Research Notes

Strategy

- We generally define a momentum thrust as a surge of more than 50% of stocks in an index making 20-day highs. That condition has been met for the Russell 2000 and Russell 3000, but not yet for the S&P 500, which we tend to prioritize given its stronger historical reliability as a signal. That said, alternative measures can also capture momentum thrusts. Click here for a deGraaf video on the subject.

- One such approach looks at whether the percentage of advancing volume or stocks over a 10-day period in the Russell 3000 reaches its upper Bollinger Band, effectively signaling an extreme relative to its standard deviation.

- When both measures align, as they just have, the signal tends to carry more weight. Historically, tactical returns following these thrusts are often muted as they tend to coincide with overbought conditions, but performance over 3-, 6-, and 12-month horizons has typically been strong.

- We think there is sufficient evidence to suggest a momentum thrust and an extension to the bull-market is underway. However, this episode differs from the thrust off last year’s Liberation Day lows. At that time, the market had undergone a deeper pullback, where sentiment and momentum were more washed out.

- In contrast, current positioning in the S&P 500 is already near bullish extremes, and the relative performance of high vs low momentum stocks, particularly within Tech, is as strong as it has ever been. While the outlook still favors momentum, we would characterize this as a later-stage phase, one that carries an increased risk of a speculative blow-off top, potentially reminiscent of 1999.

- The S&P 500 High Beta Index continues to climb to new highs, now up more than 20% from its March 30 lows and leading the broader market. This type of leadership is typical following market bottoms, as high beta stocks tend to outperform in early-stage recoveries.

- Beneath the surface, however, the magnitude of some sector moves stands out. Within the Russell 1000, high vs. low beta Tech has surged more than 200% on a 252-day basis, well beyond its performance during the dot-com bubble. Industrials are also showing significant strength, with high vs. low beta up nearly 100% over the same period.

- We’d expect some near-term tactical consolidation, consistent with the typically softer one-month returns that follow momentum thrusts. But the strength of 3-, 6-, and 12- month returns suggests that weakness or consolidation in market leadership should be bought.

- Gold still looks vulnerable to us here as it struggles with the declining 50-DMA. We are not big gold bears but think there is further downside, possibly to the 200-DMA.

- The gold miners recently got overbought and it looks like a good time to lighten up in the space.

- Seasonality is historically bearish for gold over the next three months.

- Also, gold recently flagged as excessive negative relative returns vs silver in SERM, suggesting mean reversion, implying silver is even more vulnerable than gold here.

Economics

- The US economy is currently being supported by strong business investment, particularly AI-related capex, but that support is set to slow. After surging the past two years, Hyperscaler spending is expected to decelerate sharply, which could start to weigh on equipment investment and overall growth into 2027.

- Fiscal policy is also becoming less supportive for the US economy. What has been a tailwind turns into a modest drag this year and a more meaningful one next year, gradually removing a key pillar of growth.

- There is a policy angle as well. If the Fed stays on hold while fiscal policy tightens and wage growth cools, that effectively acts as passive tightening on the US economy.

- Not an immediate issue, but the setup for the US economy into next year looks less favorable as these key supports begin to fade.

- The labor market looks stable at the margin. Job finding rates are already weak, near levels typically seen around recessions, so there is limited room for them to deteriorate further. That means any meaningful rise in unemployment from here would likely need to come from layoffs, and there is little evidence of that so far with claims still low.

- The issue more about lack of upside. Labor demand is not improving and wage growth is showing signs of slowing.

- Forward-looking measures like Indeed wage postings and broader labor tightness indicators point to continued cooling, suggesting income growth is unlikely to reaccelerate anytime soon.

- Headline retail sales rose 1.7%, but most of the strength came from higher gas prices. Strip that out and the picture is still decent, with core sales up 0.7% and real sales closer to 0.8%.

- Spending is holding up but getting more selective. Online and goods categories are firm, while restaurants and housing-related areas are soft.

- With weak income growth, consumers are likely leaning on savings and tax refunds, making the overall mix look more fragile than the headline suggests.

- April PMIs held up on the surface across the US, UK, and Japan, but the resilience looks misleading. Services are softening as consumers pull back, while manufacturing strength is being driven by precautionary inventory building rather than real demand.

- That stockpiling is showing up in prices. Input and output costs are surging across regions, with services inflation particularly firm, pointing to renewed inflation pressure even as underlying activity looks more fragile.

- Pending home sales extended their rebound in March, with the NAR's contract signings index rising 1.5% to a four-month high of 73.7. This marked the second straight monthly increase, as improving inventory helped offset the drag from higher borrowing costs.

- On a year-over-year basis, however, contract signings slipped 1.1%, a modest loss of momentum. Regional patterns were uneven: the Northeast (+4.4%) and the South (+3.9%) led the monthly gains, while the Midwest and West declined.

- The annual picture tells a different story, with the South the lone region in positive territory (+2.3%) and the Northeast logging the steepest drop (-6.5%), followed by the Midwest (-3.1%) and West (-1.7%).

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

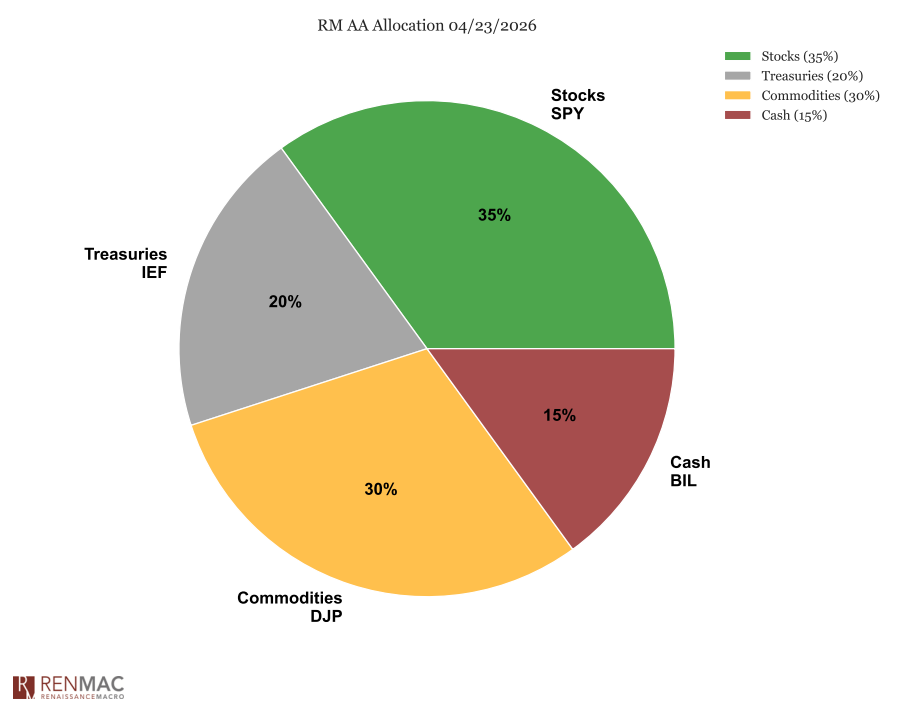

Asset Allocation Model

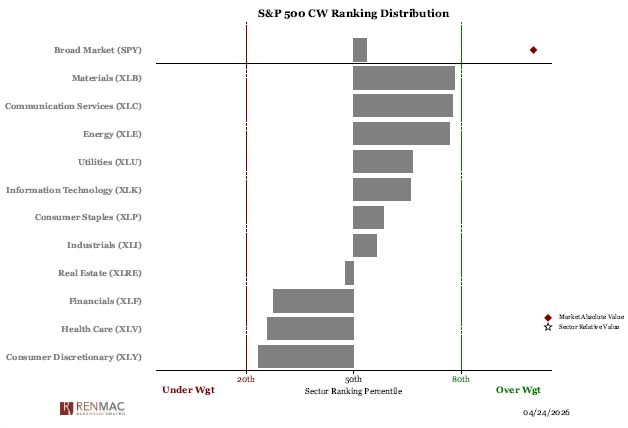

Sector Ranks

Sector Ranks  Chart of the week

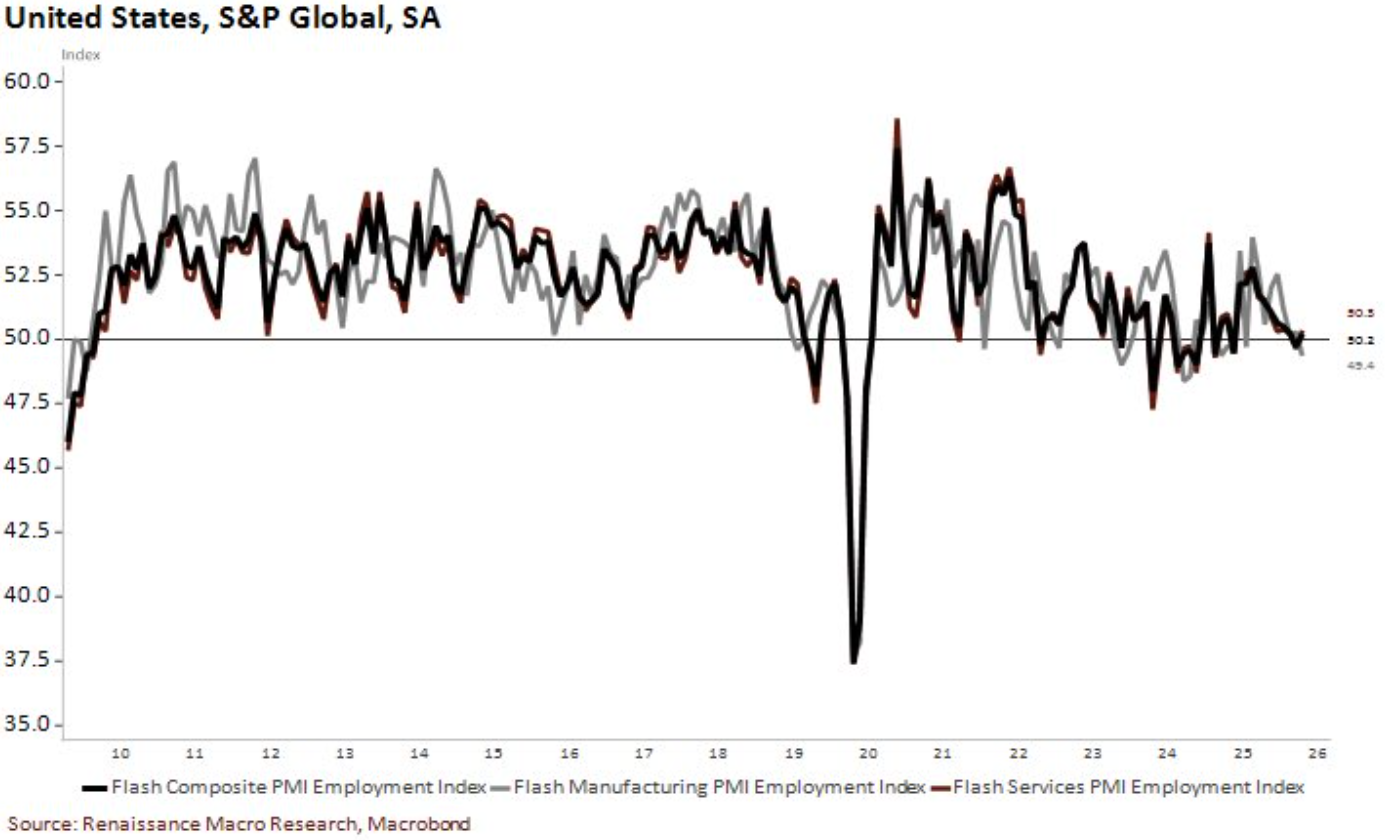

Chart of the week