Research Notes

Strategy

- Equal weight Staples sector has rallied briskly off the lows since the beginning of the year, but the rally has failed to change the overall chart.

- Multi-year resistance points loom above current price, confirming no absolute breakout while the relative trend has reverted back to its clearly declining 200-DMA.

- At the margin, we would be selling these names, not buying them. If you're concerned about defense, tilt toward Utilities and HealthCare, they've got more bullish trends supporting them.

- Cyclicals are battling for relative supremacy versus defensives which have come on strong since the beginning of the year. Only Industrials have all 3 relative trend conditions in bullish territory with technology neutral and discretionary bearish.

- Staples and Utilities are overbought, but the latter are in well-defined trends. Staples more vulnerable to overbought conditions because trends remain weak on a relative and absolute basis.

- If Staples ignore the overbought condition, or consolidated vs. correct, it's a bullish development. If they crack and resume trend, it's bearish.

- Crude oil is in a similar set-up with recent strength having little impact on the overall structure of the primary trend. There is resistance in the $70 range, but the downtrend from Sept 2022 remains intact.

- Crude is not overbought yet, but we'd use overbought conditions to be sellers, not endorsers of the strength. Do NOT chase Mid-Eastern conflicts as it is unlikely sustainable.

- Energy equities look better than physical crude, so use weakness to add to energy positions and get equal weight.

- 2yr yields are probing new lows and the softening bond yields are helping push homebuilders higher. They've been bullish in our work since mid-autumn with many just emerging from base formations.

- BDCs and private equity shops that are publicly traded continue to look vulnerable in this tape. Financials rolled over in our work late last year, but most of the weakness is driven by insurance, exchanges, private equity firms and payments.

- Traditional areas that are usually linked to economic health/strain like regional banks and consumer finance continue to be the strongest areas within the sector.

Economics

- Recent FOMC minutes leaned hawkish, but incoming data suggest inflation pressures are easing. Business inflation expectations fell to 1.9%, and wage growth in job postings has slowed to 2.0%, pointing to cooling underlying cost pressures and limited tariff pass-through.

- While activity data remain firm, a durable productivity boom would require sustained upside growth and surprises and stronger real wage gains - evidence for the former is building, but the latter remains lacking.

- Housing starts rose to a 5-month high in December, led by the West and a pickup in multifamily, but single-family permits declined - suggesting the rebound may reflect catch-up activity rather than renewed momentum.

- With completions still running ahead of starts and full-year authorizations down from 2024, the broader trend points to slowing residential investment despite the late-year bounce.

- Pending home sales decline -0.8% MoM in January, missing expectations of a +1.8% gain. While the YoY drop suggests the housing market remains stuck in neutral, despite expanded affordability (lower rates), we have not seen an expanded qualified buyer pool yet.

- The New York Fed survey showed a sharp drop in regional service activity, with business conditions and employment hitting five-year lows even as wage pressures rose.

- Despite slightly improved forward expectations, weak hiring, soft capex plans, and deteriorating supply conditions point to a fragile outlook.

- The Philadelphia Fed's February survey beat expectations, with the headline index rising to 16.3, but the underlying details were more cautious.

- New orders stayed relatively firm, yet shipments nearly stalled and employment weakened, with both headcount and hours worked declining sharply.

- Looking ahead, business expectations improved meaningfully, but capital spending plans were cut in half, price pressures eased, and many firms reported greater customer price sensitivity and ongoing tariff-related headwinds.

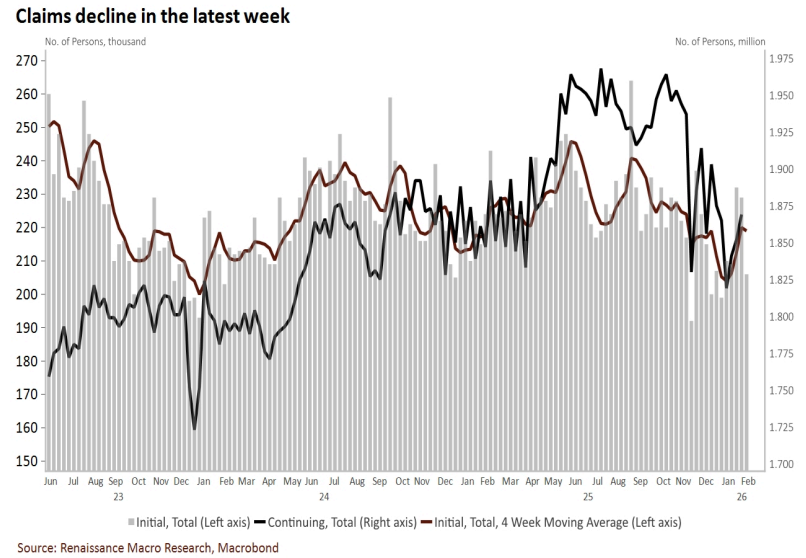

Initial jobless claims fell sharply to 206k, suggesting layoffs remain low and prior weather-related distortions have faded. However, continuing claims rose to 1.87 million, signaling that while separations are contained, displaced workers may be taking longer to find new jobs.

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

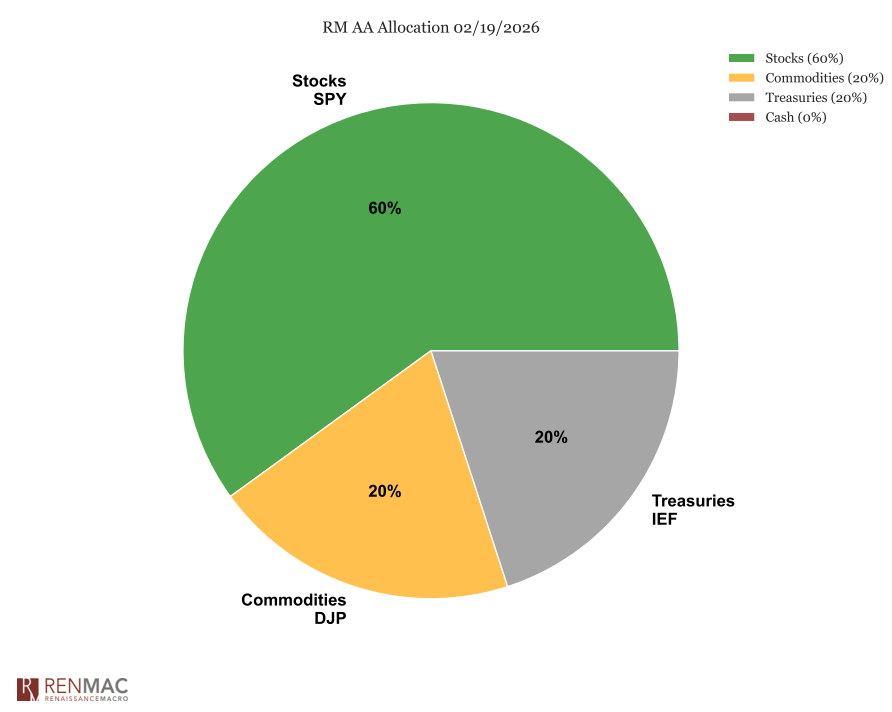

Asset Allocation Model

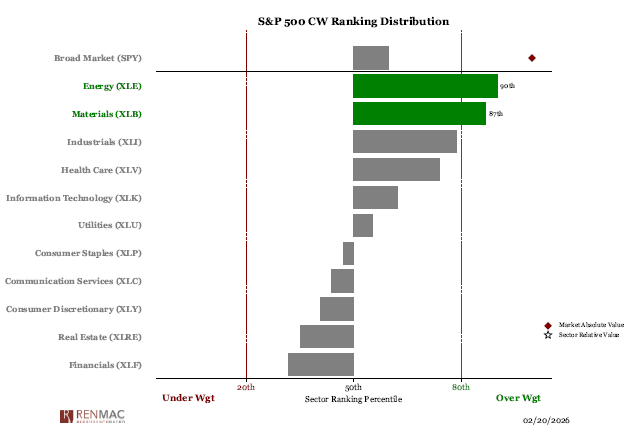

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week