Research Notes

Strategy

- The equal-weight S&P 500 continues to make new highs. The percentage of issues making 20-day highs are at 30%, still below our momentum thrust threshold.

- Simultaneously, the S&P 500 is flashing an overbought signal.

- Avoid chasing strength in overbought markets without momentum. Patience is warranted when adding exposure and we'd prefer to add on pullbacks.

- S&P 500 equal-weight cyclicals vs defensives are testing the 200-DMA following a lower high from last year. The trend is still bullish but looks vulnerable and we’ve already seen Discretionary vs Staples crack.

- Click here for a video Jeff did diving deeper into this.

- Emerging markets have been surging to start the year, but ETF inflows are showing signs of overheating. We'd caution chasing strength in EM and prefer to be a buyer of weakness.

- The latest Investors Intelligence data indicates an elevated bull-bear spread for the S&P 500.

- We put more weight on extreme downside than elevated readings, but given the overbought condition and lack of momentum in the market, caution is warranted around the elevated sentiment. This reinforces our view to be patient when looking to add exposure.

- EW S&P 500 Pharma triggered a positive relative trend change. Small-cap Pharma has significantly outperformed large-cap Pharma over the past year but it recently flagged as excess relative alpha generation in our SERM model suggesting to start rotating out of small and into large.

Economics

- If tariffs were going to create inflation, they'd create inflation, but in January headline CPI rose 0.2%, and over the last 12 months, CPI is up 2.4%, about where it was in May 2025. There is a lot of anxiety around tariffs but we're not seeing it.

- Core goods inflation has been flat for the last 4 months (yes, used car prices tumbled in January and auction prices show it is unlikely to repeat).

- Rents remain on an easing track, and by contrast, non-housing core services jumped 0.6% on the back of airfares and medical care services, but is up 2.7% over the last year, generally keeping up with a slowing trend.

- Interestingly, there was a sharp increase in airfares despite the slowing in lodging away from home.

- January's employment report was strong. Unemployment DOWN, Wage growth UP, Workweek UP, Jobs Growth BEAT. See here for a video from Neil on this. The robust labor data are a reminder that rate cuts are a forecast, not a present day necessity. If the labor market keeps up like this, it's hard to see the Fed penciling in insurance cuts anytime soon. The best you can expect in that case is a cut or two if inflation moderates. With that being said, Neil still believes the optimism around the labor market is premature primarily for two reasons...

- Consumers continue to report a high level of anxiety around employment. Job finding expectations are lower than they were during COVID.

- The breadth of payroll growth was weak. The good news is that more industries saw payroll gains, but the bad news is that private education & health services was the lion's share of the monthly gain. Neil is concerned about 4 areas moving forward...

- Technology: Layoff announcements have been perking up in recent months and share prices of software firms have been sliding.

- Residential construction: Rates are not coming down in time to save the spring selling season, meaning more affordability adjustments to move completed units which will squeeze margins, causing employment to drop.

- Food services: Payrolls here have surged by an average of just under 28k per month for the last 6 months which is surprising considering weak sales across restaurants.

- State and local governments: Will cut US GDP growth by an average of 0.2% per quarter this year. In FY2026, twice as many states forecast spending cuts or flat spending relative to last year.

- Technology: Layoff announcements have been perking up in recent months and share prices of software firms have been sliding.

- Existing home sales dropped 8.4% MoM to 3.91 million units SAAR in January, well below the consensus estimate of 4.15 million and the largest decline since February 2022.

- The severe winter storm likely weighed on contract closings, though January activity also reflects purchase decisions made in December when weekly mortgage purchase applications were trending lower.

- In January, NFIB Small Business Optimism Index fell to 99.3, roughly where it was in October. Despite talks of a capital spending boom, plans to make capital outlays over the next 3-6 months fell to 18, the lowest reading since April. Employment expectations also eased up to a 3-month low of 16.

- Despite the weaker intentions, small firms remain upbeat on the outlook with 15% reporting that now is a good time to expand. Now, despite rising stock prices and the passage of OB3, small business sentiment is actually lower than it was this past summer.

- Retail sales came in flat against a +0.4% forecast after a strong showing last month with 8 of the 13 categories posting declines. November's gain was also revised down to 0.2% from 0.4%.

- The combination of a weaker print and downward revisions implies retail spending carried less momentum into year-end than initially thought. That said, consumer spending remained resilient throughout Q4 on the whole, likely advancing ~3.0% annualized.

- The combination of a weaker print and downward revisions implies retail spending carried less momentum into year-end than initially thought. That said, consumer spending remained resilient throughout Q4 on the whole, likely advancing ~3.0% annualized.

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

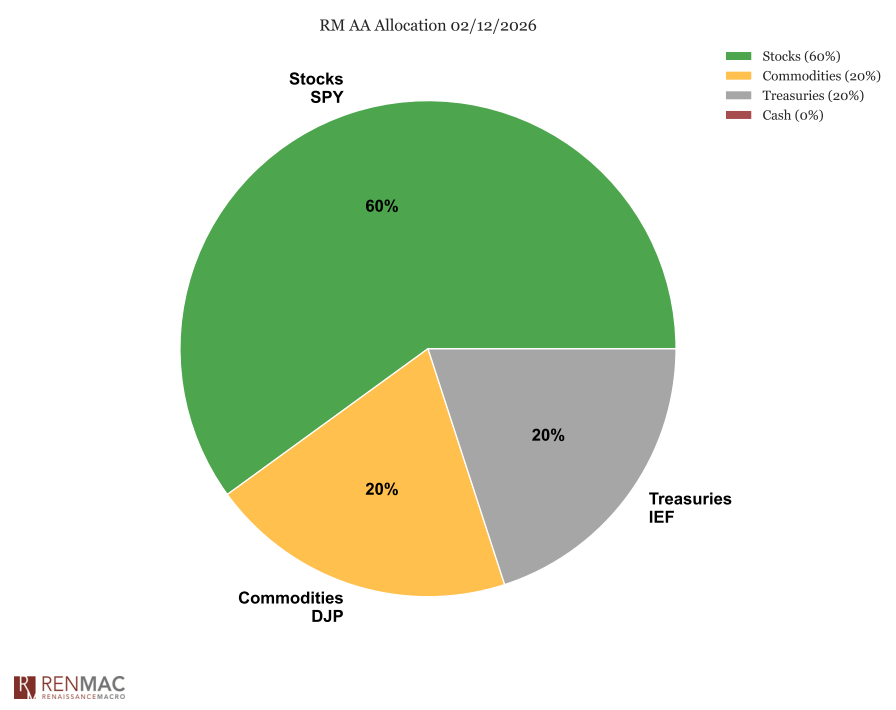

Asset Allocation Model

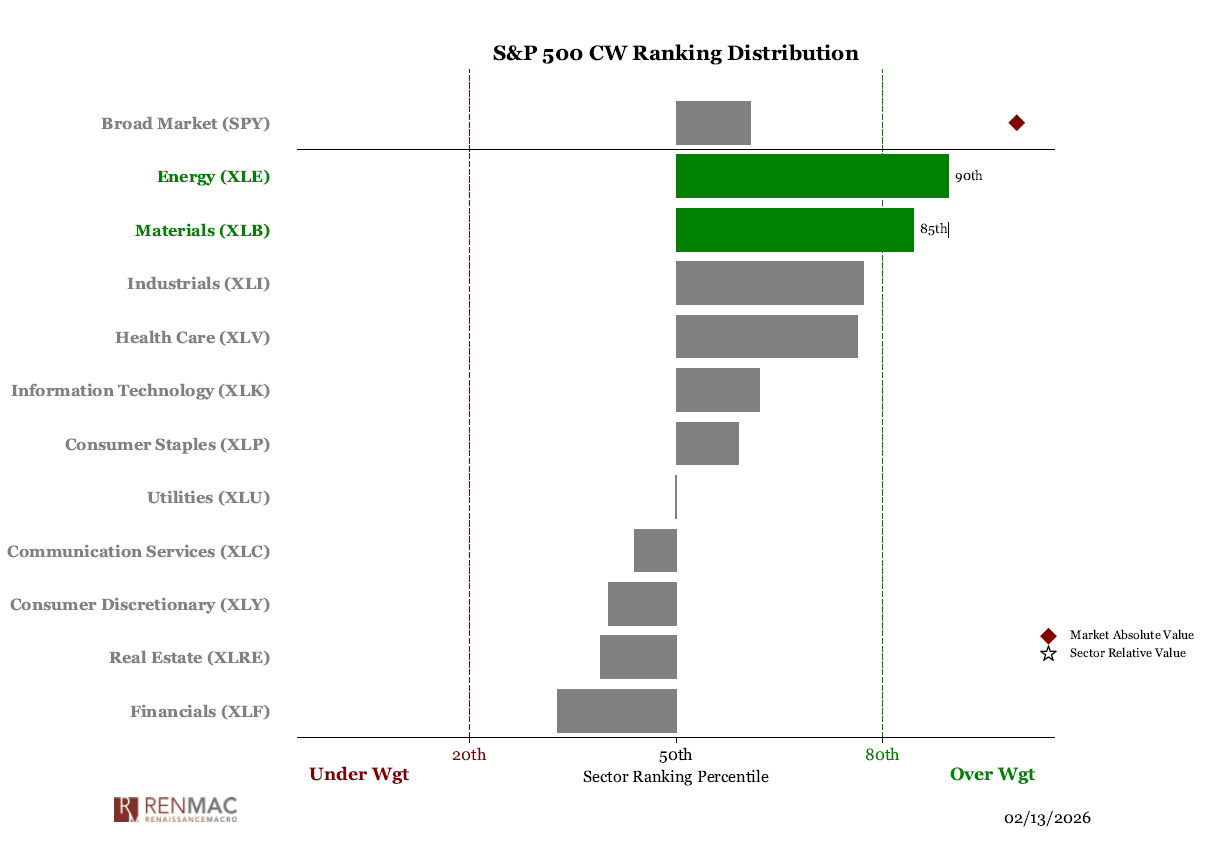

Sector Ranks

Sector Ranks  Chart of the week

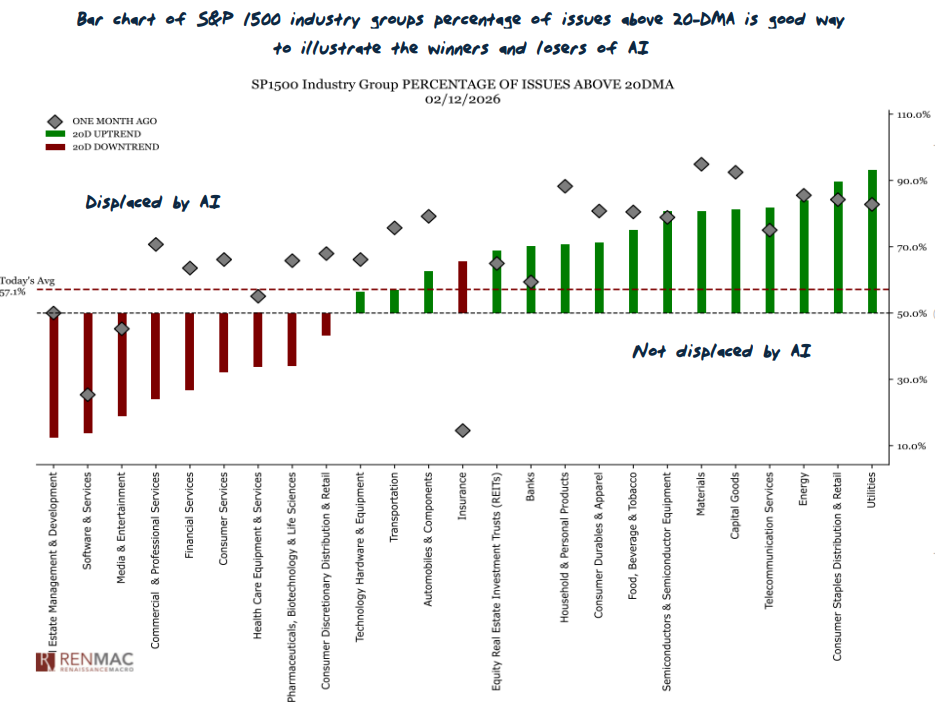

Chart of the week