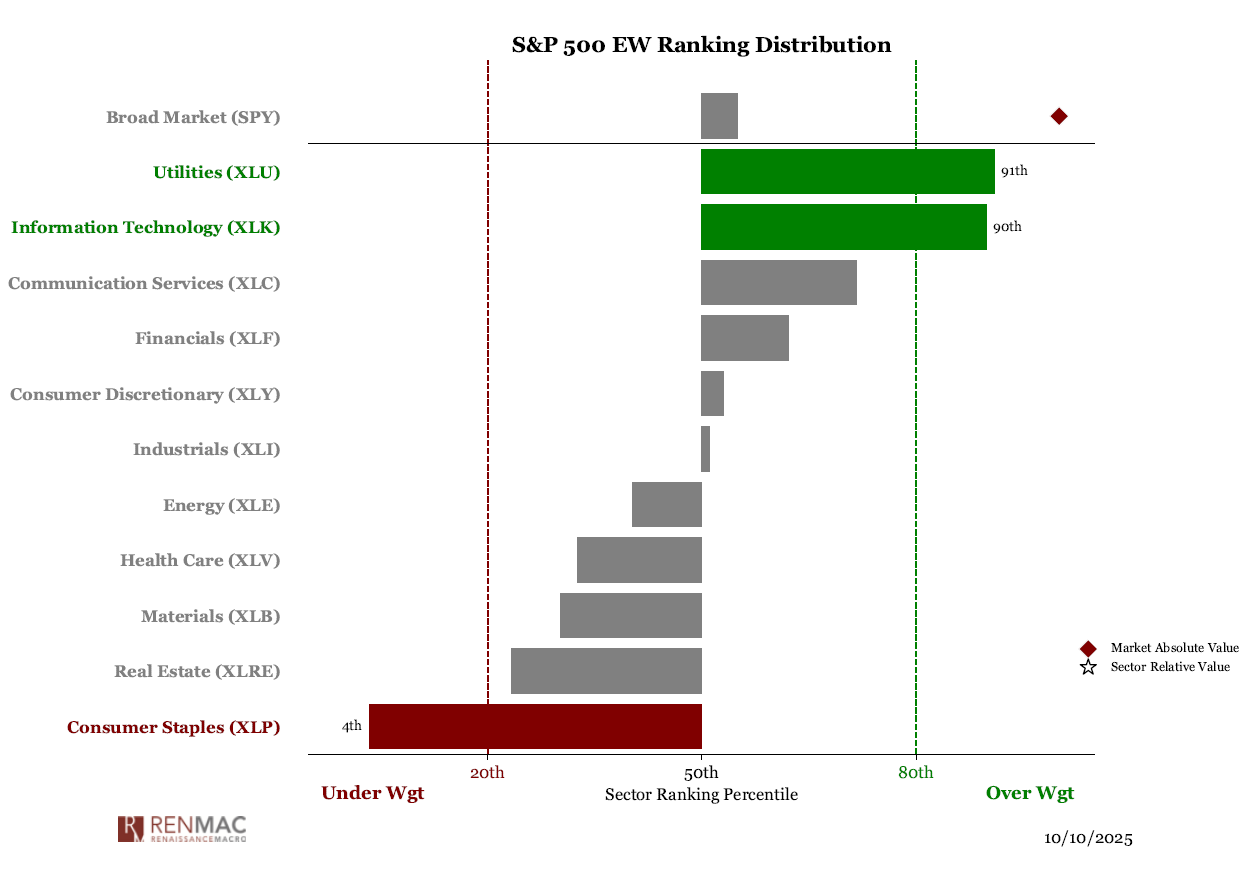

Sector Ranks

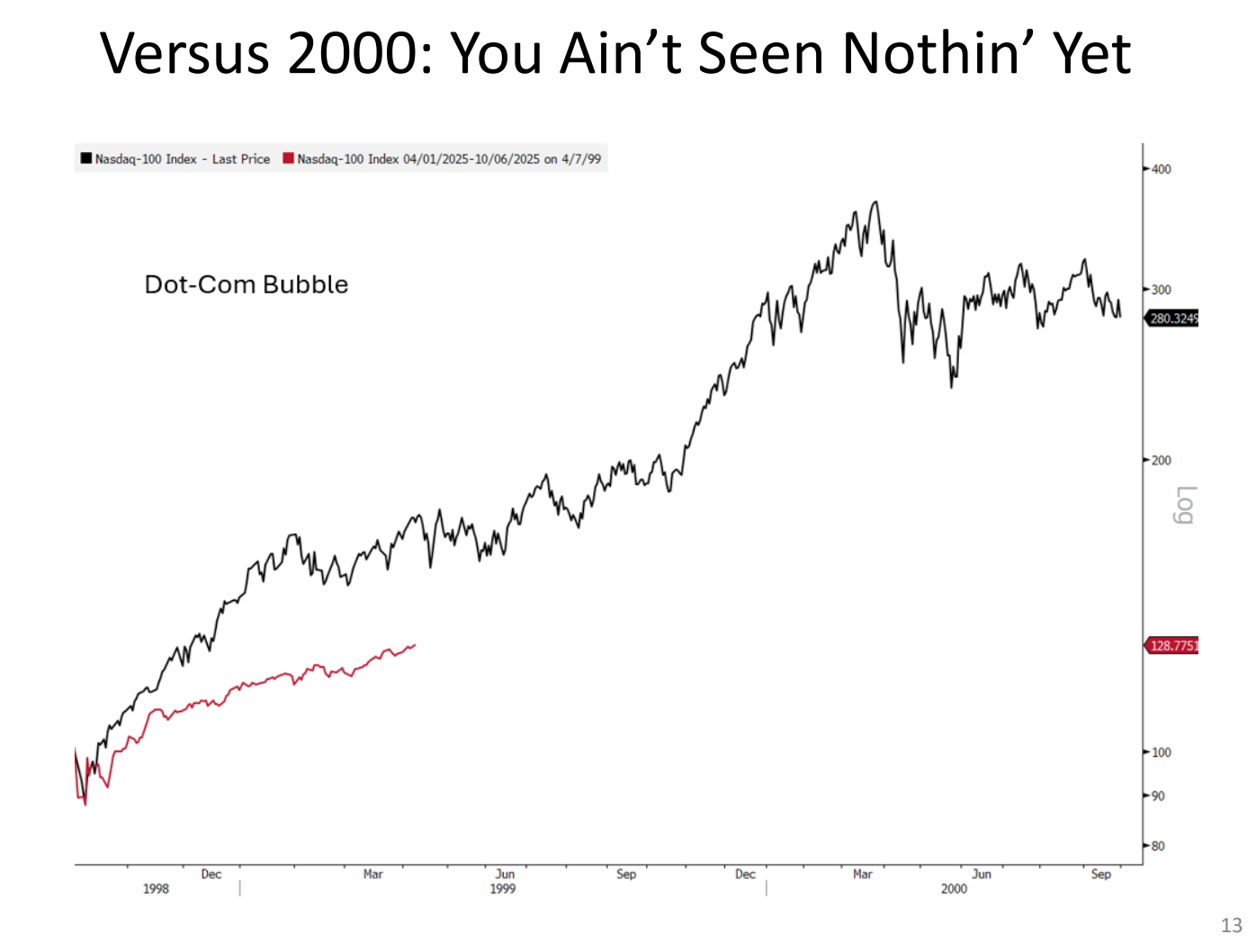

Sector Ranks  Chart of the weekIf we’re comparing today’s setup to 2000, it’s worth remembering that when markets broke out in 1999, the real fireworks came afterward. We’ve aligned today’s move with past crises like LTCM and the tariff shock, and while speculation is clearly heating up, it’s not yet parabolic on a log scale. In other words, things are strong—but not at bubble levels… yet.

Chart of the weekIf we’re comparing today’s setup to 2000, it’s worth remembering that when markets broke out in 1999, the real fireworks came afterward. We’ve aligned today’s move with past crises like LTCM and the tariff shock, and while speculation is clearly heating up, it’s not yet parabolic on a log scale. In other words, things are strong—but not at bubble levels… yet.

RenMac Off-Script Podcast

.png?width=717&height=403&name=10-10-25%20RenMac%20(1).png)

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week