Research Notes

Strategy

- The expansion in 52-wk highs on the SPX is uncharacteristic of a bear market's beginning. This is a "reality-shock" to tech as blue-sky optimism meets the realities of priced to perfection.

- Bitcoin is oversold, but still in a downtrend. Don't be lured into thinking oversold conditions in downtrends are long term bottoms, they rarely are. Any rally should be considered counter-trend in nature.

- Equal-weight Russell 1000 Tech has now dropped to multi-month relative lows vs the broader equal-weight index.

- You can couple that with software oversold condition, but only in the context that it pairs well with high momentum semi's.

- The relative performance of the Russell 1000 Value vs Growth is flagging as a golden-cross confirming a bullish relative trend change.

- While the Q1-Q5 65-day return of the R1K Value factor is now in the 96th percentile, R1K Growth has now dropped to just the 1st percentile (highest and lowest readings since Covid).

- While we are bullish on value, the rotation from growth into value is clearly stretched and we would look for at least some tactical reversion.

- The energy sector continues to build momentum and once again led the market Wednesday. The strength is broad based as 100% of issues are above their 200-DMA's.

- The relative trend of Energy vs the broad index tends to track the price of crude and while crude is in a downtrend, there is still room to the upside until the next level of resistance around $72, so we would expect more outperformance for Energy in the near-term.

- The current zone on the market cycle clock tends to be good for two-year yields going down.

- Jeff put together a quick video on what is going on with Gold & Silver.

Economics

- Wednesday's ADP announcement showed a jobs gain of just 22k, well below consensus estimates of 45k and following a downwardly revised 37k gain in December. Without education and health services, the private sector contracted.

- Mid-sized businesses (50-499 employees) accounted for all the net job creation, while small firms showed no change and large employers cut jobs.

- Layoff announcements have perked up, though how much this translates into hard data remains to be seen.

- According to Challenger, ex-government/nonprofit layoff announcements jumped in January, trending up over the last 6 months.

- Meanwhile, hiring intentions remain sluggish, with announced hiring plans declining 12.9% against the same month last year, following a holiday season of lackluster hiring. Layoff announcements are up, hiring intentions are down.

- Job openings tumbled to 6.542 million in December, down 386k from November and nearly 1 million lower over the year.

- We are operating on the flatter part of the Beveridge Curve. If openings continue sliding from here, unemployment will rise more quickly. Unlike mid-2025 when conditions were merely flat, the December data points to a labor market where demand is actively cooling.

- The January ISM Services report held at 53.8, but the stability masks softening fundamentals.

- The headline was propped up by longer supplier delivery times, while new orders, employment, and export demand weakened meaningfully - most notably a sharp drop in export orders that may reflect early trade-policy effects. At the same time, prices paid rose to a three-month high, underscoring sticky services inflation.

- Overall, the internals paint a less constructive picture than the headline suggests, with slowing demand and rising cost pressures.

- January core PCE is likely to look hotter than the underlying inflation trends imply.

- Historically, January prints run about 1% above the full-year norm due to residual seasonality, meaning a ~3% annualized reading would largely reflect noise rather than true reacceleration.

- This year, however, tariff cost pass-through may add some genuine pressure, making it harder to separate seasonal distortion from emerging inflation risks - a key issue for Fed expectations.

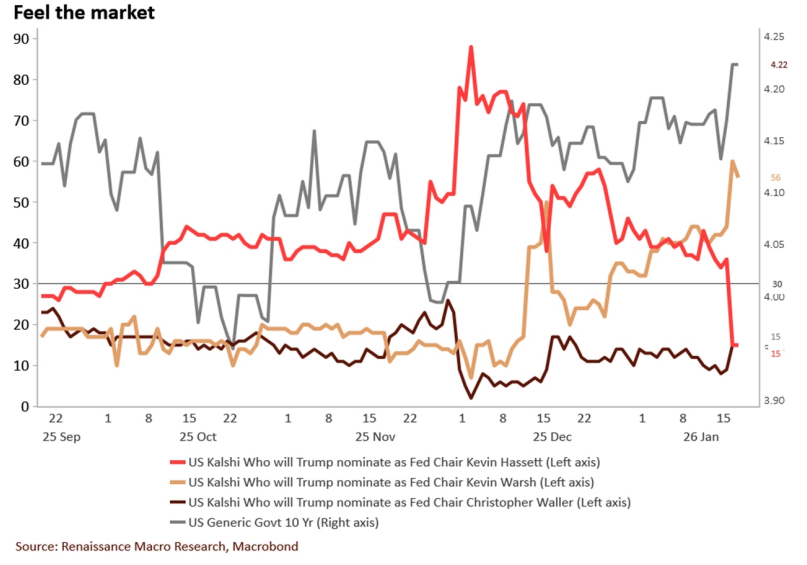

- Leaving the merits of the Warsh pick aside, there are 4 things investors ought to be thinking about right now:

- How long? It typically takes about 3 months to confirm and Senator Tillis has vowed to block any nomination to lead until the DOJ investigation into Powell is resolved.

- Equity stress test: All 4 of Greenspan, Bernake, Yellen, and Powell had selloffs within their first year.

- Communications change: Warsh believes policymakers talk too much. His belief of the Fed being too reliant on forward guidance and the fact that he never really gave speeches on economic and policy outlook when he was Fed Governor implies less discretion and more of a rules-based approach to policy. This approach works in normal times, less so during times of elevated market and economic uncertainty.

- Curious timing: We ran an index rating Warsh's public commentary over the years to determine hawkishness or dovishness. A higher score is hawkish and lower is dovish.

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week