Research Notes

Strategy

- The Russell 2000 index has had a good run, but neither our excess return model nor our ETF flows indicate that there’s even an elevated risk of a tactical retreat.

- This is a breakout and relative performance turn that is slow to gain acceptance and far from the exuberant level that gives us pause, lean in.

- 2yr yields are close to resistance at 3.63%, but a long-way from changing trend. Regardless, banks are taking the consternation in yields in stride as the Regional Bank ETF (KRE) broke to a new 52-week high as internals confirmed the move.

- Gold’s risk-adjusted performance is rivalling 1980. It is rarified air, but the risk-adjusted relative returns to silver make it look reasonable compared to the “Devil’s Metal” (i.e. silver is even nuttier).

- Calling tops is a fool’s errand, but putting returns into perspective keeps your feet on the ground.

- If you’re playing, know that you’re playing in a bubble-environment with high probability of +30% drawdowns in the blink of an eye.

- Our commodity allocation is focused more on the industrial metals than the precious metals. The former can be dollar cost purchased while the latter should be dollar cost sold, as they’re vulnerable to correction

- JGBs bear watching but are not flashing crisis signals yet: default risk remains low, the BOJ controls roughly half of issuance, and capital flight risks appear manageable.

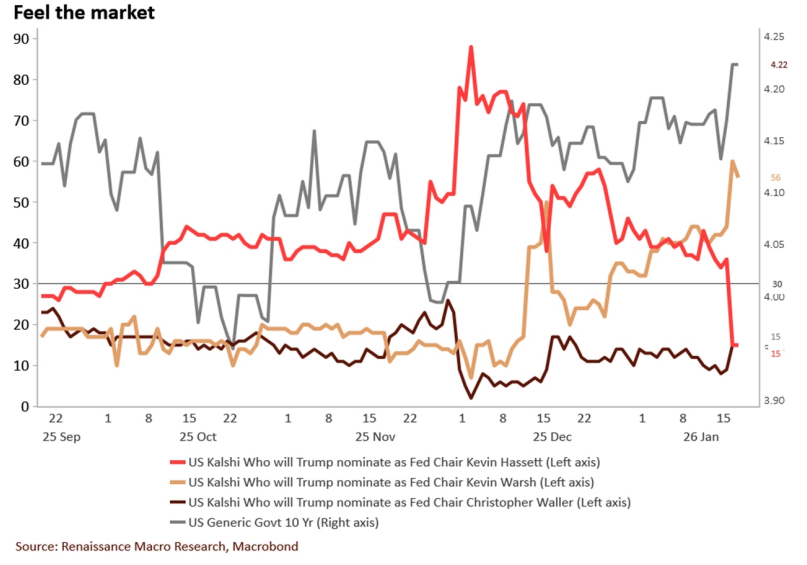

- Markets are pricing a potential BOJ policy shock in February, with gold strength and bitcoin weakness hinting at central banks reallocating capital amid currency concerns.

- While a breakout in long-end global yields would be uncomfortable, current models suggest equities are not yet vulnerable; the cleaner hedge is yen strength and weakness in Japanese exporters rather than betting on a JGB collapse.

Economics

- If the labor market was tightening, wage growth would be perking up, but instead the opposite is true. According to data from Indeed, posted wage growth slowed to 2.08% in December. If advertised pay in job postings is slowing, it stands to reason that actual wage growth will also moderate.

- According to Atlanta Fed's Wage Growth Tracker, median wage growth eased to 3.7% in December, the slowest since 2021.

- Without a pickup in the workweek, this would result in income growth to ease, taking momentum out of consumers' spending.

- Our yield decomposition suggests the 10-year Treasury's decline in 2025 was driven far more by macro and financial conditions than by fiscal or earnings fundamentals.

- The biggest contributors were falling rate volatility, a weaker dollar, Fed easing, and softer growth expectations, all of which worked to compress term premiums and pull yields lower.

- Dollar dynamics, in particular, played an outsized role. The trade-weighted dollar flipped from solid YoY gains early in the year to meaningful depreciation by year-end, creating sustained downward pressure on yields and reinforcing foreign demand at the margin.

- Fed policy amplified these effects, as easing at the front end combined with volatility compression to support lower long-end rates. While foreign investors were net sellers of Treasuries in 2025, the direct flow impact was modest; instead, currency effects were the dominant foreign channel influencing yields.

- Housing demand weakened sharply in December, with pending home sales falling across all regions and the pending home sales index sinking well below its long-term baseline - signaling softer existing home sales and residential investment ahead.

- The S&P 500 slipped in January as rising yields overwhelmed modest support from slightly a slightly lower equity risk premium. Higher Treasury yields compressed equity multiples, while earnings expectations softened at the margin.

- Our model shows the implied equity risk premium near 2% - well below historical norms - suggesting elevated valuations and a less attractive risk-reward profile for long-term investors unless rates retreat or growth expectations improve.

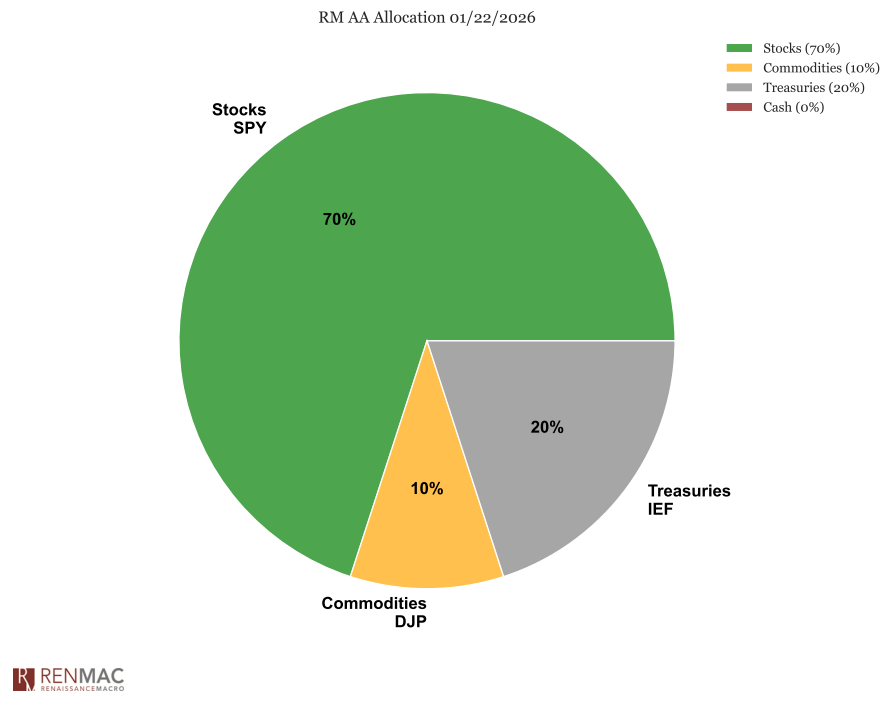

Asset Allocation Model

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

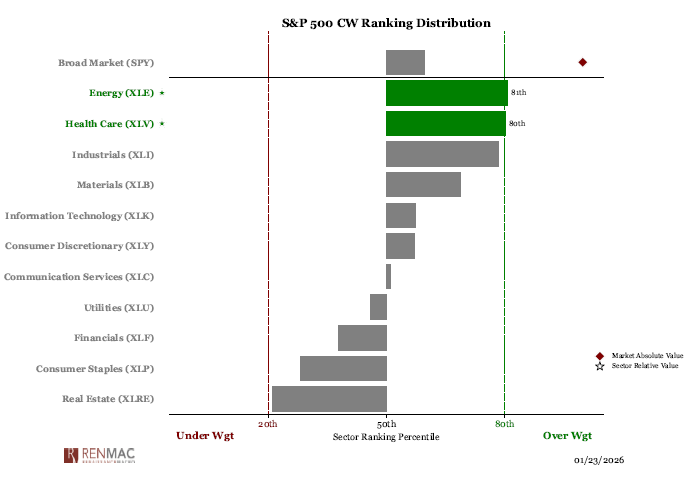

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week