Research Notes

Strategy

- We're seeing a minor momentum divergence emerge beneath the surface. While the S&P continues to climb, fewer stocks are holding above their 20-day moving averages.

- It's not a major red flag - more of a sign of seasonal fatigue and a natural cooldown after a blistering 3-4 month rally. We're still constructive - but easing off the throttle.

- It's not a major red flag - more of a sign of seasonal fatigue and a natural cooldown after a blistering 3-4 month rally. We're still constructive - but easing off the throttle.

- With sentiment stretched, trade-related positioning imbalanced, and the dollar pushing through its 50DMA, we see a tactical setup for a rebound in the weeks and months ahead. A stronger dollar could also act as a natural headwind for beta, cooling the risk-on trade that's dominated recent flows.

- We're already seeing some cracks: meme stocks and GS' most-shorted basket are rolling over.

- Copper just posted its worst single-day drop in at least 40 years. It's now oversold and still within trend - but historically, these kind of dislocations take time to stabilize.

- Volatility should fade, but we're not endorsing exposure here - seasonality is at its weakest for the next three months, and we expect a backing and filling taking place for the remainder of the summer.

- Our call to rotate toward momentum remains in play, but we're focusing on high momentum, low beta.

- Real Estate and Communications Services screen well by this framework.

- Health Care and Tech look vulnerable here.

- On the flip side, Financials and Industrials are crowded with high momentum names, while Real Estate and Energy have very few - worth watching for possible rotation setups.

Economics

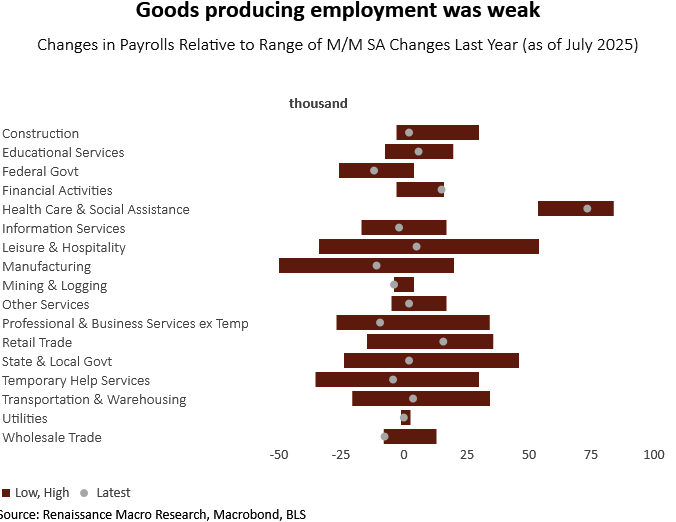

- Friday's NFP revisions were a red flag: A two-month net cut of -258k jobs is rare outside of recessions. Prime-age employment dropped to 80.4%, its lowest since March - a better signal than the headline unemployment rate.

- Markets are right to price in more near-term cuts. Discontinuities in the data may already be here.

- Markets are right to price in more near-term cuts. Discontinuities in the data may already be here.

- ApartmentList reports vacancies hit a record 7.1% in July, the highest since 2017. Rising vacancies are pressuring rents, which fell 0.8% YoY - a trend that typically leads CPI rental inflation.

- Real GDP rose 3.0% in Q2, rebounding from a 0.5% annualized decline in Q1. But the headline masks underlying softness.

- The sharp swing was largely driven by imploding imports, which artificially boosted net exports by 5%. Averaging the first half of the year, GDP grew just 1.2% SAAR - well below the Fed's longer-run potential, and consistent with Neil's view that the economy is slowing beneath the surface.

- When stripping out volatile components like trade and inventories, real final sales to domestic purchasers rose just 1.1% SAAR - the weakest print since Q3 2022.

- Neil emphasizes this is the number to watch: it's a cleaner read on domestic demand, which tends to be a more reliable signal of where the economy is headed.

- The sharp swing was largely driven by imploding imports, which artificially boosted net exports by 5%. Averaging the first half of the year, GDP grew just 1.2% SAAR - well below the Fed's longer-run potential, and consistent with Neil's view that the economy is slowing beneath the surface.

- Delinquencies among households earning at least $150,000 annually have surged nearly 20% over two years. This trend coincides with a cooling labor market, that has particularly impacted white-collar workers, creating pressure on an economy dependent on high-earner spending.

- New York Fed surveys indicate job-finding prospects for those earning $100,000 plus have deteriorated since 2023, now at 50/50 odds, the worst levels since before the pandemic.

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

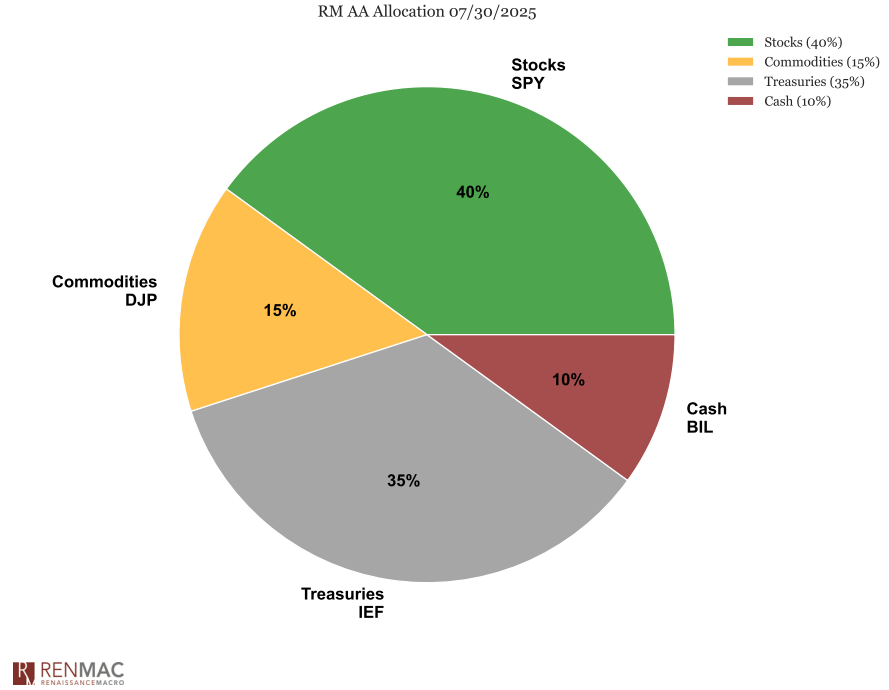

Asset Allocation Model

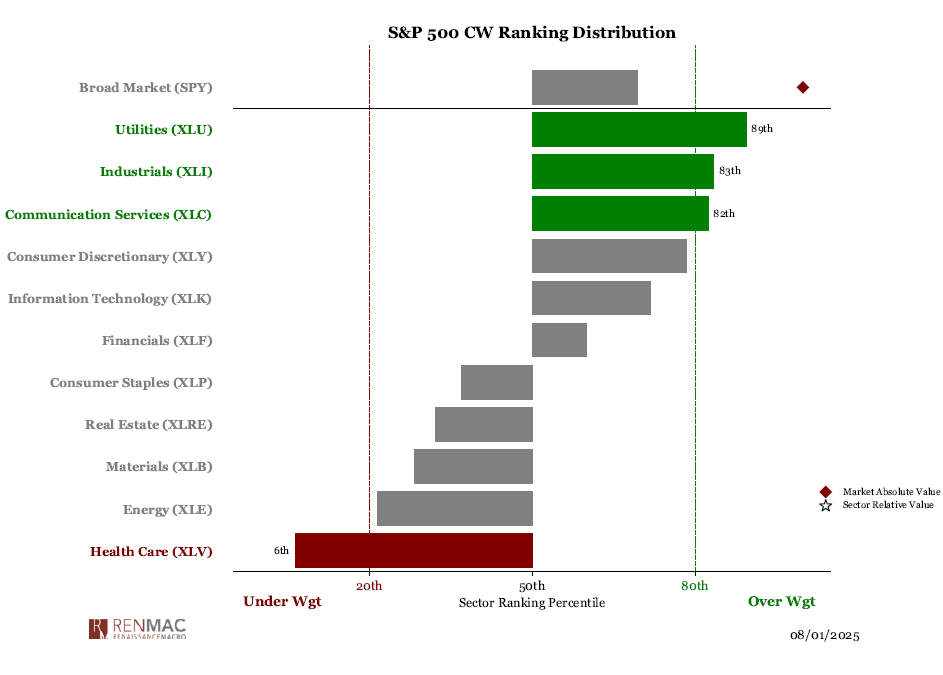

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week