Research Notes

Strategy

- Chinese technology may be extended, but momentum measures are so strong as to suggest staying with the strength versus fading it. We think upside remains substantial over long-run and are more focused on counting runs scored than balls and strikes.

- We remain bullish on China as a whole, and Jeff had a recent video explaining what we are seeing. Watch the video here.

- We remain bullish on China as a whole, and Jeff had a recent video explaining what we are seeing. Watch the video here.

- Homebuilders have anticipated a more friendly Fed, but ETF flows in XHB and equivalent have reached excess levels, suggesting sentiment and expectations may be ahead of the data.

- We would use the overbought condition to pair back exposure and buy weakness in the improving trends rather than chase strength.

- Short-rates are in a clear downtrend, intermediate-rates (10s) are a mixed bag, while the uptrend in long-rates persists.

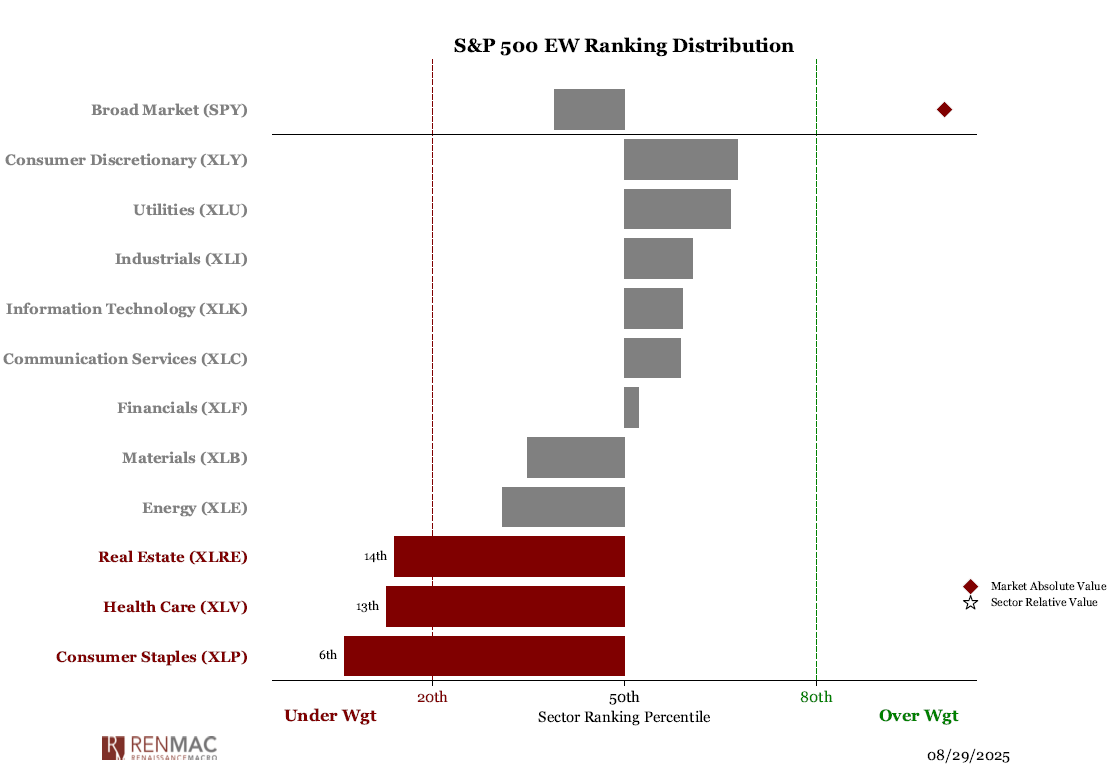

- The steepening curve has pushed staples to relative lows while improving EW discretionary trends enough to turn the group positive.

- The one area within discretionary we remain cautious on are restaurants.

- The steepening curve has pushed staples to relative lows while improving EW discretionary trends enough to turn the group positive.

- Beta is consolidating, not breaking down, and should still pay into year-end. Momentum has stalled since April but historically outperforms 70% of the time - setting up for a reassertion ahead.

- Relative trends have improved for the R2K

versus the R1K, but they are not dominant yet. In our opinion, one of the biggest bull cases to be made for R2K is the extreme positioning and consistent pounding these names have taken on a relative basis.

Economics

- Durable goods orders decline -2.8% in July, beating expectations of a -3.8% decline. Excluding transportation, orders jumped 1.1%. Core capital goods orders rose 1.1%.

- The strength appears partly driven by AI-related spending as real business spending on equipment grew 4.8% in Q2, with computers and peripheral equipment leading the gains.

- While capex intentions have improved

, they remain muted overall, but the underlying resilience in business investment is genuinely surprising to us. It's difficult to envision this momentum sustaining if broader growth expectations continue deteriorating.

- The strength appears partly driven by AI-related spending as real business spending on equipment grew 4.8% in Q2, with computers and peripheral equipment leading the gains.

- August saw a decline in consumer confidence - expected following significant downward revisions to payrolls. The Conference Board's headline consumer-confidence index fell, reflecting weakening fundamentals.

- The Labor Differential continues to soften, and we saw a significant jump in those saying "jobs hard to get".

- 2nd estimate of Q2 GDP was revised higher to 3.3% annualized versus an initial estimate of 3.0%, marking a significant acceleration from the 0.5% contraction in Q1. Consumer spending was revised up to 1.6% from 1.4%, and showed broad strength across both goods and services.

- While the headline GDP figure was robust, it was influenced by a massive swing in international trade.

- Net exports contributed a substantial 5.0% to GDP as imports plummeted, meanwhile inventory investment acted as a drag on growth.

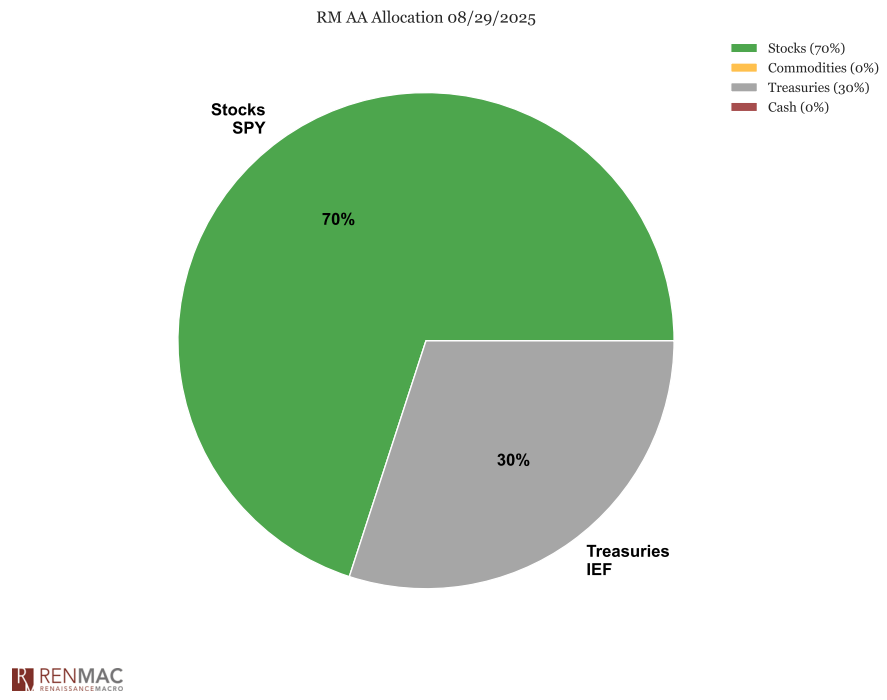

Asset Allocation Model

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week

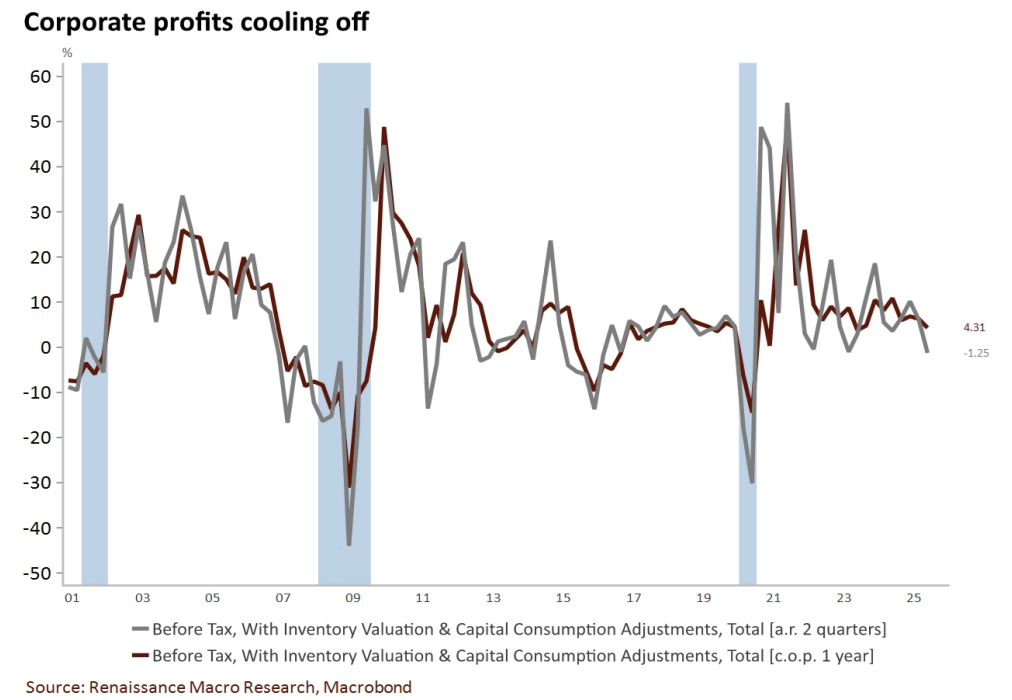

Despite the positive signs in consumer spending and investment, corporate profits have shown signs of cooling. Although they rose by 1.7% in Q2 after a decline in Q1, corporate profits have dropped by 1.3% (2-qtr %chg SAAR) so far this year, and 4.3% over last four quarters. This trend signals that while the economy is expanding, corporate earnings may be facing headwinds.

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week