Research Notes

Strategy

- Crypto showing relief took some sting out of the sentiment, but even their trend work has deteriorated enough to make us defensive.

- In downtrends, we expect overbought levels ($100k and $107k) and resistance zones to repel strength.

- The response to the recent oversold condition in the R2K has been impressive as the index has rallied 10% and is just shy of YTD highs.

- On an EW basis, the R2K is breaking out to new multi-year relative highs vs. the R1K, suggesting investors should be increasing their exposure to small-caps.

- The dollar is struggling at resistance as ADP data hep push December odds of a rate cut near probabilistic certainty.

- The dollar weakness is lagging metal's strength as copper shakes free of a 65-day high and the Bloomberg commodity index completes a large multi-year base formation.

- Materials as a sector are not bullish in our work, but metals and mining are.

- Homebuilders saw a clear improvement in relative performance and momentum after rate-cut odds for December jumped.

- Sentiment isn't stretched, leaving room for further gains and offering support to discretionary stocks.

- The broader housing supply chain isn't confirming the move - home furnishings and building products remain weak, with the latter breaking lower.

Economic

- Kevin Hassett is now the overwhelming favorite in the betting markets to succeed Jerome Powell as Chair next year. On paper, Hassett checks off all the boxes for the role, but Neil makes the argument he should not be Chair.

- Waller has the best track record of forecasting. Waller noted that inflation could fall without a surge in unemployment in 2022, and now has been quick to see the slowing in the labor market.

- Hassett can only use macroeconomics to try to sway an otherwise opposed Fed, while others like Bessent could argue market dynamics.

- Hassett is also not the best on TV, and his main qualification is his loyalty to President Trump.

- To be Chair, you must first be a Governor. Additionally, Powell may decide to stick around for two more years - in which case Hassett would operate as Chair in name only. Putting Waller in the seat likely ensures Trump gets to pick two Governors.

- According to ADP, nonfarm payrolls slid 32k in November, turning private payrolls negative over the last 3 months.

- Important to note that in the last 3 months, small firms have shed 178k off their payroll while large firms have added 143k.

- There is quite a bit of enthusiasm around Black Friday sales, but Neil says there is less than meets the eye.

- Strength is primarily online, but not a breakout pace.

- The data is not adjusted for inflation. According to SpendingPulse, retail sales ex-autos rose 4.1% against last year in nominal terms, but with prices for core goods ex used cars having jumped roughly 3%, the real spending growth is closer to 1%.

- The Fed will almost certainly have to revise its unemployment outlook higher, with trends pointing to 4.8% by year-end - well above the Fed's optimistic forecast.

- Core inflation is also easing, with core PCE on track for ~2.9% Q4/Q4, giving officials room to mark projections down by 0.1-0.2ppts.

- Yet, despite softer labor and inflation data, the FOMC is unlikely to shift rate projections much.

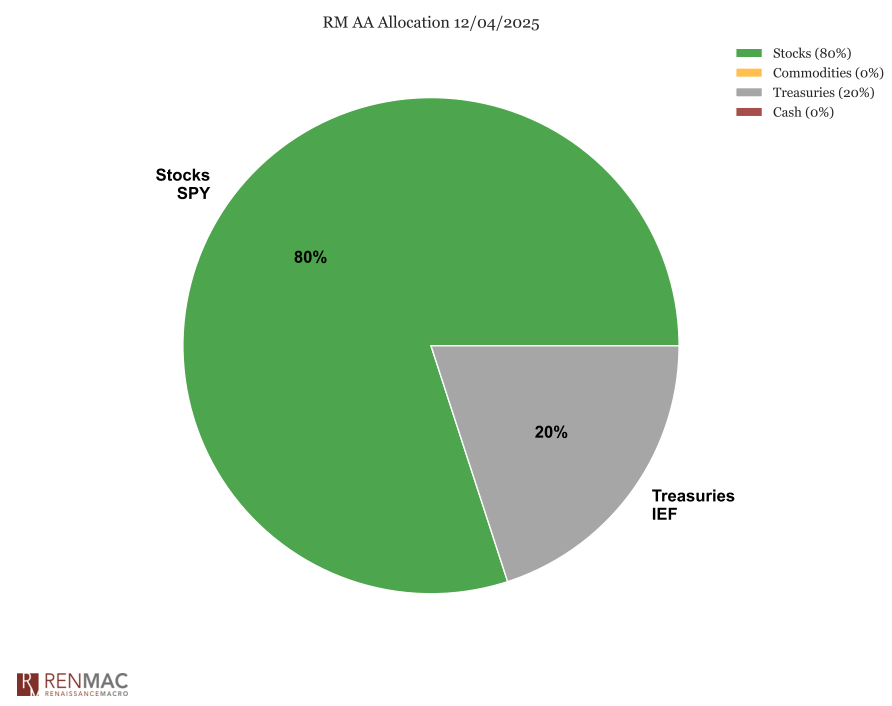

Asset Allocation Model

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

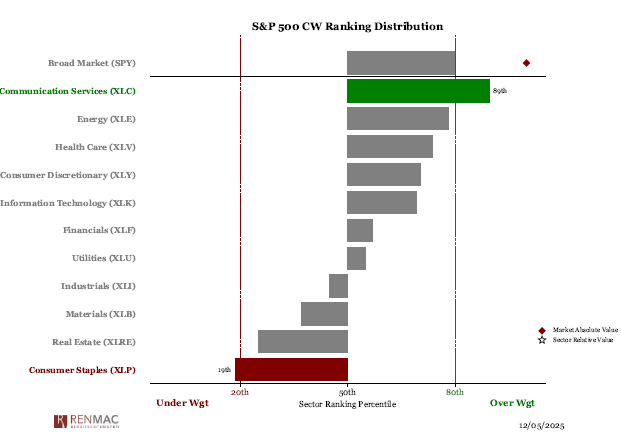

Sector Ranks

Sector Ranks  Chart of the week

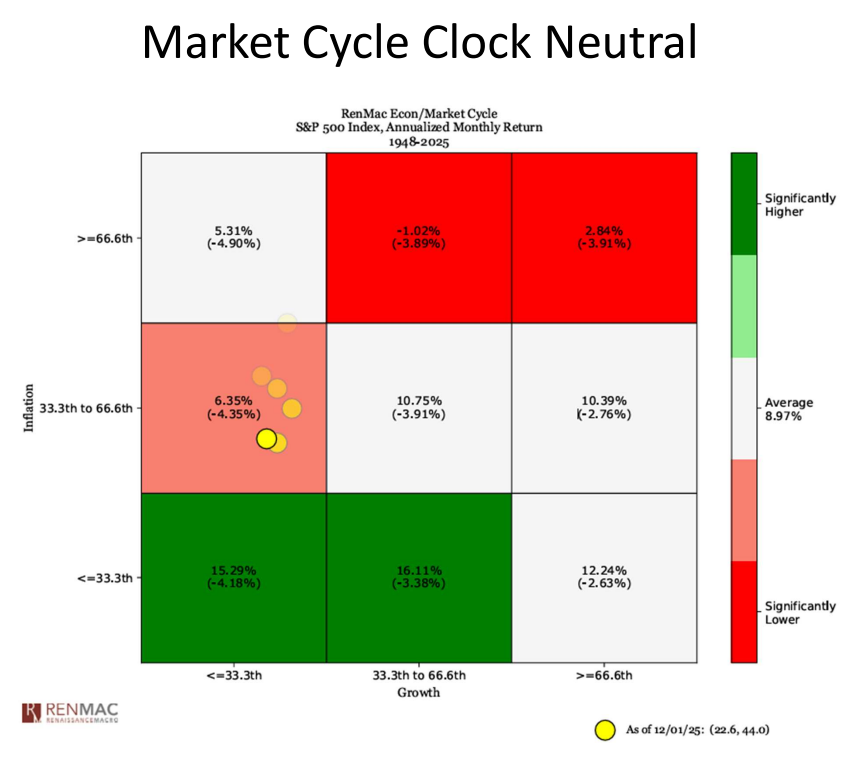

Chart of the week