Research Notes

Strategy

- Equal-weight has made new 20-day highs a couple times recently, suggesting this is not a market that's expanding with momentum making consolidations and/or pauses a likely occurrence.

- 52-week highs and lows were 14% and 12% respectively last week, with strength and weakness about what you would expect with utilities and tech dominating high list while staples and real estate dominated the low list.

- When new highs and lows run at equal but low grade levels near an all-time high, markets tend to be rotating.

- At times, that rotation ends up fueling the final flicker of a bull market where winners attract the marginals dollars before bears dominate the tape, or it proves to be a mid-market rotation as a new narrative gains a toe-hold and propels the bulls higher.

- Returns are weaker on the 65-day basis than they are on a 6 or 12-month basis suggesting this is more likely a reshuffle.

- We have the 2nd highest number of stocks making 52-week relative lows since 1957.

- We did an analysis on market returns when you are within 5% from an ATH. In the current zone given relative highs/lows, average return is 35bps in next 3 months, while overall average is about 192bps.

- Many of the sentiment indicators have ticked into the upper historical boundary suggesting elevated levels of bullishness.

- Historically, extremes in bullishness are not as timely as that in bearishness, so we're willing to give the bulls a bit more leash to reinforce their unrestrained illusion.

- Historically, extremes in bullishness are not as timely as that in bearishness, so we're willing to give the bulls a bit more leash to reinforce their unrestrained illusion.

- S&P sets its sights on the ascending 50-day.

Economics

- Private sector employment returned to growth in October as ADP reported a 42k increase in payrolls, following a revised 29k decline in September - exceeding expectations. However, the 3-month average gain of just 3k underscores significant deceleration in hiring momentum.

- The October gains were concentrated in specific sectors and firm sizes, revealing an increasingly uneven hiring landscape.

- Trade, transportation, and utilities led with 47k new positions, while education and health services contributed 25k and financial activities added 11k. Offsetting these gains were losses in information services (-17k), professional and business services (-14k) and manufacturing (-3k). Notably, all net job creation came from large companies while small businesses declined for the fifth time in the last six months.

- Ship counts from Asia to the US are down sharply against last year (~20%). Many of the goods coming into the US drive retail employment. Put differently, the jobs being supported by imports are often Made in the USA. Not a good signal for retail employment.

- Despite mortgage rates hovering near recent lows, purchase activity showed little improvement in late October. Mortgage applications slipped 1.9% for the week ending October 31, the first decline in 3 weeks.

- The expiration of the EV credit in September meant a pull forward of sales into Q3 at the expense of Q4. In October, unit auto sales slowed to 15.32 million SAAR, the weakest pace since January 2025 and running well below their average in Q3.

- The Fed's Q4 loan officer survey showed continued tightening in business credit, with +6.5% of banks tightening C&I standards for large firms and +8.3% for small firms. Loan demand improved modestly for large firms but stayed weak for smaller ones.

- Commercial real estate and household credit showed tentative stabilization: CRE standards still tightened but at a slower pace, while household credit was mostly steady with firm consumer demand and easing in auto loans offsetting tighter subprime mortgage standards.

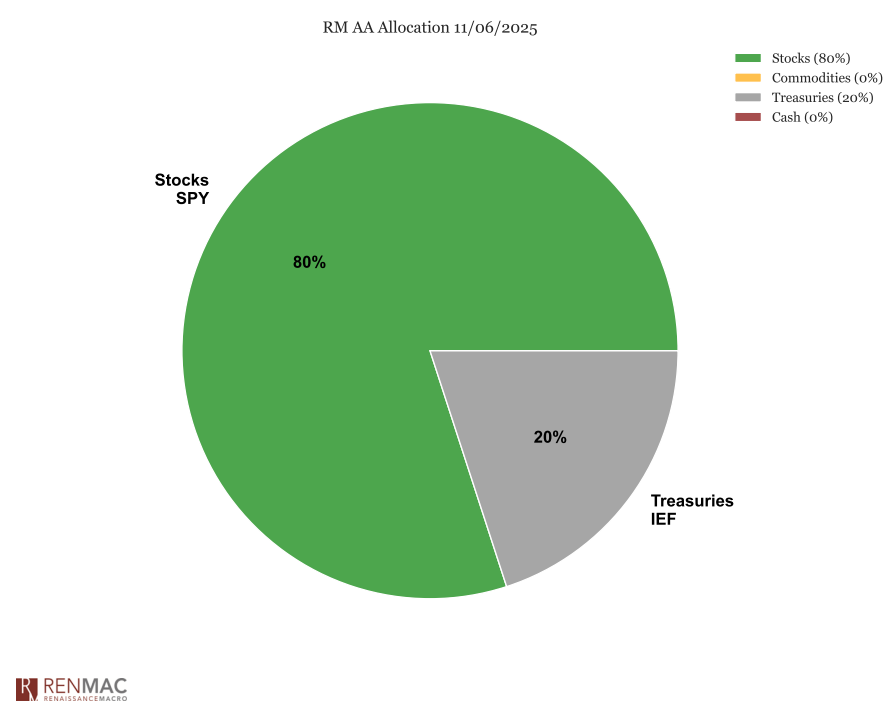

Asset Allocation Model

RenMac Off-Script Podcast

.png?width=717&height=403&name=11-7-25%20RenMac%20(3).png)

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

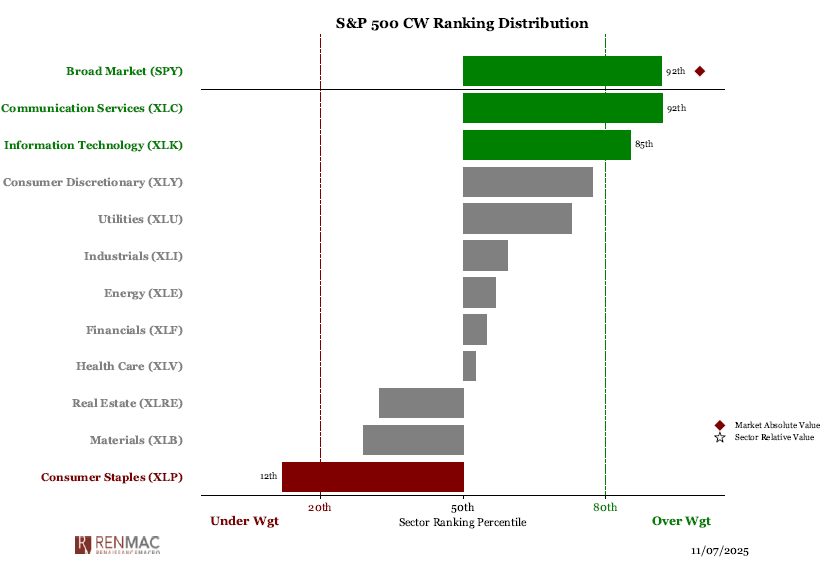

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week