Research Notes

Strategy

- The first positive volatility alert in SPX futures since April’s tariff rebound came Tuesday with 100% advancing issues in semis and Discretionary’ Durables and Apparel names.

- It was, however, only a decent breadth day and a little softer up-volume day. Strength is strength, but it was not confirmed directly by a contraction in oil prices, suggesting equity markets are searching for relief while oil markets are looking for confirmation.

- While we’re not convinced that the market is resuming it’s uptrend, we are convinced that those names breaking-out on a relative and absolute basis, particularly not tied directly to the war with Iran should be bought; they are a window into the soul of the narratives that develop in the next 6-9 months.

- Bull-Bear spread collapsed last week as the persistence of the war dragged down sentiment.

- Bears are not as high as we’d expect and while not providing a bullish signal officially, the survey have moved in the right direction given 13-week SPX returns.

- We’ve been tactically more cautious on energy believing the retail enthusiasm was likely to market a tactical peak.

- It’s not to say we don’t like the charts and even the valuation support for the group. We’ll be buying oversold conditions to get overweight as outflows start to develop, but that’s not happening here.

- We’ve been keeping track of the markets messaging regarding conflict through energy futures and option pricing, particularly the difference between Brent (geopolitically challenged) and WTI (less Hormuz impact).

- How to think about the 10yr yield:

- 10yr nominal at 4.50% is now in the 90th percentile of our Yield Impact Model, which historically is a bit below average for equity returns going forward. The worst case scenario in the 90th percentile however is flat returns for the next quarter, so not the end of the world, but works against returns.

- 5-year/5-year forward inflation expectations are at approximately 205bps and coming down. This tells you Fed credibility is intact.

- Spreads are rising, which points to a growth scare, not an inflationary regime.

Economics

- Strong headline masks softening labor market signals.

- In March, NFP exploded +178k following a decline of -133k in February. If February was depressed due to weather and strike activity, probably best to take average of last 2 months which would be just +22k.

- The distribution of employment growth was favorable causing the payroll diffusion index to rise to 56.8. That said, if the spring selling season is looking sluggish, and March was payback for weather, there is good reason to expect residential construction employment to bleed in Q2.

- Workweek slid 0.1hrs to 34.2hrs/wk. Meanwhile, average hourly earnings climbed just 0.2%, weakest since December. The surest signs of a tight labor market is accelerating wage growth, and we're just not seeing that now.

- The HH Survey saw the unemployment rate unexpectedly tick down 0.1% to 4.3%, making it unchanged since May 2025, and prime-age employment at 80.7% stands exactly where it was in April 2025.

- Retail sales rose 0.6% in February following a weak January, but the broader trend remains sluggish, with only modest growth over the past three months.

- While some categories like health and apparel saw gains, much of the strength appears driven by higher prices rather than real demand.

- After adjusting for inflation, spending in key areas like clothing, groceries, and household goods likely declined, pointing to soft underlying consumer momentum despite the headline rebound.

- Mortgage purchase applications declined again as rising rates (now ~6.57%) continue to weigh on demand, with activity largely flat over the past year.

- With minimal home price growth and rates rising into the key spring season, housing momentum is likely to remain subdued.

- ISM Manufacturing improved modestly, but rising prices and delivery delays point to lingering supply pressures.

- With new orders soft and employment weak, the strength looks more like temporary inventory restocking than a sustained recovery.

- Consumer confidence rose modestly in March despite falling equities and higher gas prices, but underlying labor market signals deteriorated, with more respondents sayings jobs are hard to get.

- With employment pressures building and energy costs likely to rise further, the resilience in sentiment may prove short-lived.

RenMac Off-Script Podcast

.png?width=717&height=403&name=04-03-2026RenMac%20-%202%20(1).png)

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

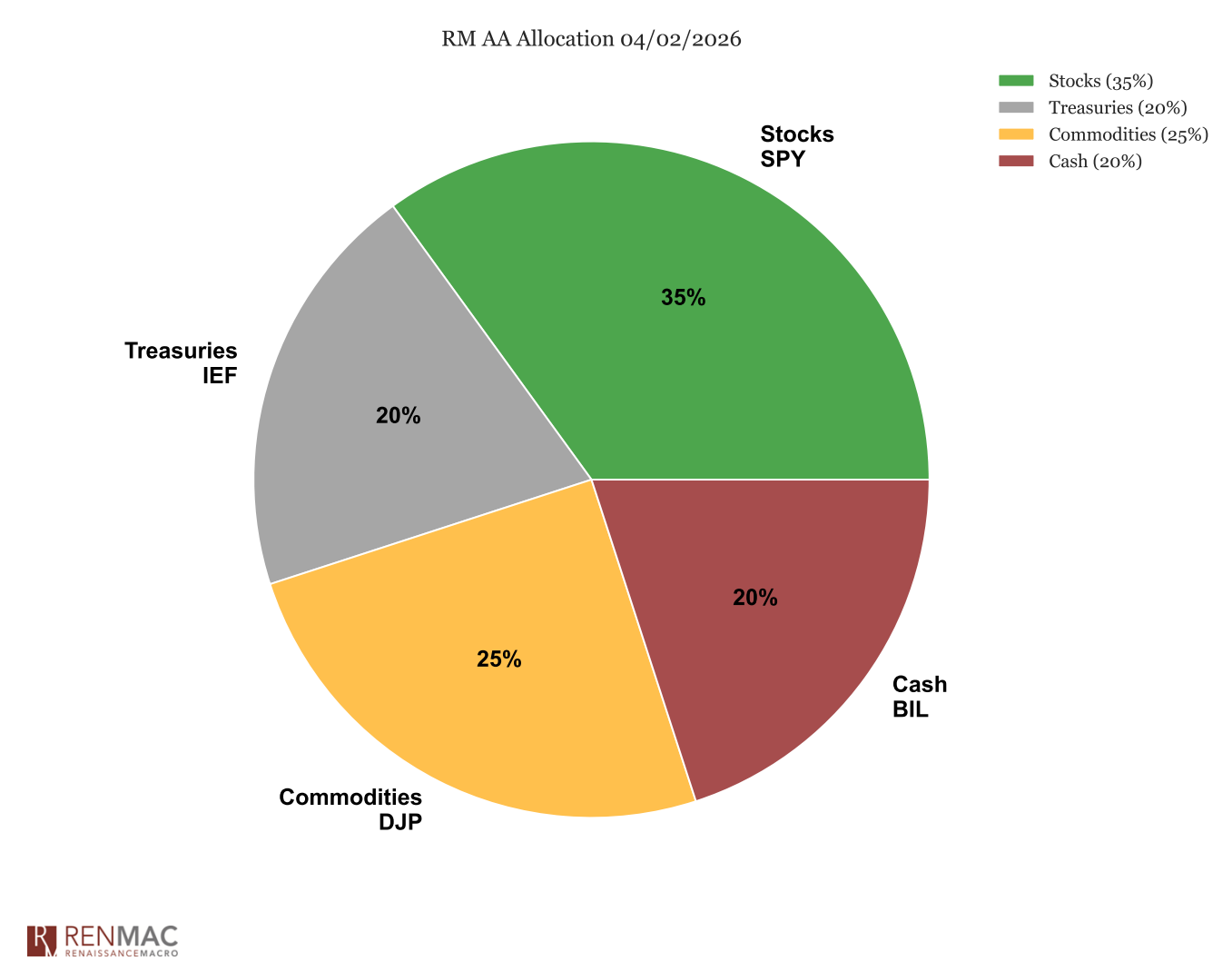

Asset Allocation Model

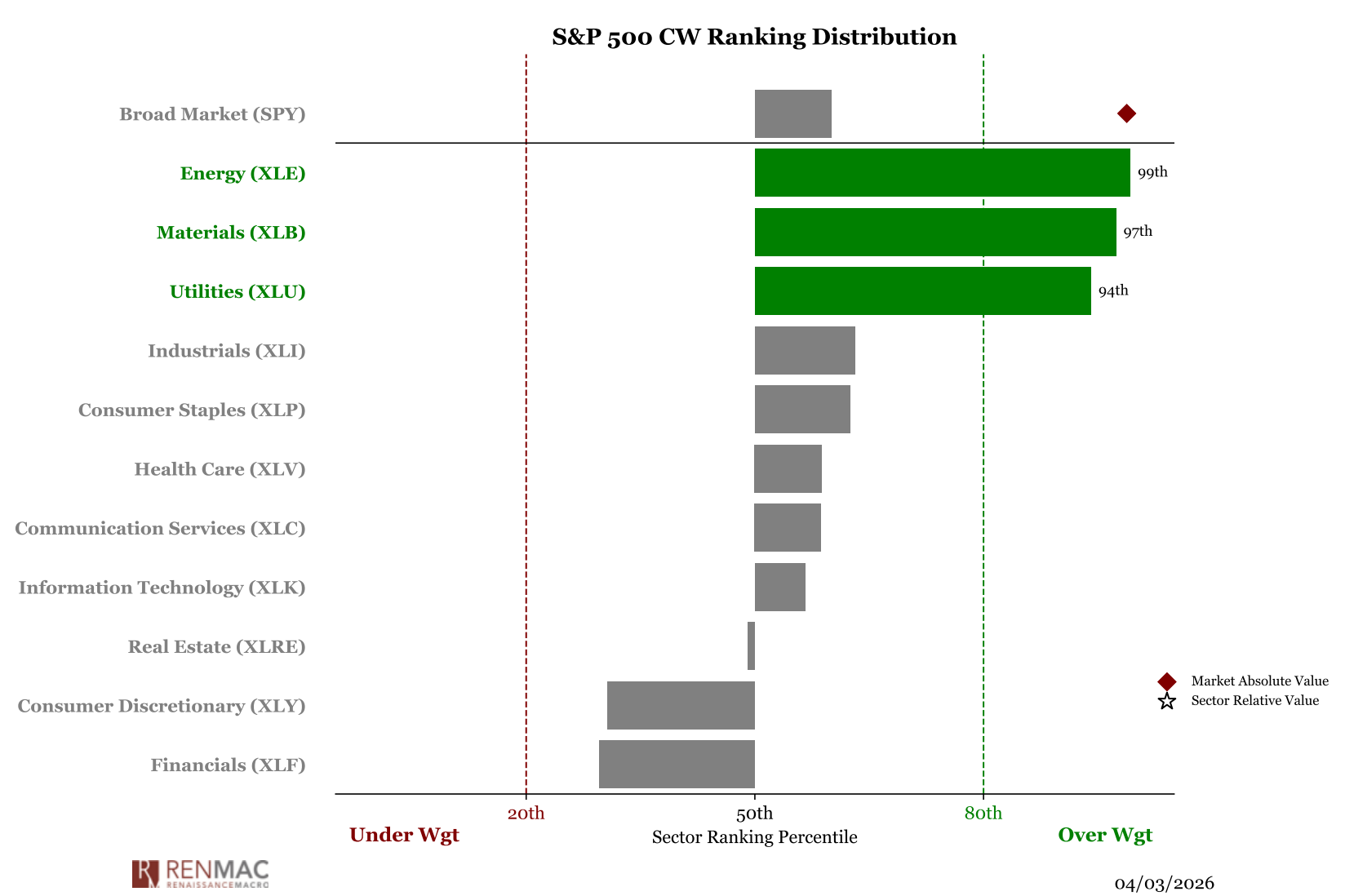

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week