Research Notes

Strategy

- Wednesday’s new S&P high was driven by only 16% of names making 20-day highs. Internally things are soft and rotating, with constituent correlation hovering near lows for this bull-market cycle.

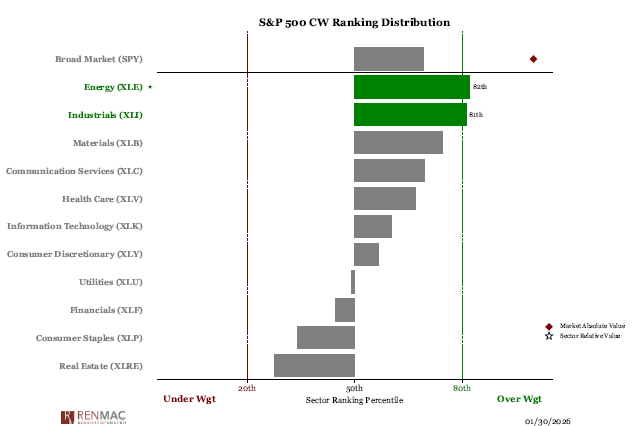

- The highest percentage of names above their 20-day moving average are found in energy; last month the group had the lowest percentage above their 20-day.

- We’re seeing bullish moves in the equities as crudes downtrend remains well-established but currency shifts create a “hard asset” characteristic through reserves and cash-flows.

- The dollar broke with White House comments and rumblings of a coordinated support of Yen. There’s a potentially destabilizing force at work here for risk assets as Yen appreciation draws liquidity away from higher yielding countries.

- Click here for a ~5 minute video from Jeff on this.

- Gold and silver have been beneficiaries of Fx uncertainty, but modest changes in trends, especially against the crowd, can have outsized impacts.

- We see gold and silver as vulnerable to U.S.- Japanese intervention as it changes the trajectory and introduces optionality against “one-way” bets. It may not be a 50/50 proposition, but the payoff skew is steep enough to make it a hand better than pot-odds.

- The 150-160 range USDJPY is the historic intervention zone where Yen weakness becomes uncomfortable for the Ministry of Finance.

- Currently, the jaw-boning has been enough to discourage Yen bears, but interestingly, the Consensus Inc data does not show extreme sentiment in either direction.

- Where we do see extreme bullishness is in silver where bulls have reached their highest levels since 1998 when $7.50/oz created enthusiasm similar to today.

- Industrial metals index made a decisive breakout high with copper leading the charge. Unlike precious metals, most industrial metals and their corresponding equities are emerging from base formations, not on stilts like their precious metal cousins.

- Chinese material names which have been leading since mid-summer are getting parabolic, but also confirming that the trend is global, and not specific currency related (unless it’s a broad repudiation of fiat).

Economics

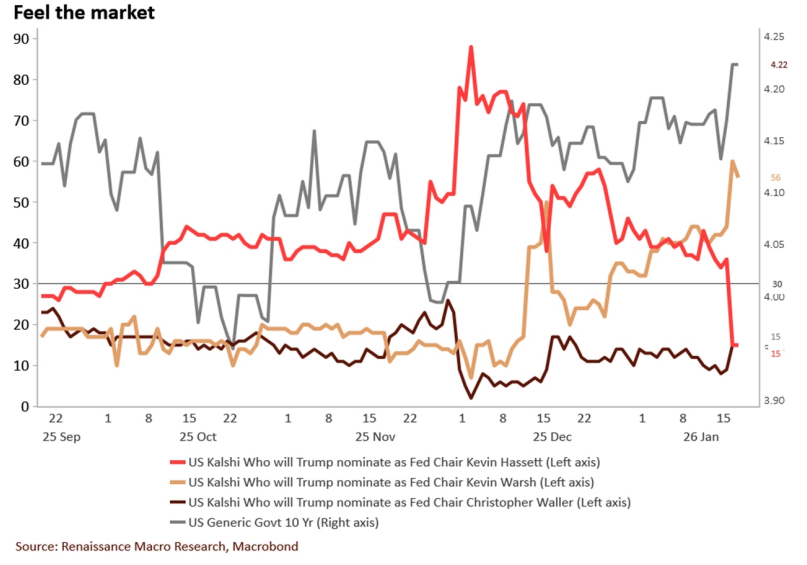

- Neil does not like the pick of Kevin Warsh for Fed chair. The upshot here is that the Fed is bigger than one person and Neil thinks Warsh will have a tough time being able to persuade his colleagues to a dovish position, a position that elevates employment risks over inflation and one he has never been able to make himself, even when the times demanded.

- Warsh has been a policy hawk his entire life, making his newfound dovishness looks very suspect - Powell may suspect the same thing, which is why there is risk of him sticking around. If he does, Warsh would be a very weak Fed Chair (though he would likely be a weak Chair regardless).

- Part of Trump's appeal is his method of handling the economy and that he is supposed to be "the greatest jobs President that God ever created", making the Warsh nomination perplexing. Someone that saw inflation as the prevailing threat during the GFC with unemployment > 10% and tightening financial conditions lacks the judgement to lead the Fed. Everyone makes bad calls, but Warsh's mistakes always go in the same direction.

- Neil believes the post FOMC meeting press statement was hawkish. The upgrade from "Available indicators suggest that economic activity has been expanding at a moderate pace" to now "solid pace" is particularly interesting since not much has changed from December to January.

- At this point, the way to think about the Fed is that if they are easing before June, something bad has happened in the economy.

- Neil sees no chance the Fed hikes this year, and sees 3 potential outcomes with him thinking #3 is most likely, and #1 is very unlikely.

- No cuts at all - strong growth tightens labor market, leaving inflation stuck in place and making it difficult to push through even 1 cut.

- Goldilocks - economy holds up, inflation continues sliding, Fed calibrates policy accordingly, cutting a couple times.

- Fed misreads the economy - unemployment climbs, growth is weaker than expected and inflation slows. In this case, Neil sees cuts at every meeting in 2H2026 (100bps total).

- Neil remains concerned about the labor market outlook, but sees both sides. Neil does not think the labor market is recovering, but the pace of slowing has eased.

- Bad: Consumer attitudes about labor market continue to sour. The breadth of employment growth has been quite weak with private employment ex healthcare and social assistance negative since April.

- Good: Unemployment rate slid in December, initial claims remain low, and continuing claims no longer rising.

- There are 3 primary conduits for upside inflation risks: labor, housing, and energy.

- Labor's pricing power is declining. If immigration enforcement were tightening the job market, wage growth would be accelerating but it's cooling. If advertised pay in job postings is slowing, actual wage growth will likely moderate as well, taking pressure off non-housing services inflation.

- Housing rental inflation is disinflating. Market-based measures of home rents are cooling, and as we know there is a large lag between market-based rents and official measures. We estimate that primary and OER rents will slow to roughly 2.1% by year-end, which would by itself knock 0.21% off core PCE.

- CPI captures all occupying renters, while market-based is currently on market.

- Energy prices have been restrained in the aggregate, rising ~2% over the last year which should help grocery prices as well as diesel prices have declined.

- Atlanta Fed's Business Inflation Expectations Survey show expectations at 2% for the next 12 months.

- We follow expectations because there may be a link to wage negotiations - if people see higher prices, they'll demand higher wages, setting off a feedback loop, however in today's economy the connection between inflation expectations and wage pressure looks weak.

- BoC Governor Tiff Macklem recently claimed the status of the USD has been "dented", but Neil respectfully disagrees.

- Using Bloomberg's asset price decomposition model, we see that the dollar's weakness has been driven primarily by a shift in global risk appetite rather than a fundamental reassessment of US economic prospects.

- As fears of a tariff-induced recession have faded and policy uncertainty has stabilized, investors have rotated out of safe-haven assets like USD into riskier assets. This same sentiment has been the dominant force lifting US equities as well.

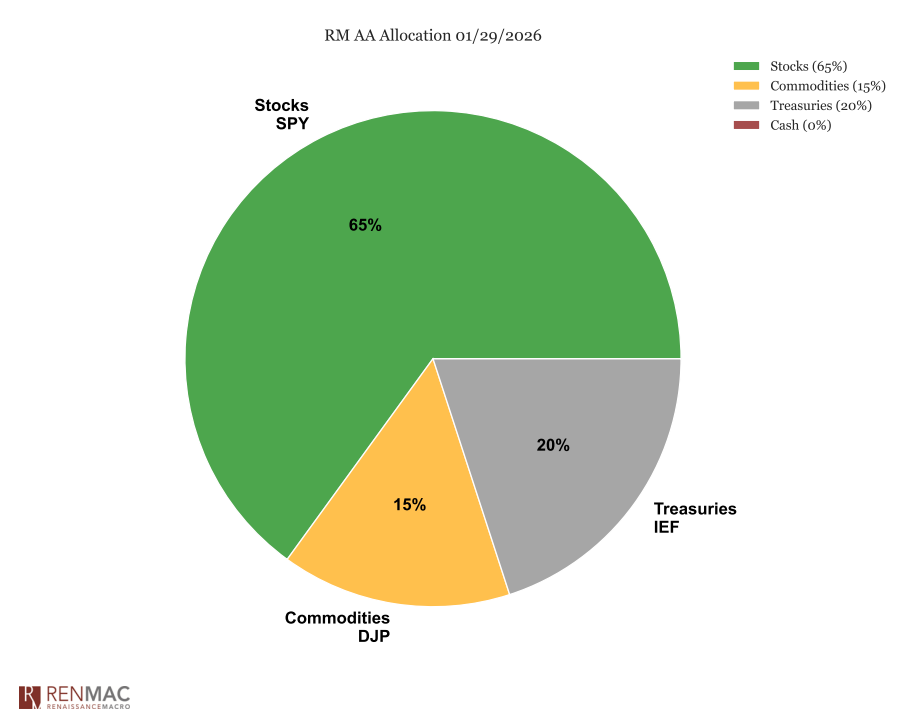

Asset Allocation Model

The shift in our AA model reflects the improvement in energy, industrial metals, and trends in precious metals, though we would warn the parabolic nature of the latter makes them especially high risk of reversals. There is a currency debasement trade permeating markets, Japan is a epicenter of this and their snap elections on Feb 8th will influence the sustainability of these trends and potentially create a source of near-term volatility.

The shift in our AA model reflects the improvement in energy, industrial metals, and trends in precious metals, though we would warn the parabolic nature of the latter makes them especially high risk of reversals. There is a currency debasement trade permeating markets, Japan is a epicenter of this and their snap elections on Feb 8th will influence the sustainability of these trends and potentially create a source of near-term volatility.

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week