Research Notes

Strategy

- Thursday's outside reversal was a masterclass in ugly. It was the most severe day for the NDX since Oct '18 and worst for SPX since April 4th this year and June '20 before that.

- Good news for those playing SPX is such days have not proven to be a reliable short signal (profitable only 27% of the time 3m out). Not yet oversold on SPX - a condition likely required before a firm low. Only 23% of issues are at 20-day lows, we look for 50% to go on the hunt.

- For the NDX, this moves to 52% success rate on short signal 3m out, though the Equal-Weight NDX is now oversold both externally and internally with 84% of issues registering an oversold condition.

- Bitcoin has broken its January 2023 trend-line, experienced a dark cross, but is mercifully oversold at these levels. Unfortunately, the next legitimate support is about 10% lower.

- Speculative excess has a price. After an unsustainable parabolic run, SPAC and fringe names have shed nearly 25% and are just NOW oversold.

- This is a natural place to expect Fed squawking b/c Tequila nights rarely yield high-performance mornings. Welcome to the hangover.

- The latest sentiment readings show II bull/bear spread pulling back from extreme levels. Since returns tend to drive sentiment, it's not surprising to see bullishness fade this week.

- While the spread and several other sentiment gauges, remains elevated and warrants caution, it is not on its own, a reason to turn bearish.

- Chinese Tech (CQQQ) has reached oversold territory on our oscillator and is approaching support within a bullish trend.

- We remain constructive on China, and the recent pullback looks like a buying opportunity.

- Similarly, Taiwan has reached oversold and looks attractive here.

- R2K broke below 2,326 support level following Thursday's sharp intraday reversal. The index is now oversold for the first time since April, suggesting its due for at least a tactical bounce. If the index fails to rebound and reclaim support level, we expect a further ~4 drop.

- We would prefer patience to wait and see if R2K can respond to oversold before adding exposure.

Economic

- September jobs report showed U3 rate rising to 4.4% (4.44% to 2nd decimal), climbing faster than the Fed expected. Up 0.039%/mo this year, which the pace would bring us to 4.6% by December.

- Job losers are up 88k over the month, with this coming before the recent uptick in continuing claims, increase in WARN announcements, and layoff announcements. Neil thinks more job loss is on the horizon.

- September's sector mix was heavily concentrated in sectors likely driven by temporary or one-off factors.

- Construction added 19k but details show gains came primarily from nonresidential specialty - likely reflecting data-center construction demand rather than broad-based building activity. Given the cooling residential housing sector and sluggish units under construction, this is unlikely to persist.

- Government payrolls also added 22k jobs in September. Federal fell 3k meaning local and state grew 25k. This support is unlikely to persist as state and local governments face mounting pressures from diminishing federal funding flows and softening tax receipts.

- According to the latest Indeed Wage Tracker, posted wage growth slowed to 2.38% in October from 2.58% in September. This can be seen as a leading indicator for overall wage growth.

- Construction, food service, cleaning & sanitation, and childcare remain quite sluggish - if these areas are showing weak wage growth, it implies demand for labor is weak.

- There is no inflationary impulse coming from jobs market and that should give the Fed confidence to continue lowering rates. That they aren't introduces needless downside risk to the outlook.

- Business inflation expectations have been normalizing since April with 12m inflation expectations now at 2.2% - unchanged from a year ago. If firms were planning to raise prices because of tariffs, wouldn't that be reflected in year-ahead expectations?

- Credit rejection rates hit record high in October survey, with increases across the board, but the most noticeable jump being seen in auto loans.

- The share of discouraged borrowers who refrained from applying due to expected rejection edged up to 8.0% from 7.2% in June and 6.6% last year, but respondents show they are more prepared in the likelihood of needing $2,000.

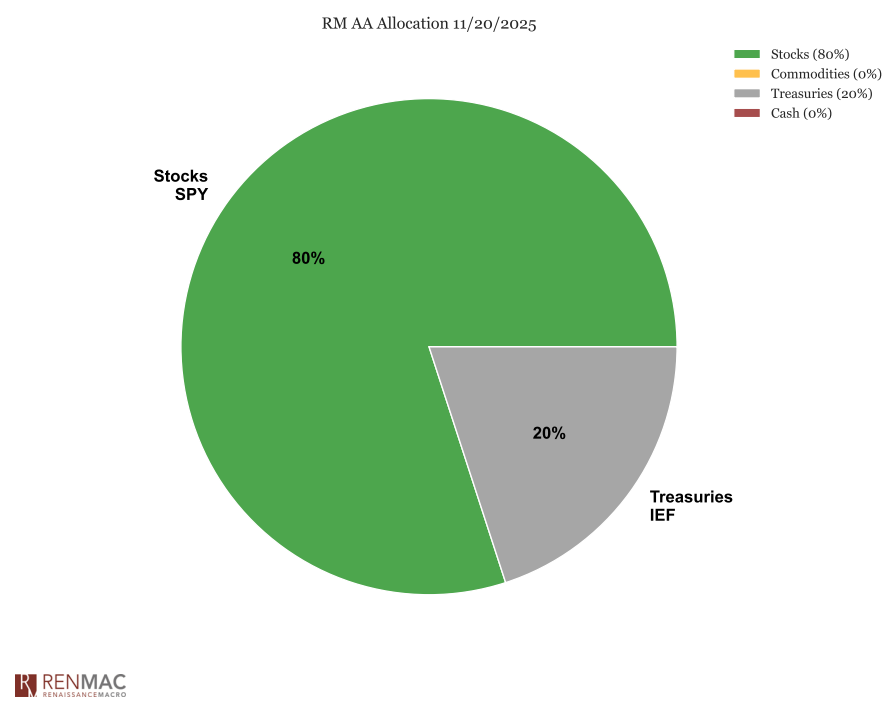

Asset Allocation Model

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

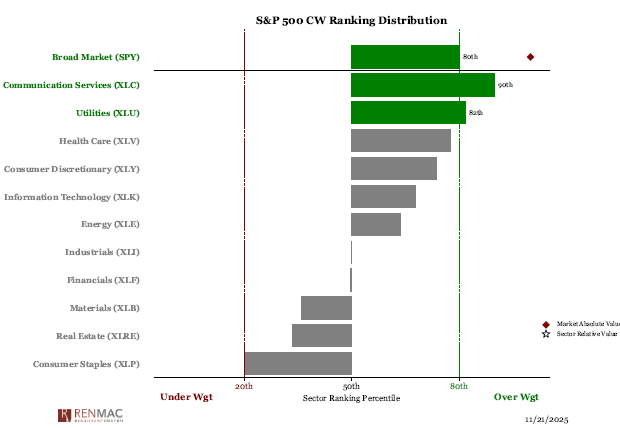

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week