Research Notes

Strategy

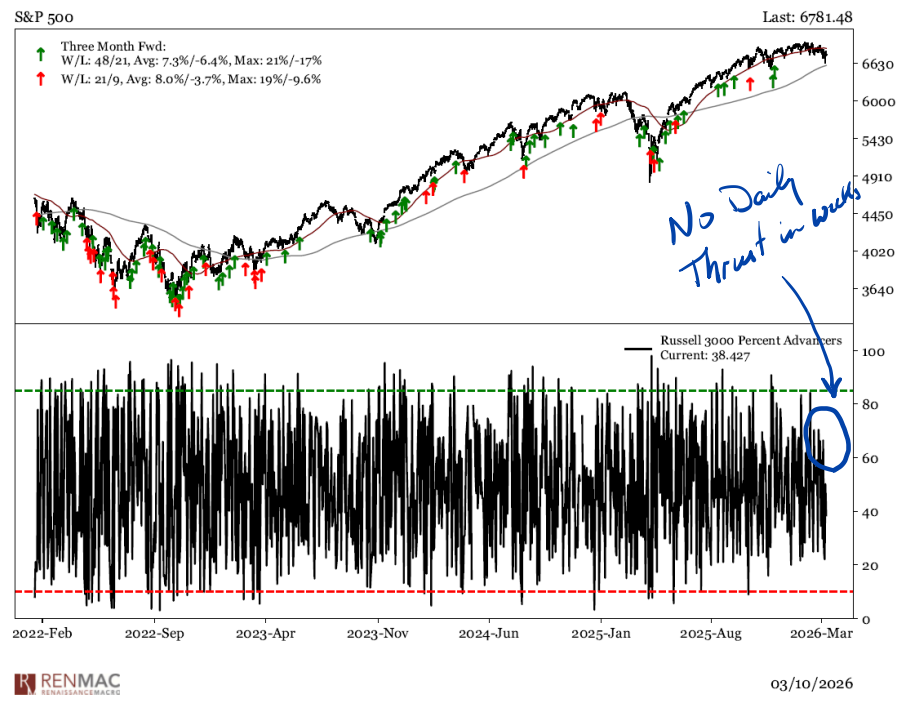

- The % of issues above their 20-day moving average slipped below the 20% threshold for the first time since the taper tantrum, and the same can be said for the net number of overbought vs oversold names in the RenMac oscillator.

- Those are internal oversold conditions. What we're missing are external oversold conditions and signs of stress in the system.

- Those are internal oversold conditions. What we're missing are external oversold conditions and signs of stress in the system.

- Latest sentiment surveys improved, but not enough to make an outright contrarian call. The surprising number came from Consensus Inc data regarding % of Bulls in Crude Oil. The number was a paltry 56% given the move with a t-stat of -1.97.

- Nothing "has to happen" in markets, but certain conditions are more favorable than others for advances vs declines, higher crude bulls would make us more comfortable with our call that Monday's intra-day reversal help set the front-month peak. We'll see.

- Materials are now oversold in an uptrend and look like a decent use of funds from extended energy names (source of funds). Trends in both are bullish, but one oversold and the other overbought is a late cycle "no brainer" at the margin.

- See this ~3 minute video from Jeff on energy.

- MSCI ACWI (Ex US) responded to the recent oversold condition as did most of the Asian/Pacific indices. That's good news and supports the uptrend call.

- European banks responded bullishly to the overall oversold condition in STOXX 600, with several positive volatility alerts out of oversold conditions developing.

- Here in the U.S. we saw relative strength lows in a handful of consumer finance names with Wells Fargo representing banks.

- Overall banks remain in uptrends, but consumer and asset managers are under continued pressure.

Economics

- In February, consumer prices met consensus expectations. Headline CPI rose 0.3% following a 0.2% increase the month prior. Excluding food and energy, prices advanced by 0.2%, rising 2.5% over the last year. Two things worth noting: 1) CPI was on an improved track ahead of the conflict with Iran, 2) There is an increasing wedge between CPI and PCE as shelter inflation cools. The Fed cannot ease when PCE inflation data look worse, and in that sense while Wednesday's data is encouraging on the surface, it may well push the Fed off a little bit further.

- Tariff linked measures like core goods CPI has climbed just 0.6% SAAR over the last 3 months.

- Services less energy services rose 0.3% in February, or 3.3% SAAR. Together, our blended index of primary and owners' equivalent rent just rose 0.2%. Given the continued slide in market-based rents, Neil thinks it is safe to assume cooling rental inflation over the course of the year.

- In CPI, the upward pressure in non-housing services CPI came primarily from medical care service inflation, which rose 0.6%, up 4.1% against last year.

- In short, underlying inflation pressures had been improving in the lead-up to Iran, at least in the CPI. With labor market conditions cooling off, the rise in energy prices will tax US households and that will make it tough for broader inflation pressures to materialize.

- Monetary policy hawks are concerned about second order inflation effects from this latest negative supply shock. Neil understands the concern, but finds them to be unfounded, digging into them below.

- Consumers lack the wherewithal to absorb higher prices. The latest Beige Book noted "most Districts received reports of some firms holding selling prices stable despite higher costs because their customers were increasingly price sensitive". Wage growth is continues to cool as well, implying ongoing slowing.

- Productivity growth has been improving recently. Nonfarm business productivity growth has been close to 3% on average for the last 3 years. Latest data from SF Fed shows a set up in total factor productivity. The important story here is it's tough to worry about negative supply shocks as productivity appears to be strengthening.

- Consumer credit growth remains relatively sluggish. Over the last year, consumer credit outstanding has climbed just 2.2%. Consumers aren't upbeat on the future either, with NY Fed's Survey of Consumer Expectations revealing that consumers see hardest credit availability for the year ahead since may 2025. There is no household credit boom.

- Inflation expectations appear to be anchored. The Atlanta Fed's Business Inflation Expectations Survey shows median expected change to unit costs next 12 months at just 1.9%, right around pre-COVID levels. Households have shown improvement, but we put more weight on firms since they are the price setters and incorporate a wider range of information when forming their views around inflation.

- The inflation risk from the energy shock is less important than the growth shock. Inflation ultimately boils down to a household's budget constraint. As a result, the shock households will feel from rising energy prices will squeeze disposable incomes, forcing spending cuts elsewhere. Businesses cannot raise prices in that environment without feeling a deeper squeeze themselves.

- Neil has been cautious on labor for a while and February's data confirms his priors. February was a bad month, and January was a better month.

- The 3-month average on private payroll employment is 18,000, which isn't good, but is what we have seen for much of the last year. That's why the dial does not shift for the Fed. The labor market is cooling but not collapsing.

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

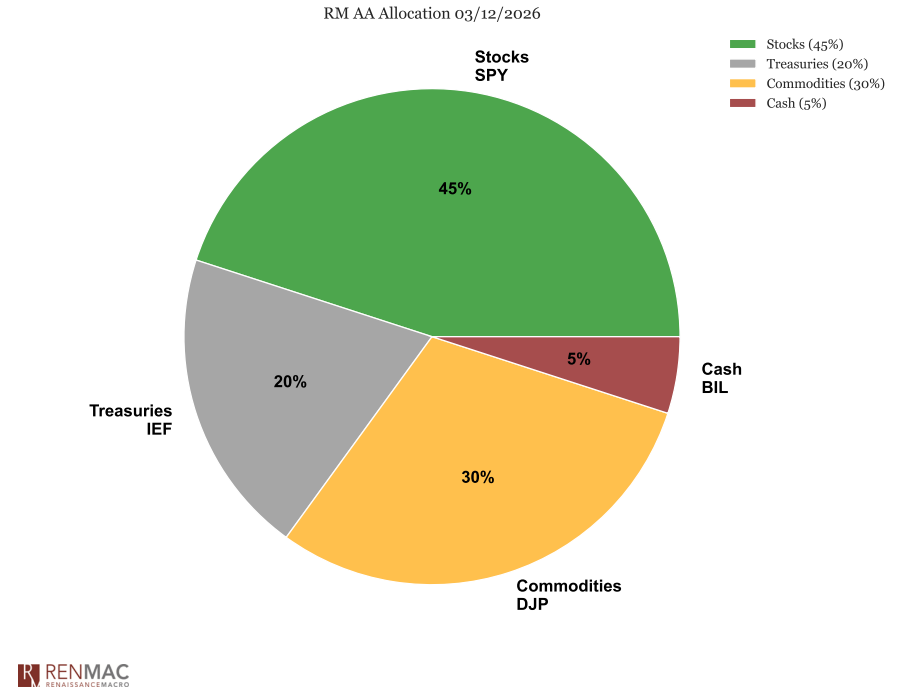

Asset Allocation Model

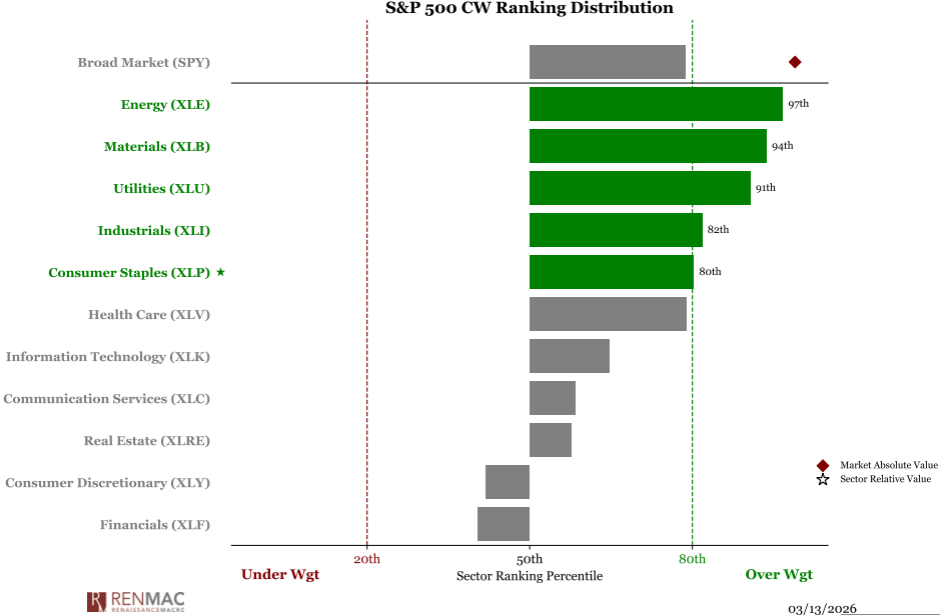

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week