Research Notes

Strategy

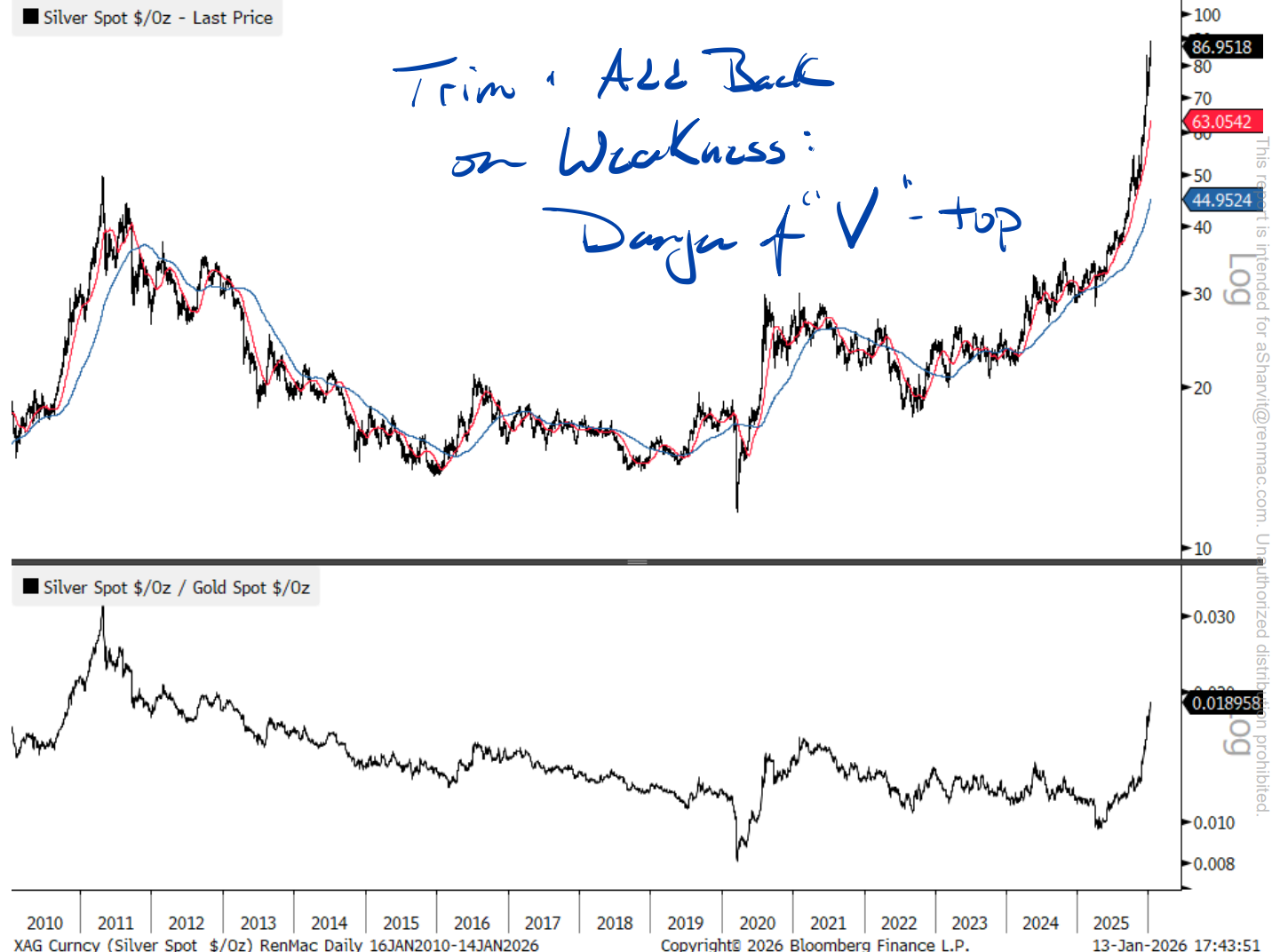

- Silver is parabolic and prone to “V-tops”. Trends are good if you own it, but they are unsustainable.

- We recommend trimming 20-50% positions and look for oversold conditions to develop to play from a position of strength. The timing and pricing are inexact, but the probability of 50% declines over the next 3-6 months are dramatically higher after such events than in normal trends.

- The Russell 2000 continues to impress as it’s now up roughly 7% to start the year and is breaking out to new 52-week relative highs vs the Russell 1000 on a cap-weighted basis.

- Strength in small-cap Health

Care and Financials with deterioration in large-cap Tech and Comm. Services is the perfect recipe for Russell 2000 outperformance and we think that rotation still has legs. Small-caps are positioning for a dominant year.

- Strength in small-cap Health

- Consumer discretionary is shaping up favorably, even though the charts haven’t fully confirmed it yet.

- Click here for a short video from deGraaf explaining where we are.

- Click here for a short video from deGraaf explaining where we are.

- Bitcoin is now overbought and challenging the first level of resistance around $98k. The bounce could push higher to the declining 200-DMA but we wouldn’t get greedy as we don’t think the cycle lows are in. If playing for the bounce, we would keep stops tight.

- Homebuilders turned bullish for us about a month ago. It was an uncomfortable call, and remains questionable, though supported by our market cycle clock.

{kind=link}

Economics

- Labor productivity growth has been quite robust in recent quarters, sparking many to conclude we are in a strong boom. Neil highlights a few points:

- Productivity has ebbed and flowed since the pandemic. There was a strong boom early, followed by a decline. It has now been recovering since 2023, but remains in-line (or modestly above) the pre-pandemic trend.

- In a genuine boom, real compensation growth should be expanding. Typically, with better labor productivity comes an increase in real compensation, but the current administration is well below trendline.

- There is no evidence that compensation growth is about to catch up to productivity. Average hourly earnings for production and non-supervisory workers has climbed just 3.1% SAAR over the last 3 months. The series tends to be more representative and has a strong contemporaneous relationship with the Employment Cost Index.

- The dynamic continuing depends on whether household savings continues to be drawn down. Companies cannot indefinitely expand margins by squeezing labor.

- Institutional Investors are not a major driver of housing unaffordability, owning less than 1% of U.S. single-family homes nationally and just 2.6% even in the most concentrated state, according to recent AEI research.

- Housing affordability problems long predate institutional buying, with price-to-income ratios exceeding sustainable levels in major markets like California and New York as far back as the 1990s, well before large investors entered the market.

- The primary constraint on affordability is limited housing supply driven by restrictive zoning, slow permitting, and land-use regulations; AEI argues that reforms enabling by-right zoning and faster approvals would have a larger impact than restricting institutional ownership.

- As a result, proposals to limit institutional investors are unlikely to materially improve affordability, as they target a marginal part of the housing market rather than the supply shortage.

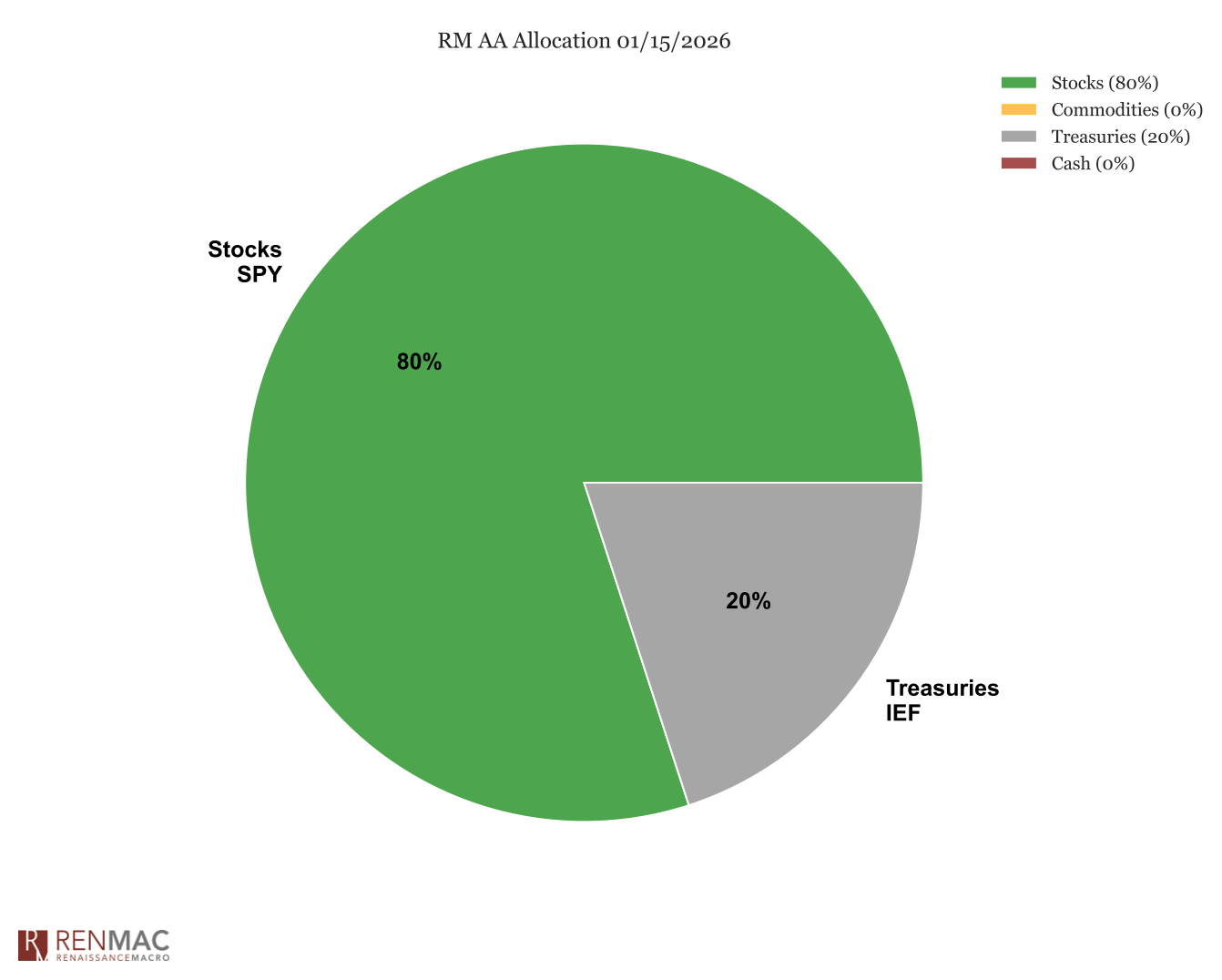

Asset Allocation Model

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

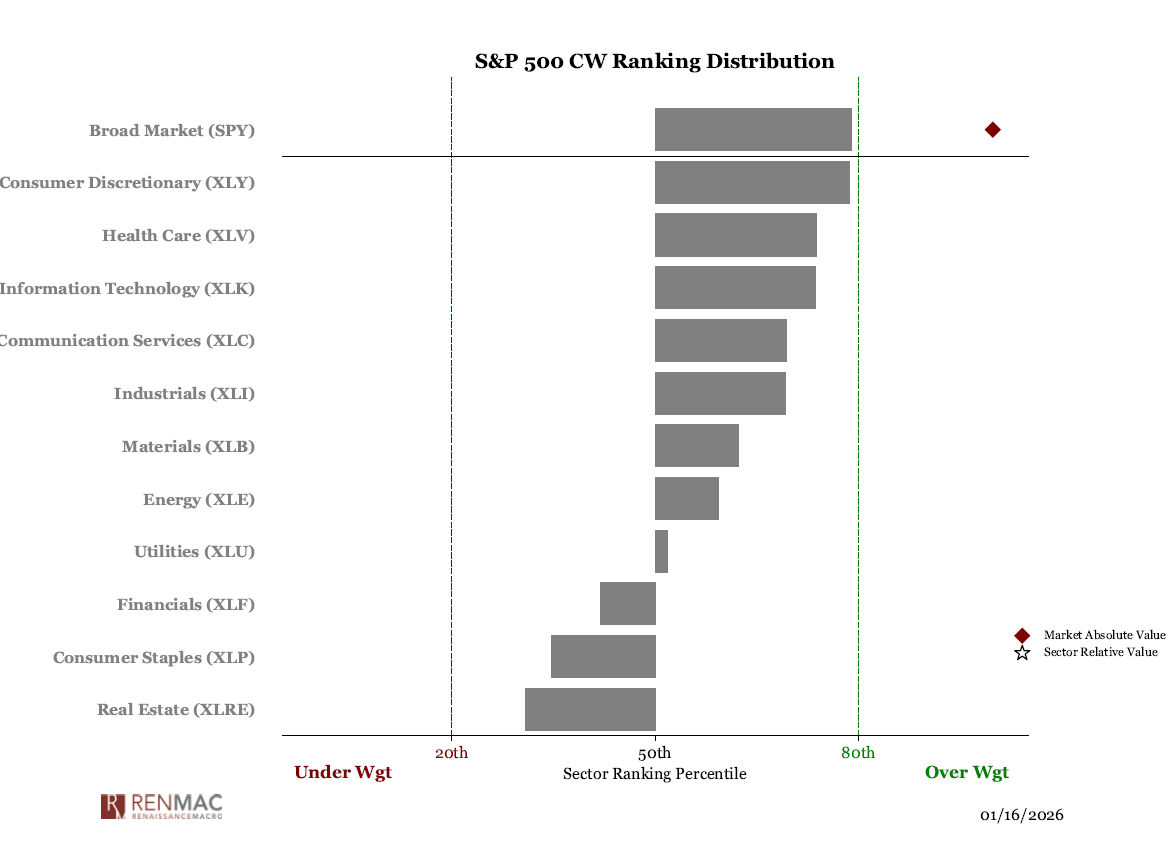

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week