Research Notes

Strategy

- Seasonally, January is in line with November and December, marking a strong part of the calendar.

- There are very few signs of momentum. Not outright bearish, but gives us a sense of how we want to think about the world, chasing breakouts versus looking for consolidations. The % of issues above their 20-DMA is hovering around 60%, leaving us in a trend market, not a momentum one.

- Inflation data are becoming increasingly supportive for equities as disinflation progresses.

- Core CPI currently sits near the 30th percentile historically, a zone typically associated with average forward market returns.

- More importantly, the trend continues to move lower, and when inflation falls into the bottom 20th percentile, six-month equity returns have been meaningfully stronger.

- While we're not yet in that strongest zone, the trajectory aligns with the market cycle clock framework and suggests disinflation could become a possible tailwind in 2026.

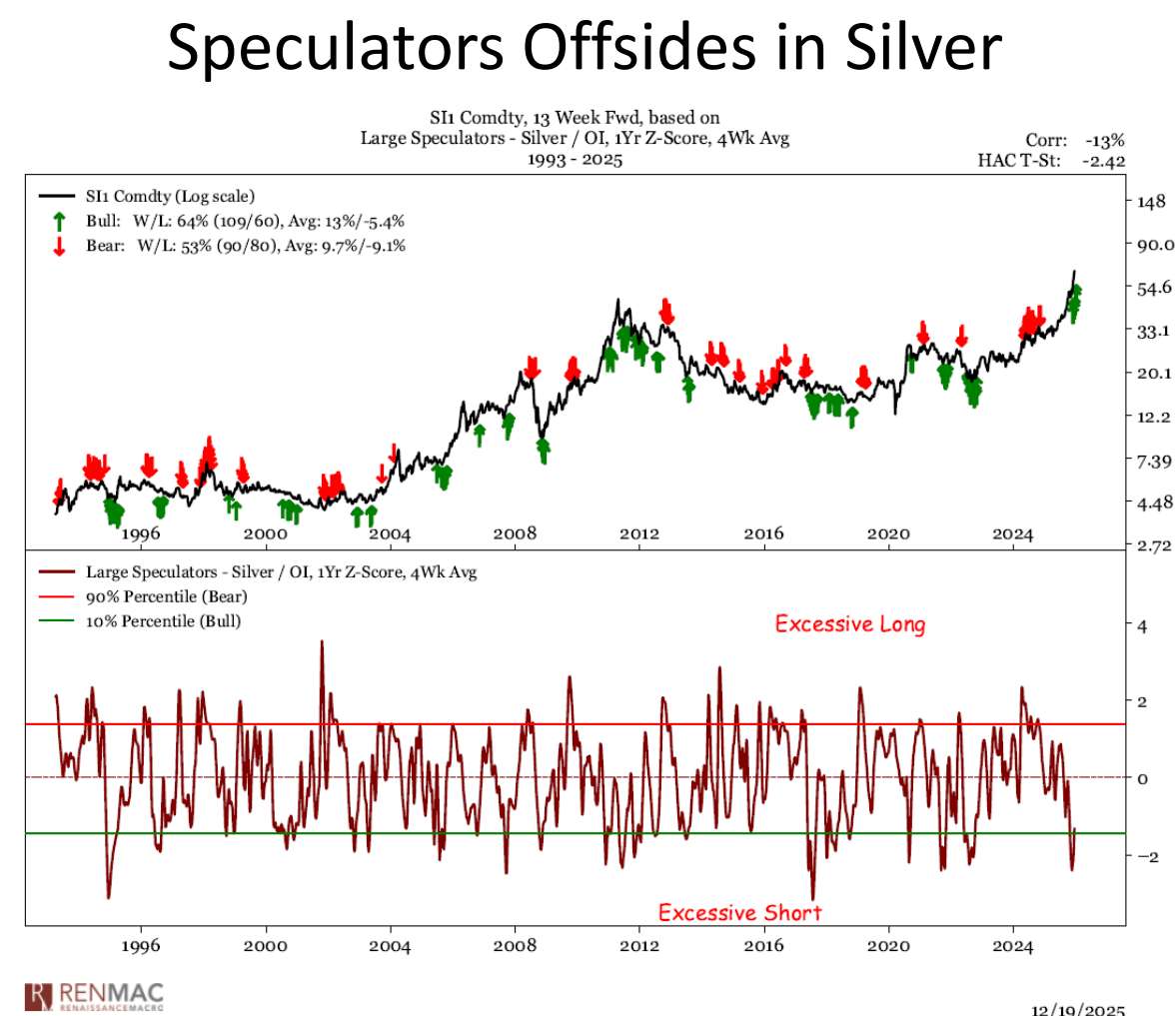

- Gold broke out again, and by our definition (double in 2 years) it has entered bubble territory again.

- With that being said, be on guard for V top formations. In bubbles, when you take money off the table, re-engaging when you go on to make new highs, or whatever threshold you set up is how you stay in the game and not make bad decisions at the very end when it sucks you in. Gold is still in a strong uptrend.

- We're seeing an anemic bounce in Bitcoin, but some good news is that outflows are excessive which should set us up for some snapback. We see this as a downtrend and like to make sure we're selling overbought conditions and not chasing oversold.

Economics

- Q3 GDP looked strong on the surface, but the underlying mix remains uneven and increasingly fragile.

- Growth was driven by consumption, with spending up sharply even as real income stalled and the savings rate fell, suggesting high-income households are carrying demand.

- Housing remains in recession and nonresidential investment is mixed, with equipment strength offset by weak structures, while higher prices are absorbing more capex and limiting real output gains.

- The gap between strong GDP growth and weak labor input persists, pointing to GDP growth likely slowing toward labor market trends rather than the reverse.

- If you take Q3 at face value, it implies rapid growth in labor productivity, north of 4% SAAR. Given the weak growth in compensation in Q3, this implies an outright decline in unit labor costs. Over the last year, "implied" ULC likely below 2%. Not bad for the inflation outlook

- US manufacturing production rebounded modestly in November, but underlying momentum remains weak. Over the past three months, output is down 1.2% SAAR, and without the 25% surge in aerospace manufacturing—largely driven by Boeing—factory production would have fallen by about 2.1%.

- Neil took some time this week to dig into residual seasonality in Core PCE Inflation, GDP, and NFP.

- Core PCE inflation data show a seasonal bias: Q1 readings tend to overstate inflation by 0.1%-0.3% (Q1 2025 overstated by 0.23%), while Q3 readings usually understate it, though the latest Q3 2025 adjustment is negligible, suggesting current inflation data are closer to underlying trends.

- GDP growth shows even larger seasonal distortions: Q3 growth has overstated true momentum by 0.7% on average since 2015, with Q3 2025's 4.3% print falling to 2.4% after adjustments, while Q4 is typically also overstated and Q1 understated but volatile.

- Monthly payroll data also shows seasonal distortions. August jobs are typically understated (by 21k on average, +70k August 2025), while February tends to be overstated, with October-November biased high and January-September biased low.

- Residual seasonality increases the risk the Fed misreads inflation, growth, and jobs at key turning points. Small monthly biases can translate into meaningful policy mistakes in a data-dependent framework.

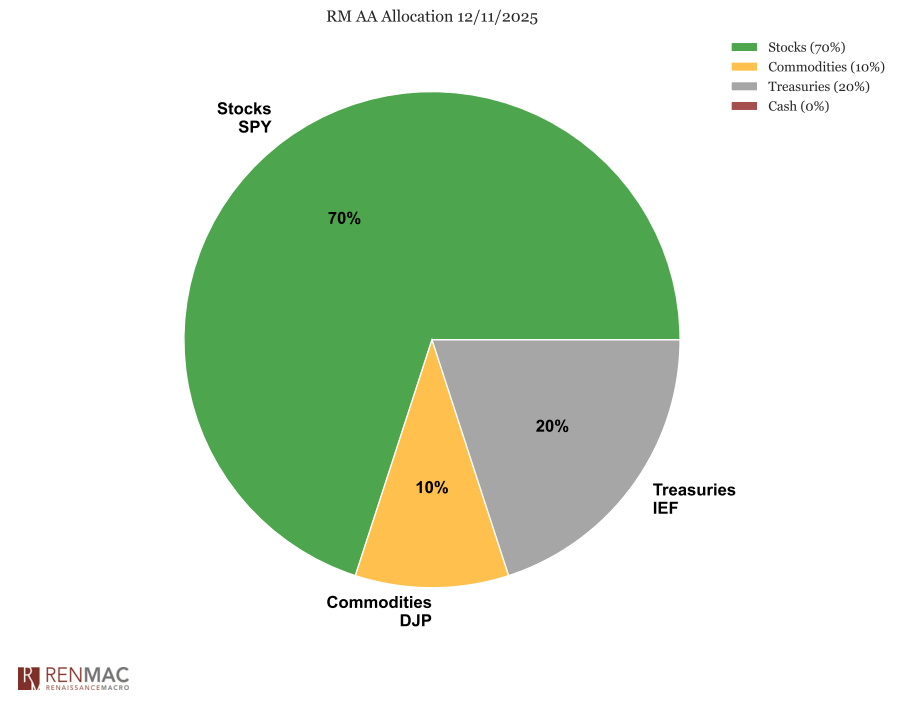

Asset Allocation Model

RenMac Off-Script Podcast

-

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

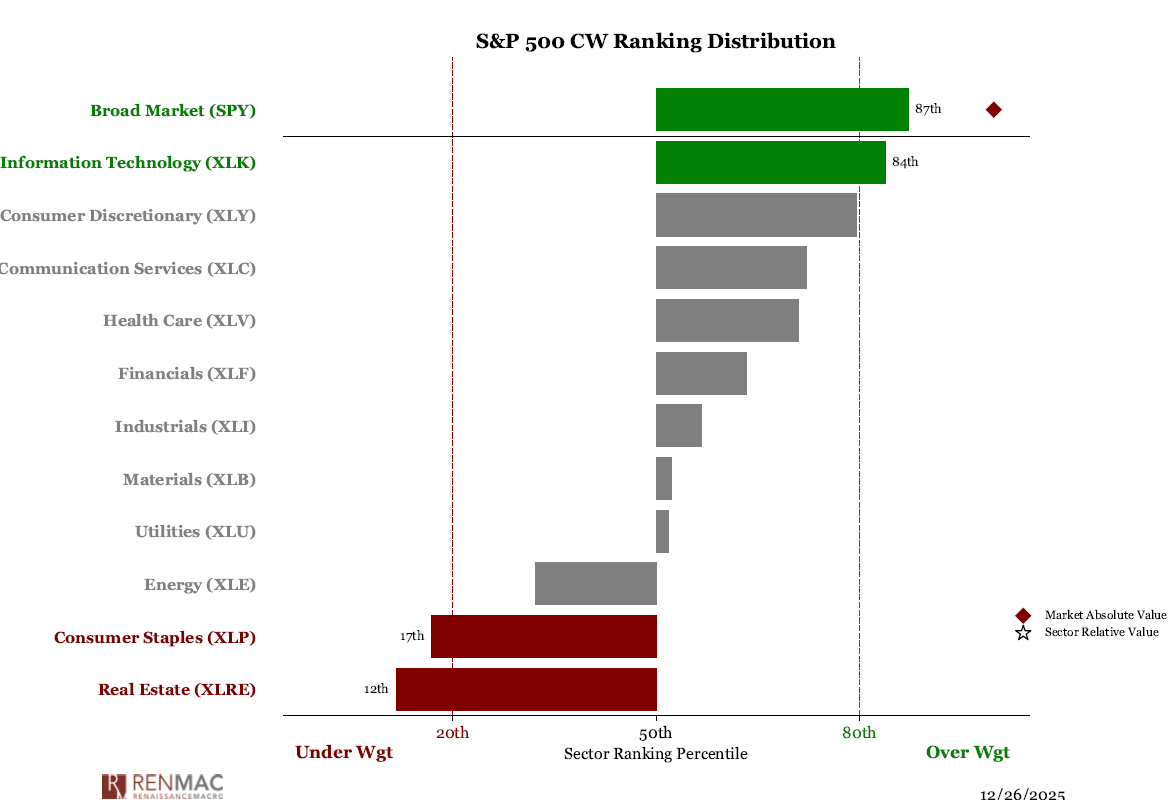

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week