Research Notes

Strategy

- Recall that pre-war conditions were not ideal, clouds existed on the horizon. Private credit was deteriorating, inflation data was not “heeling” its master, and market momentum had been soft for several months.

- Escape velocity for markets is not achieved by a day’s returns, but the characteristics of what is driving those returns. Up is up, but conviction is expressed not only through majority participation, but super-majority participation.

- 84% of the S&P and 82% of the Russell 3000 advanced Wednesday, after the ceasefire announcement; those are mediocre statistics, not game-changers. Most encouragingly, financials had 94% advancers in R3 while tech was a less inspiring 67%.

- For now, we’re buyers of relative strength highs and positive volatility alert names that are optimal entries. Those should provide leadership and a cushion of safety should things unwind and the markets decide on a retest sequence.

- Double-B vs Triple-B spreads contracted as 10-yr yields remained flat. For a sustained rise and evidence that investors are again pushing out the risk curve, willing to squint into the future to discounted cash-flows, real yields should contract.

- They closed Wednesday at 1.96% on 10s, down from 2.13% on 3/27, but they have not changed trend.

- 20-day highs advanced to 32% under 62% advancing names Thursday. Breadth was led by utilities with 88% advancers on the Russell 1000 and just 37.2% for technology.

- It was another bloodbath for software related names, with many making new lows as the market tries to find its footing.

- Focus on the winners- the breakouts- the relative highs- Momentum is still stretched, but this is a messy tape and momentum is most vulnerable at peaks with raging bullish sentiment. It’s uncomfortable, that’s probably a good indication that they’re the right place to be, for now.

Economics

- Growth expectations have to be revised down, and they are traditionally sluggish in Q1 following a weak retail sales report. Consumer spending now tracks just 1.5% annualized for Q1.

- PMI data yields similar results. When we translate those results into its effect on GDP, we get 1.6%, it's lowest level since May 2025.

- We have seen an improvement in manufacturing activity and have seen some capacity come out of the system, however we'll be sure to not get carried away here as manufacturing alone is barely consistent with 2% real GDP.

- March payrolls look strong on the surface but the signal is noisy: readings have swung positive and negative every other month since June 2025, and monthly volatility has clearly risen.

- Weather has been a meaningful tailwind, with a SF Fed model estimating favorable conditions added roughly 150,000 jobs on average over the last two months, masking a deteriorating underlying trend.

- Forward-looking hiring indicators are not encouraging, with NFIB employment plans at multi-year lows, PMI data softening, and consumers expecting fewer jobs over the next six months.

- Weather has been a meaningful tailwind, with a SF Fed model estimating favorable conditions added roughly 150,000 jobs on average over the last two months, masking a deteriorating underlying trend.

- Wage growth for nonsupervisory workers in private education and health services has cooled sharply to 2.0%, and this signal shouldn't be dismissed given the sector represents over 20% of all private payrolls.

- Supporting data backs the slowdown: Indeed's job posting data shows wage growth for nurses and medical techs running below 2%, and the quits rate in the sector has fallen to decade-lows.

- Broader wage deceleration is evident across sectors too, with professional and business services wage growth at 3.2%, but losing momentum, confirmed by cooling quits and posted job data.

- Business equipment investment looks strong on the surface, with core capital goods orders up 0.6% in February and shipments posting a second solid gain in 3 months.

- But in real terms the picture is less impressive, as producer prices for capital equipment are up 5.4% YoY, roughly offsetting the nominal shipments growth.

- The composition is also narrow: computers and electronic products account for most of the core shipments growth so far this year, suggesting the strength is not broad-based.

Research Notes

Economics

- US labor market continues its downtrend. Weekly job postings continue to trend down, layoffs picking up, quits are cooling.

- March data showed broad economic weakness, with declines in services, confidence, housing, and commercial real estate.

- Rising inflation, weakening job outlooks, and cautious business spending point to growing economic strain.

- Home prices are cooling, which may curb spending as household wealth dips and the savings rate edges higher.

- The rebound in capital goods shipments looks fragile, with growth mostly tied to tech and broader investment plans weakening.

- New tariffs could cut 0.5% from GDP, strain trade ties, and raise car prices before production shifts take effect.

- Auto repossessions are at their highest since 2009, and tariffs may push buyers to the used market, keeping prices elevated.

- Despite trade tensions, signs of de-escalation and strong profits offer some cushion, with markets already pricing in much of the downside.

- Q4 growth was lifted by consumer and government spending, but with investment falling and key supports fading, a broader slowdown seems likely.

Strategy

- Market technicals show potential for a rebound. We think Mag7 approaches 50dma and potentially crosses through, getting to overbought, high beta stocks slowly recovering, and excessive outflows in IWM and SPY could fuel a tactical bounce.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Remember, this was a beta-driven correction, not a momentum-driven one.

- Bullish signals may re-emerge if a high percentage of stocks move about their 20dma and hit 20-day highs, suggesting a reassertion of the bull trend.

- Despite heightened policy uncertainty and a dark cross in tech, strong credit markets and sentiment tied to returns suggest the current pessimism may be overdone.

- Semi's continue to weaken, with even "good" ones coming under pressure.

- Staples pulled back at resistance levels, maintaining relative downtrend. Sharp unwind in beta and extreme underperformance suggests continued downward pressure.

- Transports reiterate bearish trend but flagging oversold and in "seller's frenzy". Expect short-term tactical bounce but fade the move.

Policy

- Debt limit deadline ("X-Date") likely between July and October, with resolution hinging on reconciliation or bipartisan deal amid uncertain cash flows.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Delays risk market volatility and a Moody's downgrade, raising U.S. borrowing costs.

- Trump will announce reciprocal tariffs on April 2, targeting about 15 key partners; recent moves on oil, autos, and threats to the EU and Canada may be strategic leverage.

- Section 232 is being used more broadly to justify tariffs on national security grounds, covering autos, copper, timber, and pharma, with an emphasis on U.S. production.

- Tariff timing and scope remain unclear, with Trump using them as a flexible tool, adding to market uncertainty.

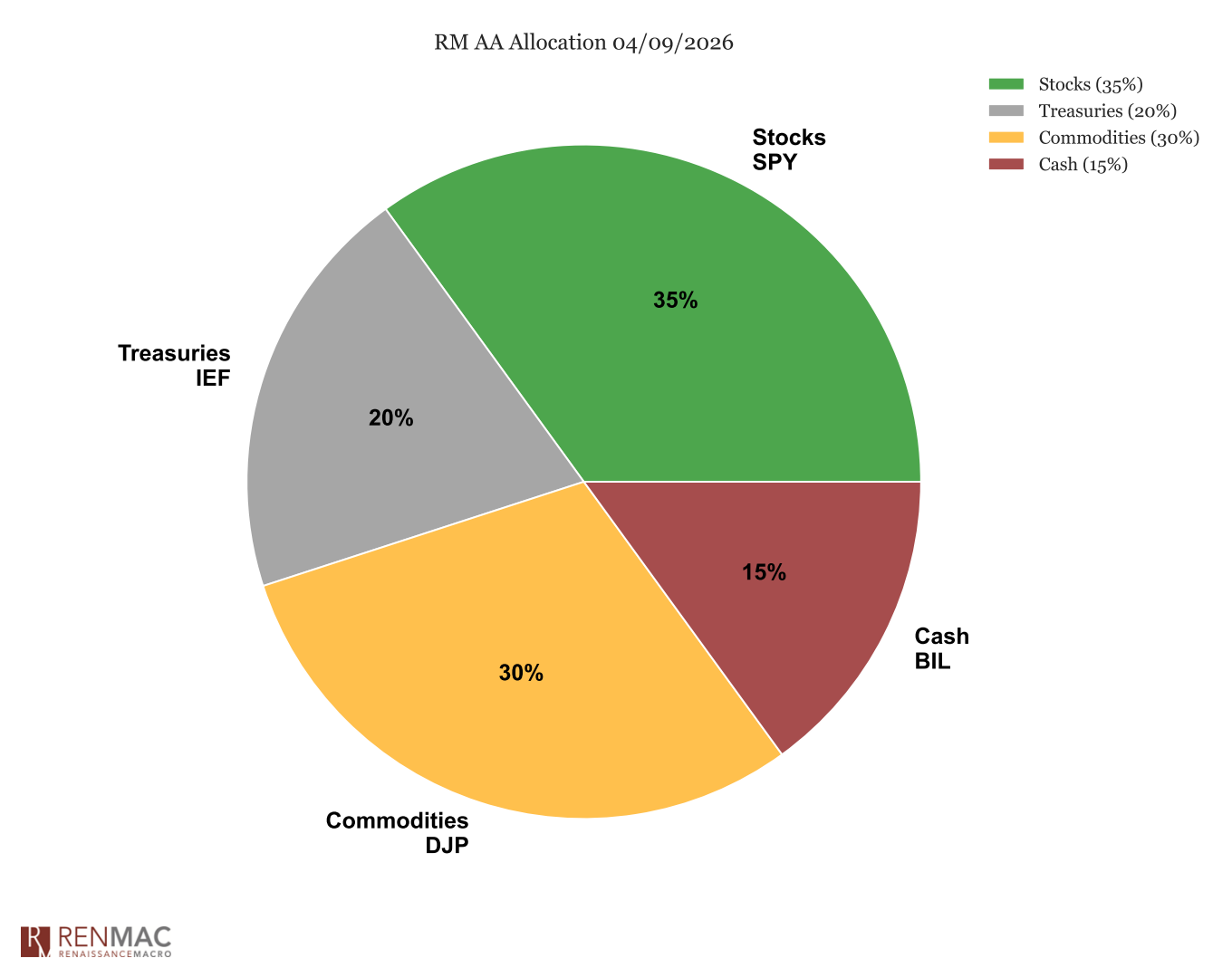

Asset Allocation Model

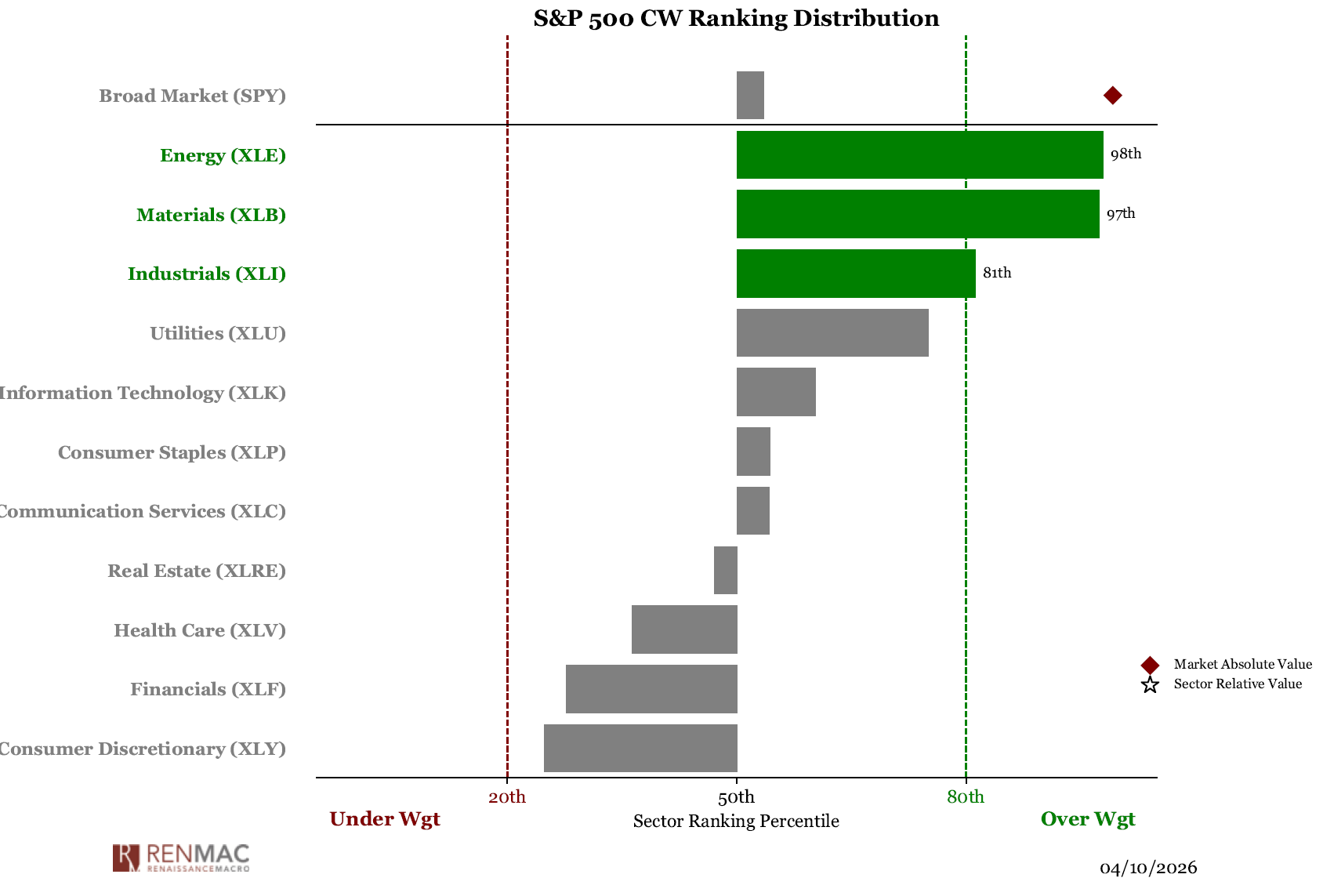

Sector Ranks

Sector Ranks  Chart of the week

Chart of the week