Research Notes

Strategy

- Bitcoin is closing in on our $125k target, but that doesn't necessarily mark the end of the move. Jeff deGraaf shared his latest thoughts on where we are in the cycle, what it means for crypto, and how it could spill over into broader risk assets.

- New highs in the S&P are being driven by more than just price momentum - economic data and earnings are providing real support. So far, 88% of companies have beaten expectations, reinforcing the bullish backdrop.

- As we noted in last week's Advisor's Note (July 12), sentiment has normalized but remains notably below historical norms relative to S&P performance (~+20% over 13 weeks). That disconnect matters.

- The current bull-bear spread sits at ~32%, well below the ~55% we'd expect at this stage. That gap signals under-positioning - and historically, that's been fuel for continued upside.

- The current bull-bear spread sits at ~32%, well below the ~55% we'd expect at this stage. That gap signals under-positioning - and historically, that's been fuel for continued upside.

- Traditionally, rising yields should support a currency - but investors appear more focused on monetization risk and inflation fears. As a result, we're seeing capital rotate into Gold and Bitcoin instead.

- Meanwhile, Yen bulls have surged past 70% for the first time since 2011, even as the Yen weakens alongside rising JGB yields. That divergence breaks with textbook relationships - and speaks to deeper macro uncertainty.

- Raw beta remains at risk, while momentum (beta adjusted) offers opportunity in our view. Seasonal trends support this call.

- The current composition of high-momentum names still tilts cyclical, offering attractive risk-adjusted exposure as we move into a seasonally softer period.

- The current composition of high-momentum names still tilts cyclical, offering attractive risk-adjusted exposure as we move into a seasonally softer period.

- While most investors are brushing off the risk of a U.S. government shutdown, our own Steve Pavlick pegs the odds at 60%. With volatility markets not pricing in that risk, it may be a hedge worth considering.

Economics

- Durable goods prices are rising - no surprise - but consumer services prices are moving lower.

- The narrative that firms are burning off inventory and will hike prices later is gaining traction, but Neil Dutta isn't convinced. If firms truly expected tighter supply, why not raise prices now?

- The narrative that firms are burning off inventory and will hike prices later is gaining traction, but Neil Dutta isn't convinced. If firms truly expected tighter supply, why not raise prices now?

- The bigger issue may be growth, not inflation. Slower gross labor income is meeting firmer prices - and consumers are pushing back. That dynamic points to weaker sales, not higher margins.

- Initial jobless claims fell for a fifth straight week to 221K, and continuing claims have stabilized - suggesting steady unemployment into July.

- Retail sales beats on the surface, but real consumption told a different story. Control group sales rose 0.5%, but with core goods CPI up 0.6%, categories like furniture and recreation likely saw real declines. Nominal spending is cooling - 3m/3m annualized retail growth is just 2.2%.

- We analyzed historical stretches since 1960 where nominal GDP growth underperformed the 10yr yield for more than a year - only 6 such episodes exist.

- The current gap - 241 bps - puts us in rare territory.

- Surprisingly, these periods haven't been disaster zones for markets. 4 out of 6 delivered positive returns. This cycle may rhyme more than it repeats.

- If implementing a dovish shift in policy is the goal while persuading people around you to your cause, then Governor Waller is showing once again why he is best suited for that role.

- We recommend reading Waller's speech for more, and you'll find nuggets in there such as...

- His reservations on labor market

- Comments on consumer spending and latest Beige Book release.

- We recommend reading Waller's speech for more, and you'll find nuggets in there such as...

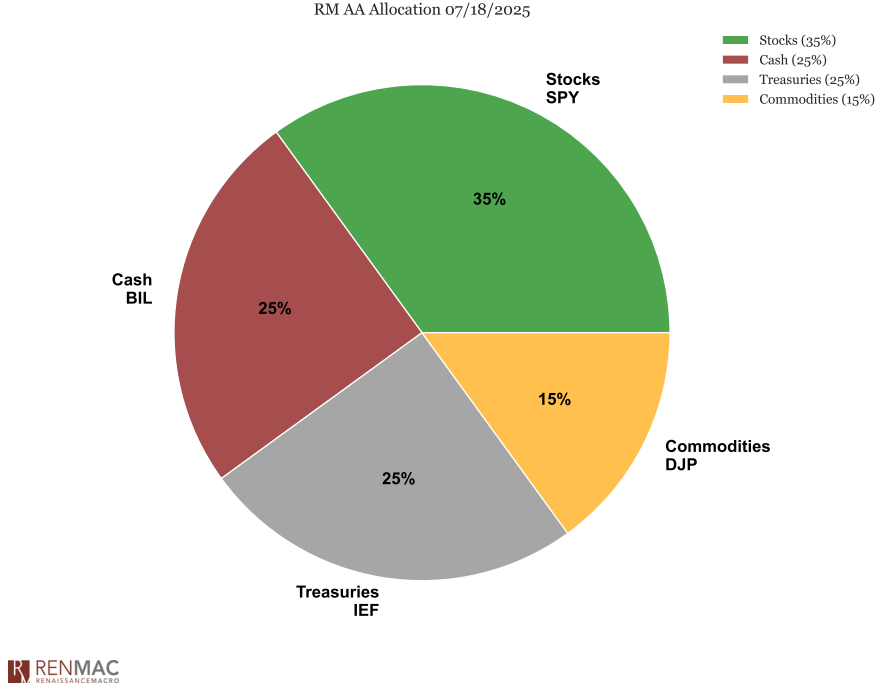

Asset Allocation Model

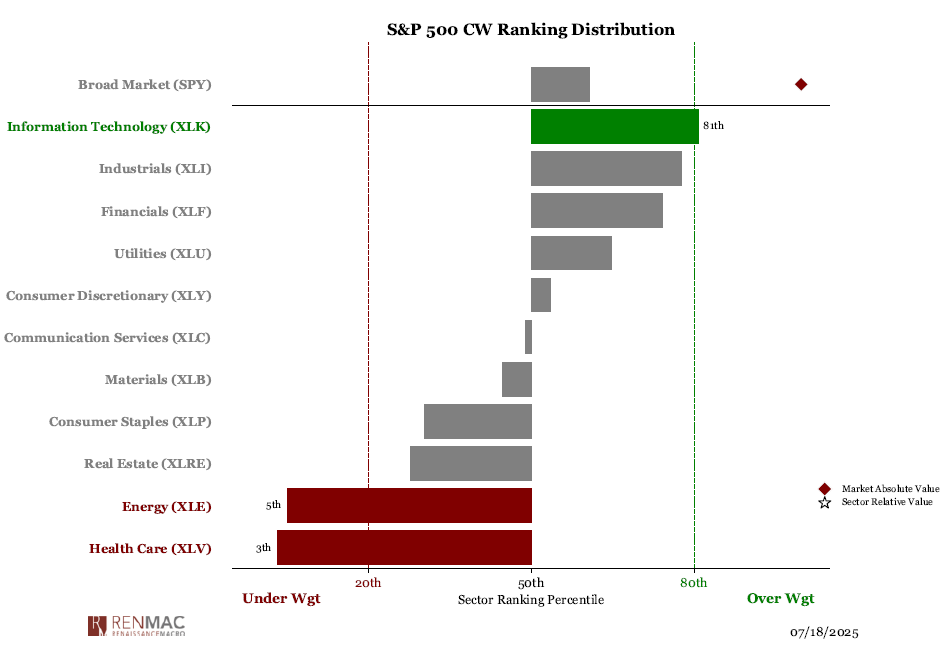

Sector Ranks

Sector Ranks  Chart of the weekA popular view is that the step up in immigration enforcement is leading to a tightening of the labor market as supply of workers dries up. If this were the case, Neil would expect wage growth to rise in those industries where undocumented immigrants make up the largest share of the workforce, but wage growth in areas like construction lag broader market.

Chart of the weekA popular view is that the step up in immigration enforcement is leading to a tightening of the labor market as supply of workers dries up. If this were the case, Neil would expect wage growth to rise in those industries where undocumented immigrants make up the largest share of the workforce, but wage growth in areas like construction lag broader market.

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week