Research Notes

Strategy

- With a new month approaching, it’s worth noting that March has historically delivered below-average returns for the S&P 500. The index is also approaching one of its weakest points for 3-month forward returns across the entire presidential cycle.

- In addition, March has typically been the worst month of the year for gold. Although gold remains about 6% below its recent high, the gold miners ETF, GDX has just pushed to new highs. Relative strength is impressive, but we prefer to see the metal confirm with a breakout.

- March has historically been the strongest month of the year for REITs, and the group is currently entering one of its most favorable 3-month forward return windows of the presidential cycle.

- The spread between Tech High Beta (semis) and Low Beta (software) has reached the 100th percentile, while Tech High Momentum sits in the 99th. We lean with momentum but extremes like this are typically where we begin looking the other way. At these inflection points, the dispersion between "good" and "bad" charts tends to compress i.e. we'd adjust risk accordingly and wouldn't be pressing software shorts.

- In 2000, Tech Beta peaked roughly 3 months before Momentum (software in that case) rolled over, with the NDX breaking a few weeks thereafter. It unfolded as a process, not an event.

- Comm Equipment and Semis created double tops before rolling. The question now is whether we are tracing a similar arc and if so, where are we within that progression.

- In this 10min video, Jeff deGraaf discusses this topic: Tech Bubble: Then and Now

- Aerospace and defense names are close to making new absolute and relative highs. They are one of the leadership groups within industrials, and while our SERM ranking for the industrial sector is in the “uncomfortable” territory the trends remain bullish. Aerospace and Defense SERM readings are not yet excessive, so we’re not fading this trend at this point.

- As the S&P churns in search of a narrative, the MSCI world index (Ex U.S.) quietly makes another high. EM is on a tear, with Taiwan and Korea nearing bubble levels thanks to their chip dominance

Economics

- Growth is respectable, but the data aren’t consistent with an economic boom. Underlying activity is consistent with growth just above two percent.

- There is no evidence, at least not yet, that productivity is taking off. Trade data has been distorted by tariff-related swings. Firms rushed to front-load imports ahead of new tariffs, widening the trade deficit, and then pulled back — creating noise that likely adds costs. While tariffs could improve the trade balance over time, the process will be slow given policy uncertainty and the difficulty of shifting production to the U.S.

- To gauge underlying growth, it’s better to focus on core measures. Private final sales to domestic purchasers rose 2.4% in Q4 and slowed modestly in 2025, while GDP Plus came in at 2.1% and has been trending lower. Overall, growth in Q2–Q3 was likely overstated, with underlying activity closer to 2% than 3%.

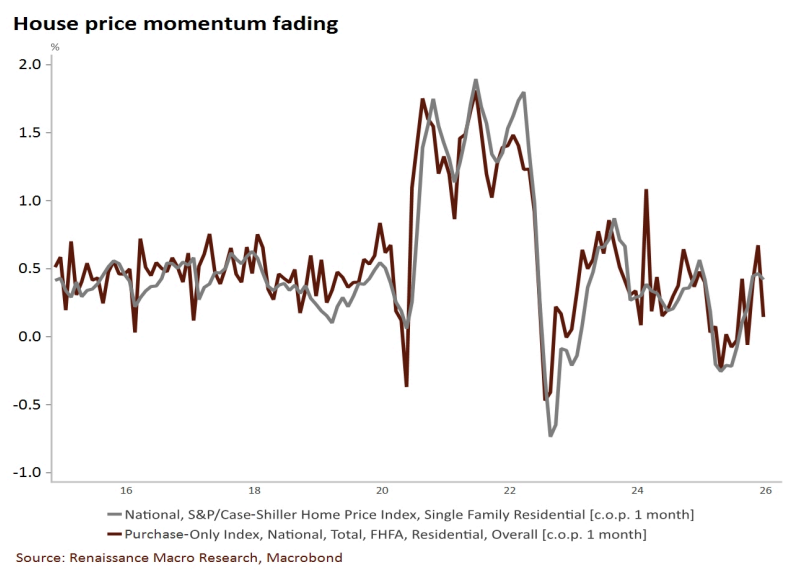

- We've seen some enthusiasm creep into housing with residential construction employment climbing in January, 3 consecutive months of single-family starts advancing, and new home sales strengthening but Neil still doesn't believe the story has changed:

- Housing activity may have gotten ahead of itself late last year. Building permits have stalled, homes sold but not yet started are down 25% from a year ago, and builder sentiment remains weak with soft buyer traffic in February.

- Residential construction will remain under continued downward pressure because housing starts are running below housing completions.

- Manufacturing has seen renewed optimism. There's been an uptick in manufacturing production, the ISM Manufacturing PMI has climbed, transportation activity is said to be advancing.

- The tech capex boom is an important driver of factory output. There has been strong growth in computer & electronic products and batteries as well as industries adjacent to AI data-center build out. Worth noting that real investment in data-centers has been easing over the last year.

- Importantly, the 3 main end markets for US manufacturing are quite soft...

- Household goods consumption has been flat for the last year.

- Residential construction and related manufacturing will face a sustained headwind as the pipeline drains.

- Export activity is soft in the face of trade policy uncertainty and sluggish growth across our major trading partners.

- The tech capex boom is an important driver of factory output. There has been strong growth in computer & electronic products and batteries as well as industries adjacent to AI data-center build out. Worth noting that real investment in data-centers has been easing over the last year.

- Jobless claims still point to a stable labor market. Initial claims remain low, and continuing claims have edged down YoY.

- However, this contrasts with consumer surveys showing more people say jobs are "hard to get," a measure that has recently tracked permanent job losses more closely.

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

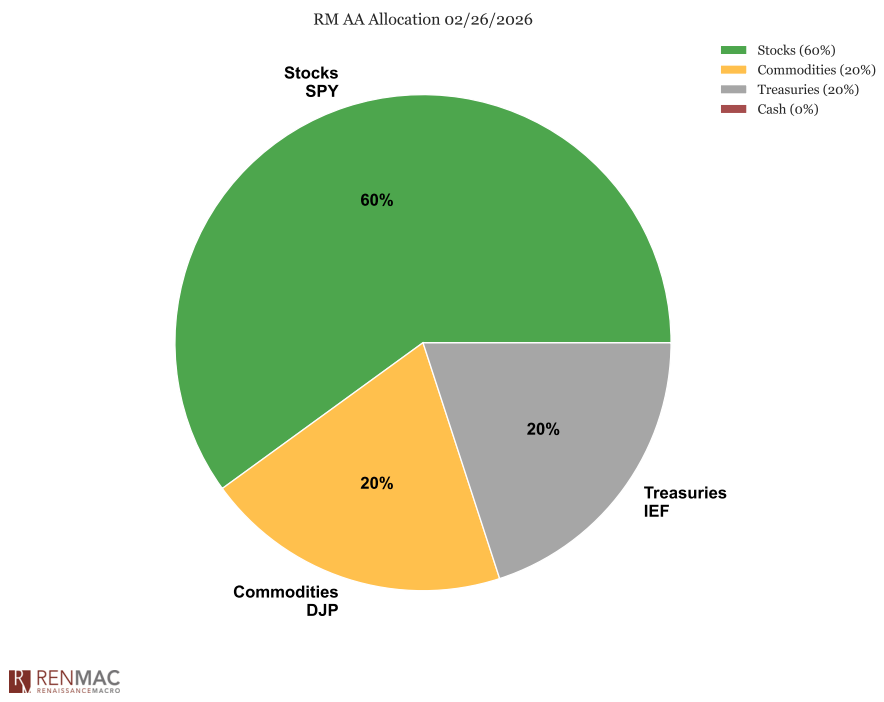

Asset Allocation Model

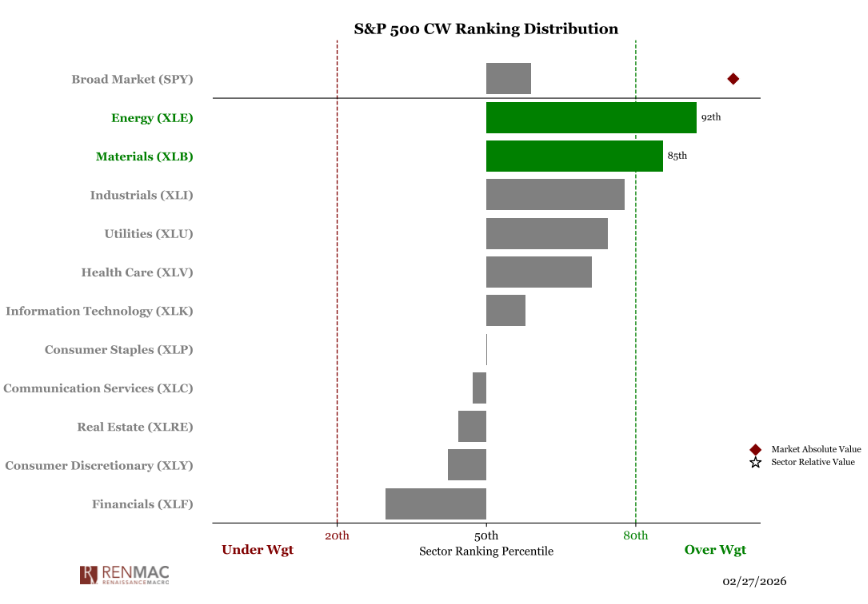

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week