Research Notes

Strategy

- The market discounted a December policy pause by turning risk-off, driving Bitcoin under $100k, officially cracking our Application Software relative trends, and pushing consumer services into a deeper oversold condition. Changing expectations is one thing, making a policy mistake is another, and the market is walking a messaging tight rope.

- Energy is showing some early signs of life after months of lethargy. The percentage of U.S. energy stocks above their 20-DMA has turned higher and is leading all industry groups.

- The relative trends have not turned, but we're willing to give more appreciation to the group because of the strength we're seeing in energy in both Europe and Asia.

- SPACs and all things speculative a month ago are approaching oversold conditions. They're not there yet, but should be with a little nudge. Legitimate uptrends find support in oversold conditions.

- If these quantum and rare-earth names can't find support out of these points, it suggests speculative spirits have turned sour.

- Little progress in overall indices masked some of the breadth improvement with 20-day and 65-day highs climbing, though still below momentum-signaling thresholds.

- That quiet expansion in participation paired with stretched sentiment and the thawing of laggard's performing suggests a transition, not end of trend. As AI-linked names lose altitude, Healthcare, Financials and Precious Metals are filling the void.

Economics

- It is going to be tough to forge a consensus for December and the meeting is much closer to a coin-flip than markets appreciate. Given how participants feel about inflation, this is not like last year. Close calls no longer go to the doves - wrongly in Neil's view.

- Neil touched on this further in Thursday's Asked & Answered video. In case you missed it, you can watch it here.

- Two areas stand out for additional disinflation from here.

- Used car prices are likely to decline in the months ahead as the Manheim Used Vehicle Index has declined 8.4% SAAR over the last 3 months. The Black Book Used Vehicle Retention Index has slid 11.5% SAAR over the same period. These indicators measure wholesale auction prices which tend to lead CPI measure by roughly 3 months.

- Housing rental inflation is likely to ease. Zillow's Observed Rent Index has moderated to 2.6% YoY in October. According to ApartmentList, rent prices are down 0.9% YoY, a sign of weakness in multi-family housing.

- Used car prices are likely to decline in the months ahead as the Manheim Used Vehicle Index has declined 8.4% SAAR over the last 3 months. The Black Book Used Vehicle Retention Index has slid 11.5% SAAR over the same period. These indicators measure wholesale auction prices which tend to lead CPI measure by roughly 3 months.

- The NFIB Small Business Sentiment Index declined to a six-month low of 98.2 in October. Considering the drop in consumers' sentiment in November, it is reasonable to assume that small business sentiment likely deteriorated further into Q4.

- Plans to increase employment slid 1 point to 15, unchanged since May 2024. The percentage of firms with positions not able to fill stood at a cycle low of 32. Small firms also reported a spike in those listing "quality of labor" as their single-most important problem; however, there was no increase in businesses with few or no qualified applicants for job openings.

- Normally, these two series move in the same direction.

- Plans to increase employment slid 1 point to 15, unchanged since May 2024. The percentage of firms with positions not able to fill stood at a cycle low of 32. Small firms also reported a spike in those listing "quality of labor" as their single-most important problem; however, there was no increase in businesses with few or no qualified applicants for job openings.

- Net share of owners reporting higher earnings this quarter fell 9%, the biggest one month drop since the pandemic.

- Additionally, the net percent of small firms expecting the economy to improve slid to 20. Taken together, this presents a cautionary tale on the US GDP growth outlook.

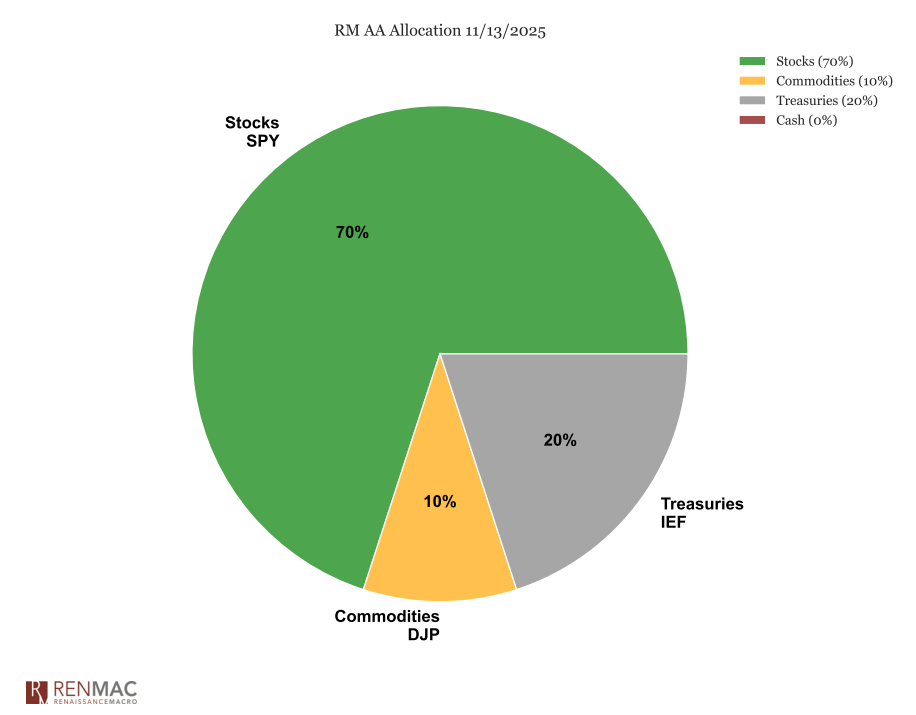

Asset Allocation Model

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

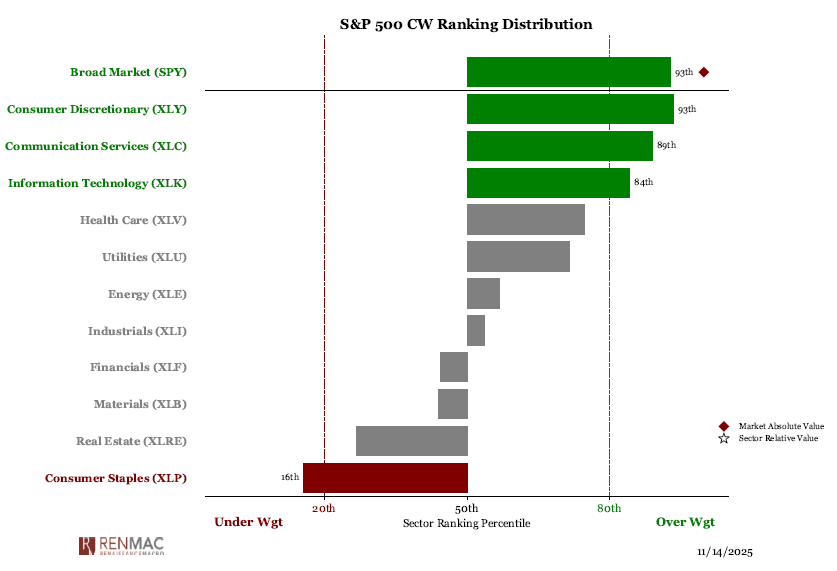

Sector Ranks

Sector Ranks  Chart of the week

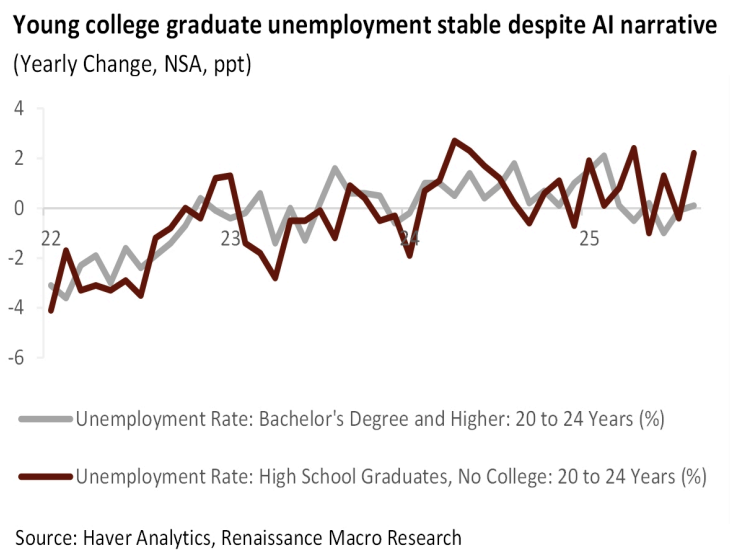

Chart of the week