Research Notes

Strategy

- Internals have softened, but not to the point of bearish proclamation. The recent headlines about breadth are complete nonsense.

- Effective breadth measures are not point in time analysis, but trend analysis. They are not relative performance distinctions, but the totality of the advance.

- If the R2K is in an uptrend, it's a safe bet that breadth figures are decent. Same applies for the EW S&P 500.

- With that being said, the % of issues above their 200-DMA contracting as the market stands right near new highs is not how we would write the script. This tells us we're not in a momentum market, but a trend market. Like a ship, they bend and contort, and make disturbing noises at times, but generally they're sea-worthy vessels that will get you to your destination.

- Apple is quietly emerging from a year's long consolidation, making a fresh 52-week high this week as other tech names like IBM, Google, and a host of system software names do the same.

- Discretionary is making a new high versus staples, but not all discretionary names are performing in unison.

- Hotels, Restaurants and Leisure had a negative volatility alert Tuesday, failing near the previous resistance. Casinos and Gaming names are also weak with several completing top formations.

- The good news is the weakness in these discretionary names is not coming at the benefit of staples, an important feature of a bull market.

- While Gold's rally has hit bubble territory after excessive inflows and a sharp run-up, we're seeing different trends in other metals.

Economics

- "Food away from home" inflation is considered a useful measure to gauge underlying price pressures because it better reflects demand-side influences such as wages, benefits, other service sector costs, and most importantly consumer demand for dining out. In September, food away from home CPI rose just 0.1% MoM and is at a 2.8% annualized pace for the last 3 months, the weakest pace since October 2024.

- Comments from corporate earnings calls support the idea of fading price pressures in restaurants.

- Restaurants lack pricing power at the moment, supporting the notion that underlying inflation pressures are cooling.

- Despite lower mortgage rates (-60bps), over the last 20 weeks mortgage purchase applications are essentially flat. The fact that housing is not really doing anything right now suggests that neutral rates are probably lower than widely believed.

- Even with improved affordability conditions, potential buyers remain cautious about their employment prospects.

- The notorious "lock-in effect" that kept homeowners trapped in their low-rate mortgages is finally loosening its grip, which is helping to boost inventory levels across markets.

- The ECB's October bank lending survey showed a surprise tightening in credit standards for business loans, driven by rising geopolitical and trade uncertainty. Loan rejection rates jumped across all categories, while enterprise loan demand remained weak.

- With banks expecting flat business credit demand ahead and fixed investment contributing little to borrowing, the outlook for euro area capital spending looks increasingly fragile, posing downside risks to the ECB's investment forecasts.

- ADP’s new weekly employment indicator shows modest job gains—about 14,000 per week through mid-October—too weak to hold unemployment steady. The series complements ADP’s monthly report, offering a timelier read on private-sector hiring trends.

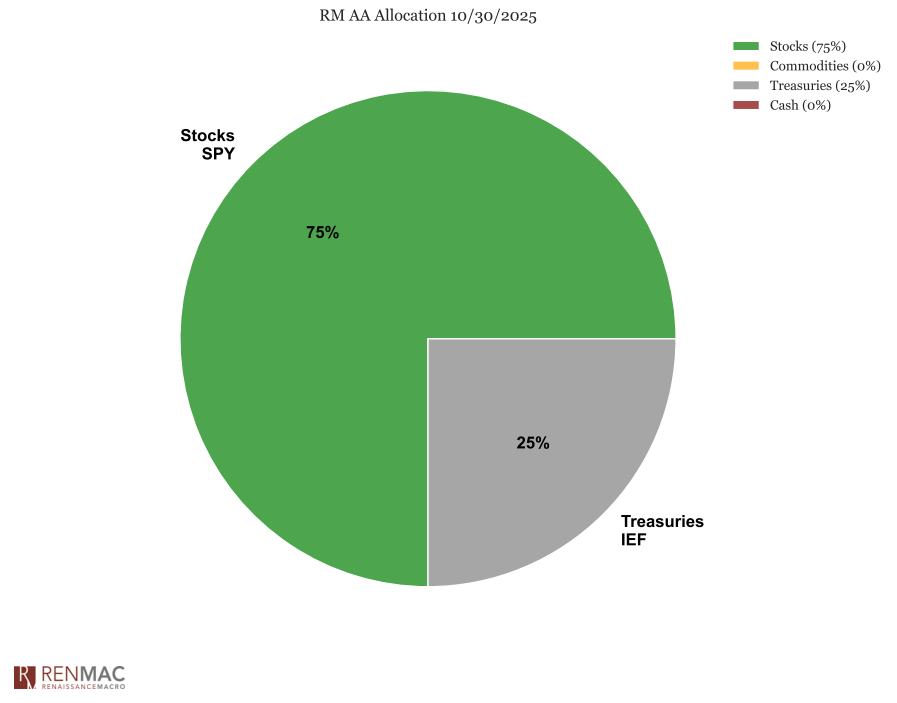

Asset Allocation Model

Why we’re marginally increasing equity exposure

Given seasonal biases and the likelihood of short-term rate contraction, we’ve incrementally increased equity exposure by 5% to capture the short-term probability. It’s tactical in nature, and could come off early next year, but given the current environment and the historical trends, the marginal increase in exposure makes sense in the short-term.

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

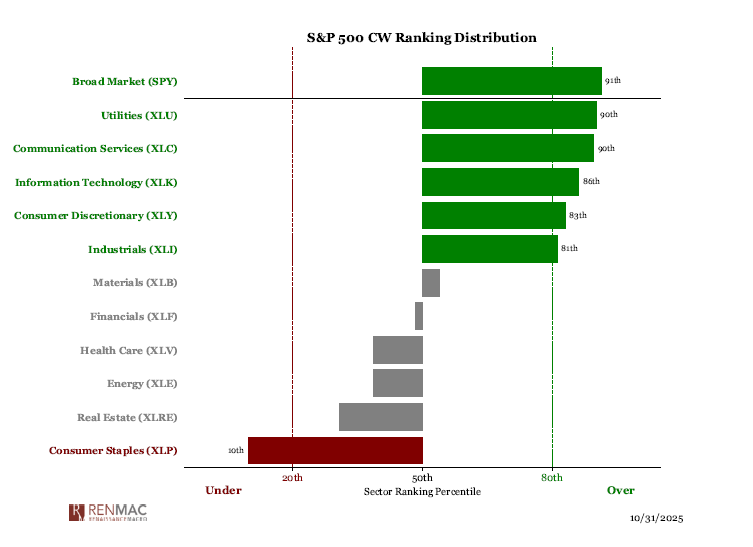

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week