Research Notes

Strategy

- Building on last week, SPX internals support a pause, so we turn our focus to the global ex-U.S. bull market.

- While none of our sentiment measures suggest too much optimism for the bull market to continue, we have seen the beta factor come down from the 100th percentile to the 93rd now with plenty more room to go.

- Cyclicals are weakening versus defensives, which is seasonally expected, but our Market Cycle Clock still points to cyclical outperformance once we're through this seasonal patch.

- After a golden cross in small-cap, we saw a minor breakout but no real change in relative performance. We're neutral here as a whole, but there are some strong areas of small-cap to focus on.

Economics

- Inflationary pressures intensified notably, as the Philly Fed prices paid index surged to its highest level since May 2022.

- Firms reported widespread price increases and none expecting decreases. Expectations are for their own prices to rise 4.1% over the next year, while employee compensation rises 3.5%.

- Despite this, six-month business outlooks are improving, and capital expenditures are picking back up, suggesting firms remain confident about longer-term growth.

- While July's housing data demonstrated some resilience, we also saw a dramatic slowdown in price appreciation to just 0.2% YoY, while Zillow shows further weakness.

- Taking the six-month annualized rate of change, food away from home CPI has climbed just 1%.

- Labor costs in the industry are already cooling down, and the workforce is overwhelmingly young people - teen unemployment has jumped 2.8% this year.

- Food away from home inflation has advanced 3.9% over the last 12 months, though Neil is skeptical this will be a meaningful source of inflationary pressure moving forward.

- Wage growth in advertised jobs is cooling, with the Indeed Wage Tracker now at just 2.4%, the weakest in five years. If immigration was responsible for the slowdown in the labor market, why is wage growth cooling too? Monetary policy hawks have some explaining to do.

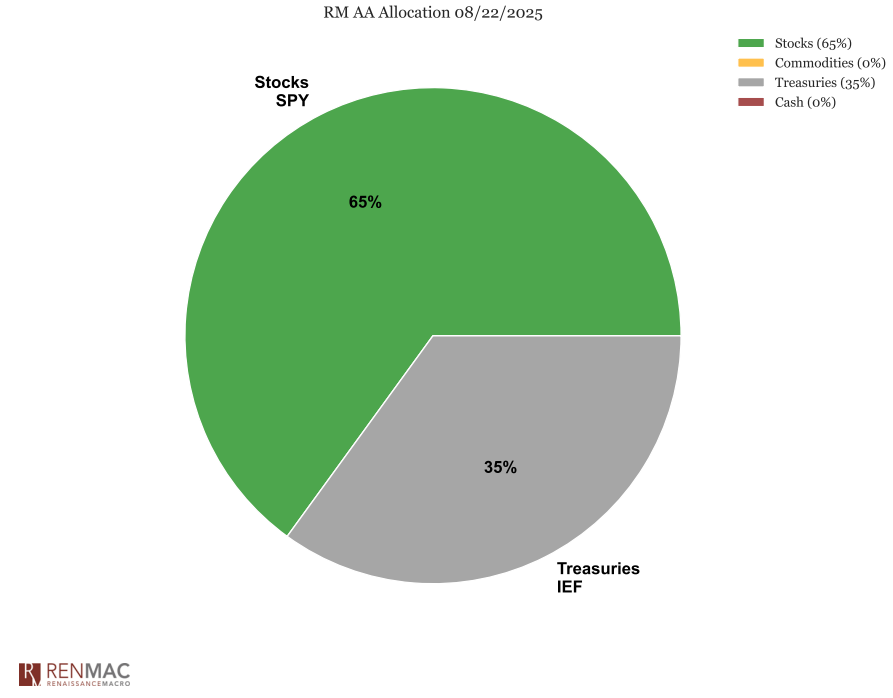

Asset Allocation Model

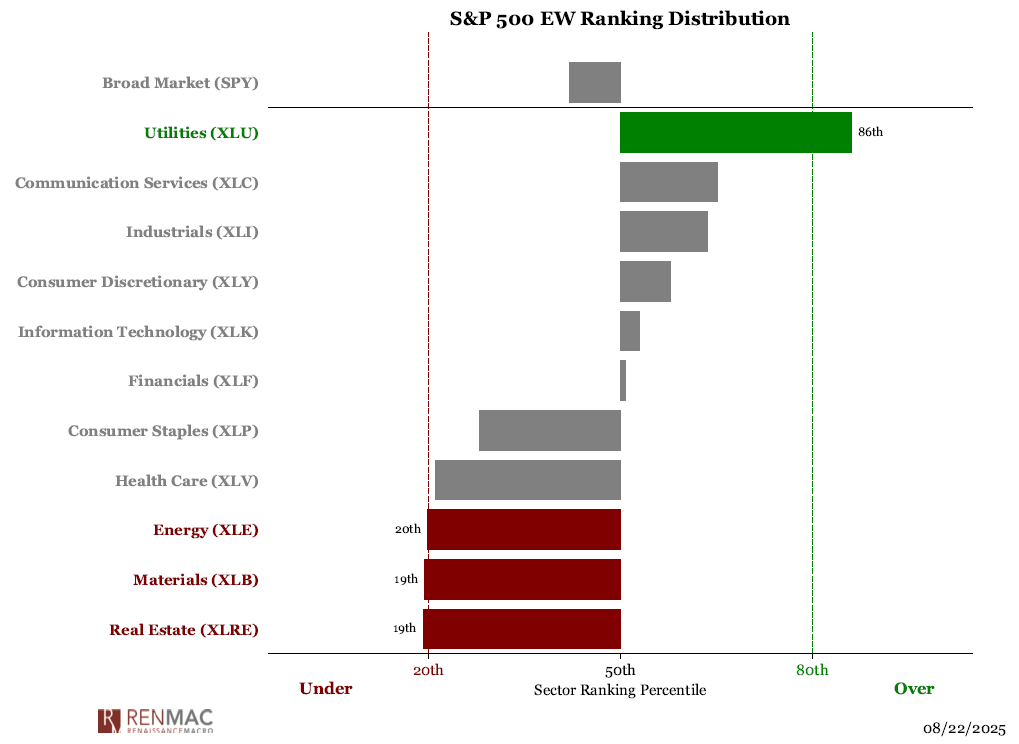

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week

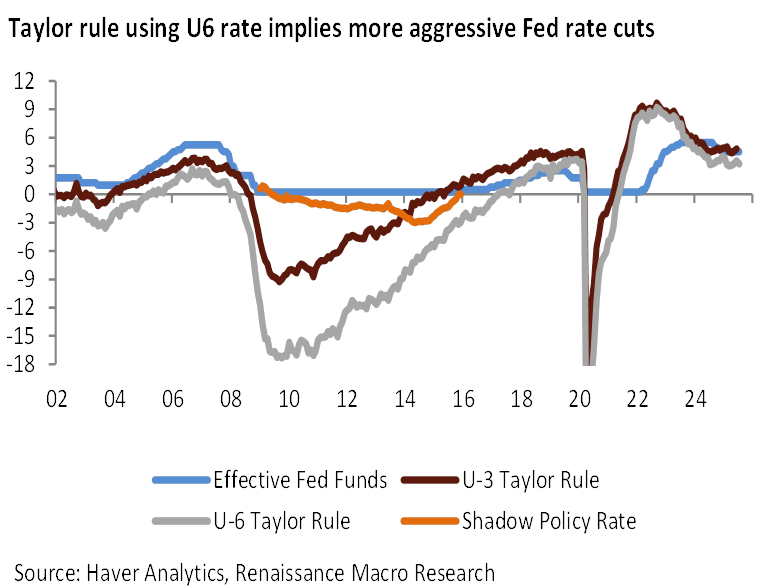

Leaning on the U3 unemployment rate and thus characterizing labor markets as "solid" is doing a lot of work for the monetary policy hawks. Neil estimates a Taylor Rule which implies lowering the funds rate by 1.3% if inflation falls by 1% and by almost 2% if underemployment rate (gap between U6 rate and that of 2019) rises by 1%. Neil admits maybe he was too pessimistic, but even assuming a neutral rate of 1.5%, we're 75bps too restrictive.

RenMac Off-Script Podcast

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

Asset Allocation Model

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week